Despite a lack of major U.S. data releases, gold prices rose for another day while crude oil, bitcoin (BTC/USD), and U.S. Treasury yields traded lower.

What’s up with that?!

Here’s what you missed from yesterday’s trading:

Headlines:

- Japan consumer confidence index for March: 39.5 (40.0 forecast; 39.0 previous)

- Japan’s preliminary machine tool orders showed an 8.5% y/y decline in March (-8.0% y/y previous) likely due to weak domestic demand

- France’s trade deficit increased in February by €200M to €6B

- NFIB U.S. business optimism index: 88.5 (89.5 forecast; 89.4 previous)

- SNB Vice Chairman Martin Schlegel said on Tuesday that FX interventions are vital to managing inflationary & deflationary pressures

- Japan’s bank lending accelerated from 3.0% y/y to 3.2% y/y in March with outstanding bank lending hitting a new all-time high in fiscal year 2023

- Japan’s producer prices improved from 0.7% y/y to 0.8% y/y as expected in March

Broad Market Price Action:

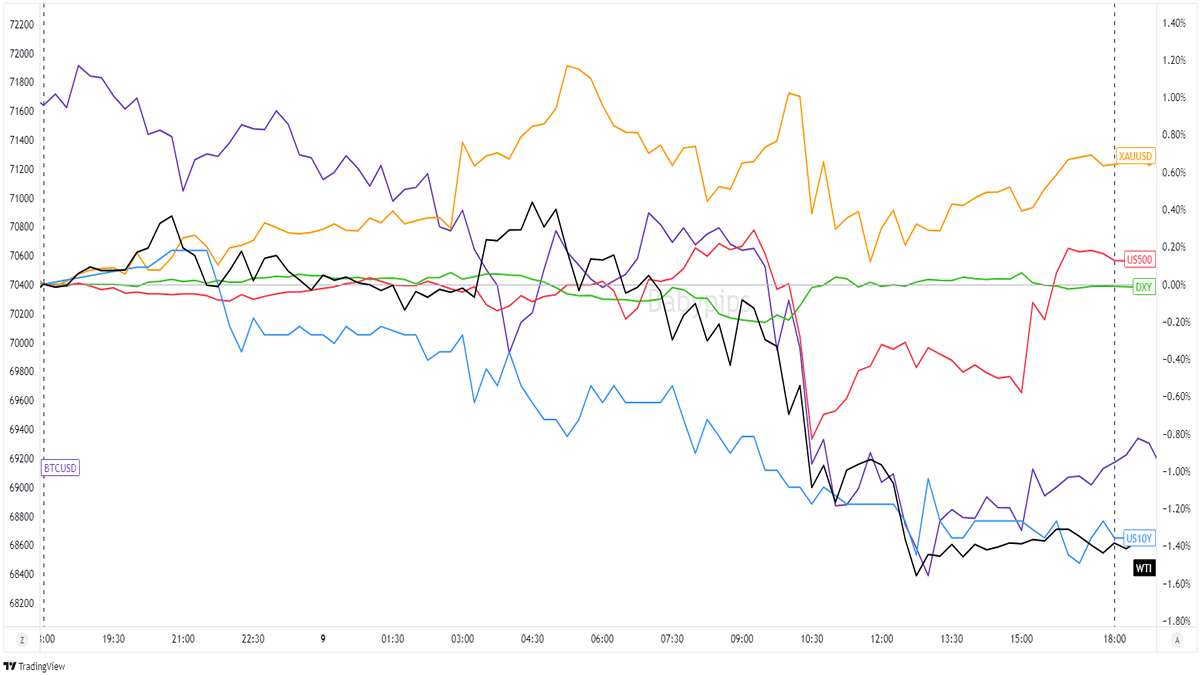

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

The major financial assets started the day with tight ranges except for bitcoin (BTC/USD) which continued to pull back from hitting notable highs on Monday. We saw some gold and oil-buying at the start of the European session but the moves were relatively limited as more traders likely stayed in the sidelines ahead of the awaited U.S. CPI reports.

“Risky” bets like U.S. stocks, crude oil, and bitcoin saw heavier selling early in the U.S. session. There were no data releases to back the move but some analysts point to short covering ahead of Uncle Sam’s inflation data as a possible catalyst.

U.S. 10-year Treasury yields also dipped which likely boosted gold. If you recall, the commodity was already getting support from its bullish momentum as well as increased demand from Indian and Chinese central banks.

Volatility was relatively limited for the rest of the trading session though we did see a bit of recovery for the S&P 500 index as it ended the day just above its opening prices.

FX Market Behavior: U.S. Dollar vs. Majors

Overlay of USD vs. Major Currencies Chart by TradingView

With not a lot of economic themes and data releases to price in, the U.S. dollar stayed in tight ranges at the start of the day. In fact, the Greenback didn’t see much action until the start of the European session when lower U.S. 10-year yields inspired a bit more USD selling.

Risk aversion and a bit of short covering likely boosted the safe haven near the start of the U.S. session but the dollar also gave up some of its session gains near the end of the trading day.

Upcoming Potential Catalysts on the Economic Calendar:

- Italy’s retail sales at 8:00 am GMT

- Canada’s building permits at 12:30 pm GMT

- U.S. CPI reports at 12:30 pm GMT

- FOMC member Michele Bowman to give a speech at 12:45 pm GMT

- BOC’s monetary policy decision at 1:45 pm GMT (presser at 2:30 pm GMT)

- U.S. EIA crude oil inventories at 2:30 pm GMT

- FOMC meeting minutes at 6:00 pm GMT

- U.S. Federal budget balance at 6:00 pm GMT

- U.K. RICS house price balance at 11:01 pm GMT

- Australia’s MI inflation expectations at am GMT (Apr 11)

- China’s CPI and PPI reports at 1:30 am GMT (Apr 11)

Wednesday traders are in for a BUSY day as we have a couple of closely-watched data releases on tap.

Traders are mostly anticipating Uncle Sam’s March inflation figures though the Bank of Canada’s (BOC) policy decision and China’s CPI and PPI reports during the Asian session may also inspire volatility among the major currencies.

Looking for your own spot to record your market observations & trading statistics? If so, then check out TRADEZELLA! It’s an easy-to-use journaling tool that can lead to valuable performance & strategy insights! You can easily add your thoughts, charts & track your psychology with each and every trade. Click here to see if it’s right for you!

Disclaimer: Babypips.com earns a commission from any signups through our affiliate link. When you subscribe to a service using our affiliate links, this helps us to maintain and improve our content, a lot of which is free and accessible to everyone–including the School of Pipsology! We appreciate your support and hope that you find our content and services helpful. Thank you!