Traders seem to have woken up on the wrong side of the bed this Monday, as major asset classes found themselves in the red.

What’s going on?

Here’s a quick rundown of the headlines and economic updates that affected the markets:

Headlines:

- BOJ meeting minutes revealed that policymakers were wary of the weak yen’s impact on import prices and household spending

- Australia’s MI inflation gauge for July ticked higher from 0.3% m/m to 0.4%

- New Zealand ANZ commodity prices for July: -1.7% m/m (+1.5% previous)

- Chinese Caixin services PMI for July: 52.1 (51.4 expected, 51.2 previous)

- Eurozone final services PMI for July unchanged at 51.9 as expected

- Eurozone Sentix investor confidence index for August: -13.9 (-5.5 expected, -7.3 previous)

- Eurozone PPI for July: 0.5% m/m (0.1% expected, -0.2% previous)

- FOMC member Goolsbee acknowledged that jobs data is weaker than expected but not indicative of recession

- U.S. S&P Global final services PMI downgraded from 56.0 to 55.0 in July vs. expectations of no change

- U.S. ISM services PMI in July: 51.4 (51.1 expected, 48.8 previous)

- FOMC member Daly noted that risks to Fed’s mandate are getting more into balance, open to cutting rates in upcoming meetings

- CBOE Volatility Index a.k.a. the Fear Gauge surged to its highest level of 65 since October 2020

- U.K. BRC retail sales monitor rebounded 0.3% y/y in July after earlier 0.5% drop

- Japanese average cash earnings in June: 4.5% y/y (2.5% expected, previous reading upgraded from 1.9% to 2.0%)

- Japanese household spending in June: -1.4% y/y (-0.9% expected, -1.8% previous)

Broad Market Price Action:

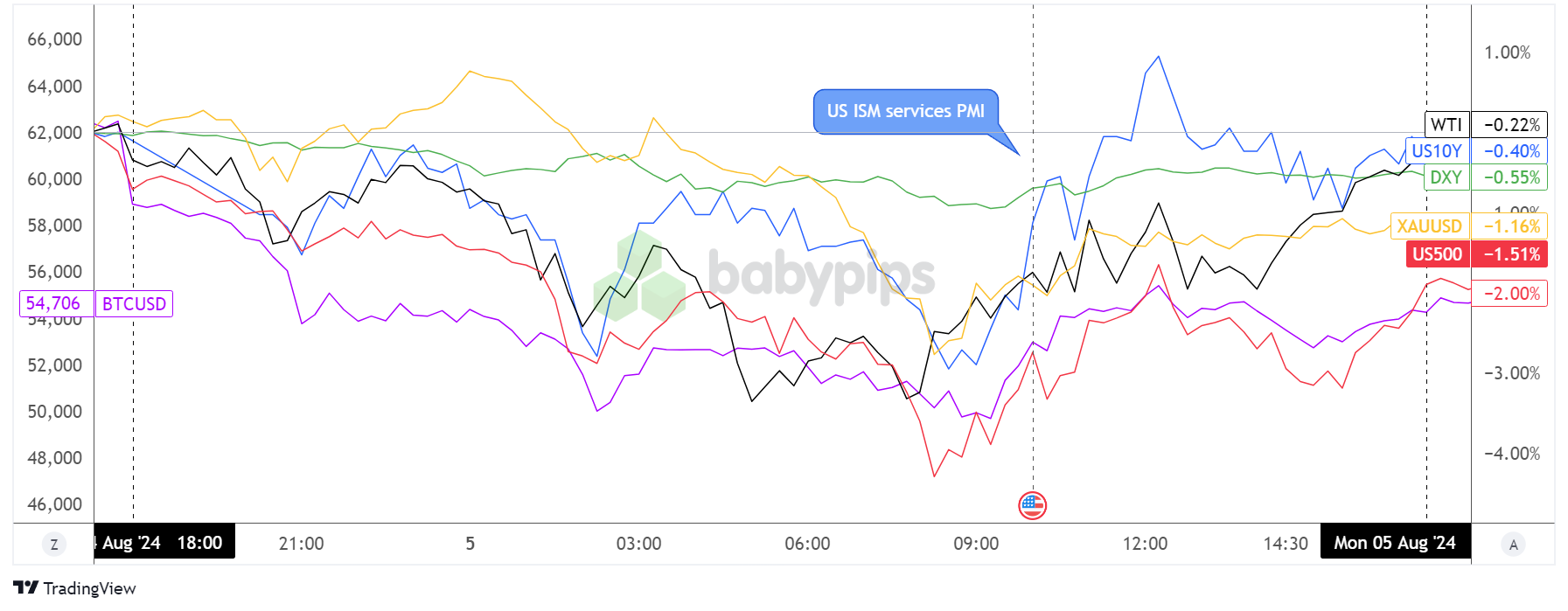

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Financial markets were still reeling in the aftermath of a dismal U.S. NFP release last Friday, as the jobs report led investors to worry that recession may be looming.

Asian equities started on a negative note, with Japanese markets chalking up their worst declines since 1987, followed by similarly steep drops for European stocks and roughly 3% in losses for U.S. equity indices.

Commodities like precious metals and crude oil also found themselves deep in the red, as gloomier global growth prospects would likely weigh heavily on demand. Still, some of the losses were pared around the start of the New York session, but not enough to put risk assets back in positive territory.

Treasury yields managed to pull off a much stronger rebound, getting an additional boost from the U.S. ISM services PMI that returned to expansionary territory and eased some recession fears.

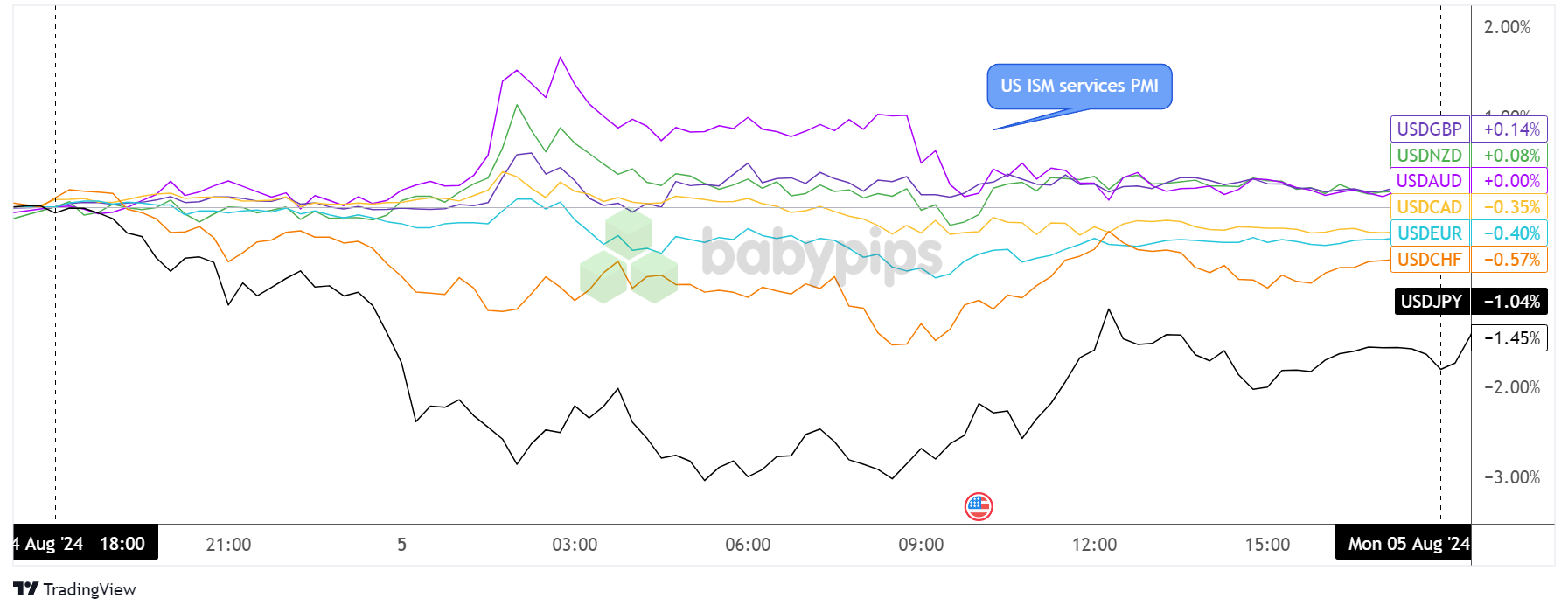

FX Market Behavior: U.S. Dollar vs. Majors:

Overlay of USD vs. Major Currencies Chart by TradingView

While majority of dollar pairs started the week off in consolidation, USD/JPY and USD/CHF were eager to get the bearish ball rolling in resuming their post-NFP slump.

The dollar broke higher against a few higher-yielding counterparts towards the end of the Asian trading session, although there appears to have been no clear catalyst for the move apart from a general dip in risk appetite.

Another round of sideways price action followed before the stronger than expected U.S. ISM services PMI sparked some gains for the U.S. currency.

Upcoming Potential Catalysts on the Economic Calendar:

- RBA monetary policy decision at 4:30 am GMT

- RBA press conference at 5:30 am GMT

- Swiss jobless rate at 5:45 pm GMT

- German factory orders at 6:00 pm GMT

- Swiss retail sales at 6:30 am GMT

- U.S. trade balance at 12:30 am GMT

- Canada’s trade balance at 12:30 am GMT

- New Zealand employment change data at 10:45 pm GMT

The spotlight shifts to the Land Down Under, as the Reserve Bank of Australia (RBA) is gearing up to announce its monetary policy decision. The central bank will also release its updated economic projections in its quarterly Statement on Monetary Policy, so keep your eyes peeled for any revisions that could serve as clues for their future policy moves.

Much later on, New Zealand will be printing its quarterly jobs data that might have major implications for the RBNZ’s policy bias as well.