Risk aversion was the name of the game on Tuesday, as caution ahead of this week’s top-tier market events got mixed in with weak U.S. tech equities performance and increased Middle East geopolitical tensions.

How did the major assets behave in the last trading sessions?

We’re sharing the deets:

Headlines:

- Australia building approvals for June: -6.5% m/m (-2.1% expected, 5.7% previous)

- France flash GDP for Q2 2024: 0.3% q/q (0.2% expected, previous quarter revised higher from 0.2% to 0.3%)

- Germany preliminary CPI accelerated from 0.1% m/m to 0.3% m/m in July; Annual CPI sped up from 2.2% to 2.3%

- Switzerland KOF economic barometer dipped from 102.7 to 101.0 (102.6 expected) in July; “The outlook for both foreign demand and consumer demand is worsening.“

- Germany preliminary GDP for Q2 2024: -0.1% q/q (0.1% expected, 0.2% previous)

- Euro Area flash GDP for Q2 2024: 0.3% q/q (0.2% expected, 0.3% previous)

- Israel’s military claimed it killed Hezbollah’s most senior commander in an airstrike on Beirut on Tuesday

- Conference Board U.S. Consumer Confidence Index for July 2024: 100.3 (100.0 forecast; 97.8 previous)

- U.S. JOLTs Job Openings for June: 8.18M (8.05M forecast; 8.23M previous)

- New Zealand building consents dropped sharply from -1.9% m/m to -13.8% m/m in June

- Japan preliminary industrial production fell by 3.6% m/m in June (-4.2% expected, 3.6% previous), as scandals involving large carmakers such as Toyota weighed on car and auto production

- Japan retail sales accelerated from 2.8% y/y to 3.7% y/y (3.3% expected) in June

- ANZ New Zealand business confidence jumped from 6.1 to 27.1 in July; Employment Intentions dropped from 0.0 to -3.6; Pricing Intentions rose from 35.3 to 37.6

- Speculations of a 25bps rate hike boosted JPY in the U.S. session

Broad Market Price Action:

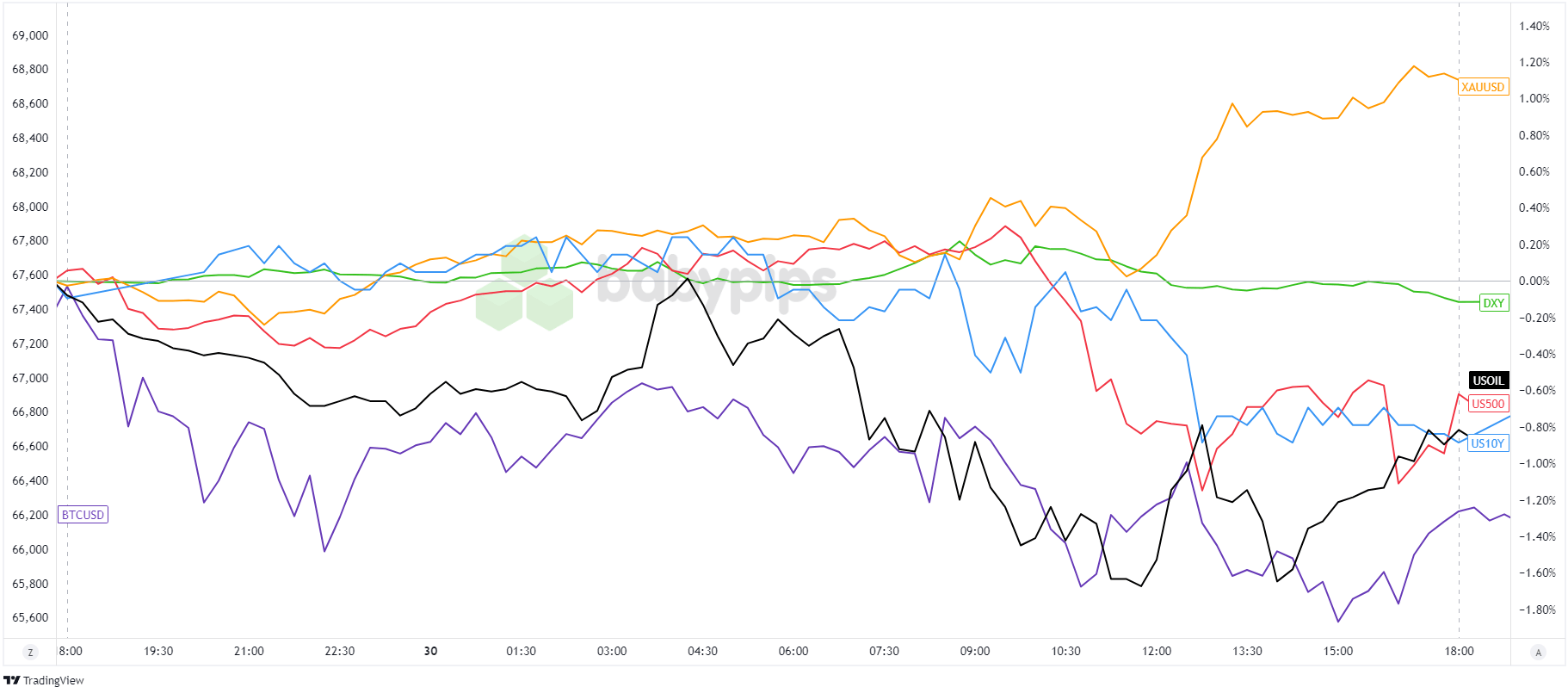

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

With just Japan’s employment data on the docket early in the day, Asian traders mostly kept things cautious, sticking to an anti-risk vibe ahead of this week’s big data releases.

Plots thickened during the U.S. session when a disappointing earnings report from Microsoft took the wind out of some optimism from AMD’s positive earnings. It also highlighted concerns that the AI-driven rally in U.S. stocks might be overextended.

Adding to the cautious mood, Germany’s GDP continued to show it’s lagging behind the rest of the Euro Area, and news that Israel claimed to have killed Hezbollah’s top commander in a Beirut operation on Tuesday didn’t help matters either.

To top it off, traders seem to be brushing off positive U.S. reports and instead are banking on a dovish shift from the Fed this week. As it stands, CME’s FedWatch Tool puts the odds of a 25bps rate cut in September at 86.3%.

Uncertainty ahead of this week’s central bank meetings, mixed U.S. earnings reports, and rising geopolitical tensions put pressure on U.S. Treasuries, the dollar, and risk assets like bitcoin, stock indices, and oil prices.

WTI crude oil hit $75.00 before finding some intraday support; BTC/USD quietly continued its weekly slide, revisiting $65,600; U.S. 10-year Treasury yields dipped from 4.19% to 4.13%; and both the S&P 500 and NASDAQ hit new weekly lows.

FX Market Behavior: U.S. Dollar vs. Majors:

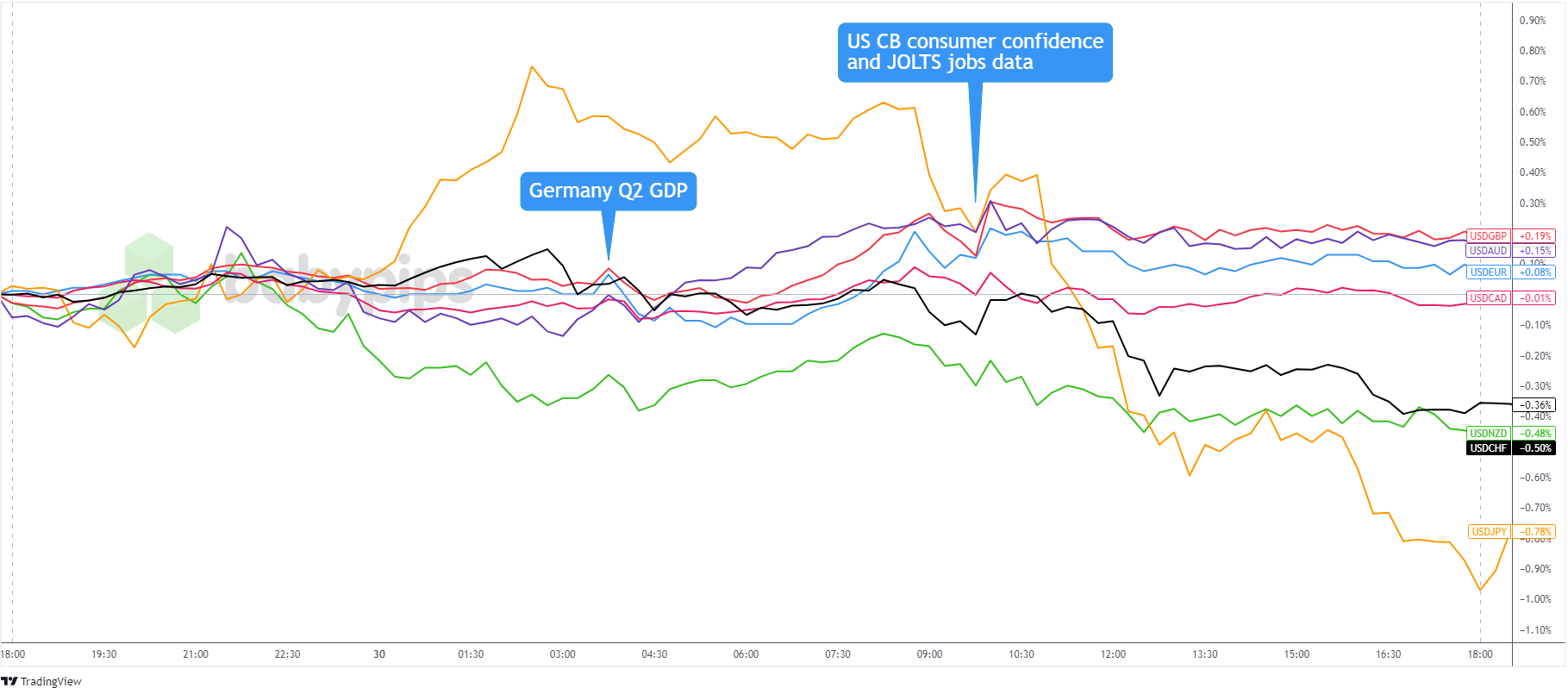

Overlay of USD vs. Major Currencies Chart by TradingView

The U.S. dollar had a mixed start to the day, reacting to a weaker yen and stronger NZD and AUD during the Asian session.

Things got more consistent during the U.S. session when the U.S. CB consumer confidence and JOLTS job reports gave the Greenback a boost.

But soon, traders shifted focus to pricing in a dovish Fed this week and the possibility of a September rate cut. This likely led to the dollar dropping against the Swiss franc and extending its losses against the yen and Kiwi.

JPY traders were active too, with the currency dropping – likely due to profit-taking – during the Asian session ahead of the BOJ’s decision. However, rumors started circulating that the BOJ might surprise the market with a 25bps rate hike this week. These hawkish speculations supported the yen throughout most of the U.S. session, and the currency ended the day higher across the board.

The British pound didn’t fare well either, as speculation about a dovish lean from the BOE later this week weighed on the currency.

Upcoming Potential Catalysts on the Economic Calendar:

- BOJ’s policy decision scheduled during the Asian session

- France’s preliminary CPI at 6:45 am GMT

- Germany’s unemployment change at 7:55 am GMT

- Euro Area inflation data at 9:00 am GMT

- Italy’s preliminary CPI at 9:00 am GMT

- U.S. ADP report at 12:15 pm GMT

- Canada’s monthly GDP at 12:30 pm GMT

- U.S. quarterly employment cost index at 12:30 pm GMT

- U.S. Chicago PMI at 1:45 pm GMT

- U.S. pending home sales at 2:00 pm GMT

- FOMC statement at 6:00 am GMT, presser to follow 30 minutes later

We’ve got a parade of top-tier economic reports today that are likely to cause increased volatility for the major assets.

BOJ’s policy decision may dominate headlines until the European session until the Euro Area prints its inflation data.

In the U.S., all eyes will be on the Fed’s policy statement for clues on any changes to the members’ hawkishness and near-term policy biases. If the members don’t lean into a bias and the event turns out to be a non-mover, more attention may be paid to the U.S. ADP and quarterly employment cost index reports and what they could mean for Friday’s NFP release.