Financial markets waited eagerly for the U.S. preliminary GDP release for the most part of the day, and the numbers did not disappoint!

Upgrades to growth and inflation figures were announced, sparking risk-on flows and some gains for Treasury yields and the dollar as well.

Read on to find out which other headlines affected asset classes during the latest trading sessions:

Headlines:

- New Zealand ANZ business confidence index jumped from 27.1 to 50.6 in August

- Australian private capital expenditure sank 2.2% q/q in Q2 2024 vs. projected 0.9% uptick, previous reading upgraded from 1.0% to 1.9%

- Japanese consumer confidence index held steady at 36.7 vs. expected pickup to 36.9

- Spanish flash CPI slowed from 2.8% y/y to 2.2% in July vs. 2.4% estimate

- German preliminary CPI showed a 0.1% m/m dip in July vs. expected 0.2% uptick, previous 0.3% gain

- U.S. Q2 2024 GDP upgraded from advanced 2.8% q/q reading to 3.0% thanks to stronger consumer spending, price index revised higher from initial 2.3% to 2.5% q/q

- U.S. goods trade deficit widened from $96.6B to $102.7B vs. expected $97.7B shortfall

- U.S. initial jobless claims at 231K for the week ending August 22 vs. 232K forecast, 233K previous

- U.S. pending home sales chalked up a steeper 5.5% m/m slump in July to lowest on record since 2001, as high borrowing costs weighed on sentiment

- SNB head Jordan says weak euro zone demand is dampening Swiss export activity

- ECB official and Bundesbank head Nagel suggested that they shouldn’t rush to cut again since inflation hasn’t reached 2% target

Broad Market Price Action:

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Major asset classes started the day off on a chill note, as investors were likely holding out for the release of the second version of the U.S. GDP. Volatility picked up slightly right around the start of the London session, causing a dip for both crude oil and U.S. bond yields while bitcoin continued its steady rise.

Upgrades to both the U.S. growth figure and price index for Q2 2024 sparked a run higher for risk assets like crude oil and equities, as the numbers appeared to soothe slowdown concerns, and an uptick for the dollar and Treasury yields thanks to upbeat expectations for Friday’s core PCE release.

On the flip side, gold prices took a hit upon seeing the preliminary GDP report, although the precious metal managed to keep its head above water since it quickly rebounded after the initial dip. BTC/USD, on the other hand, hit a ceiling at the $61,000 mark and retreated close to $59,000 before the end of the U.S. session.

U.S. equities also struggled to hold on to their post-GDP gains before the closing bell, with the S&P 500 index and Nasdaq ending roughly flat for the day.

FX Market Behavior: U.S. Dollar vs. Majors:

Overlay of USD vs. Major Currencies Chart by TradingView

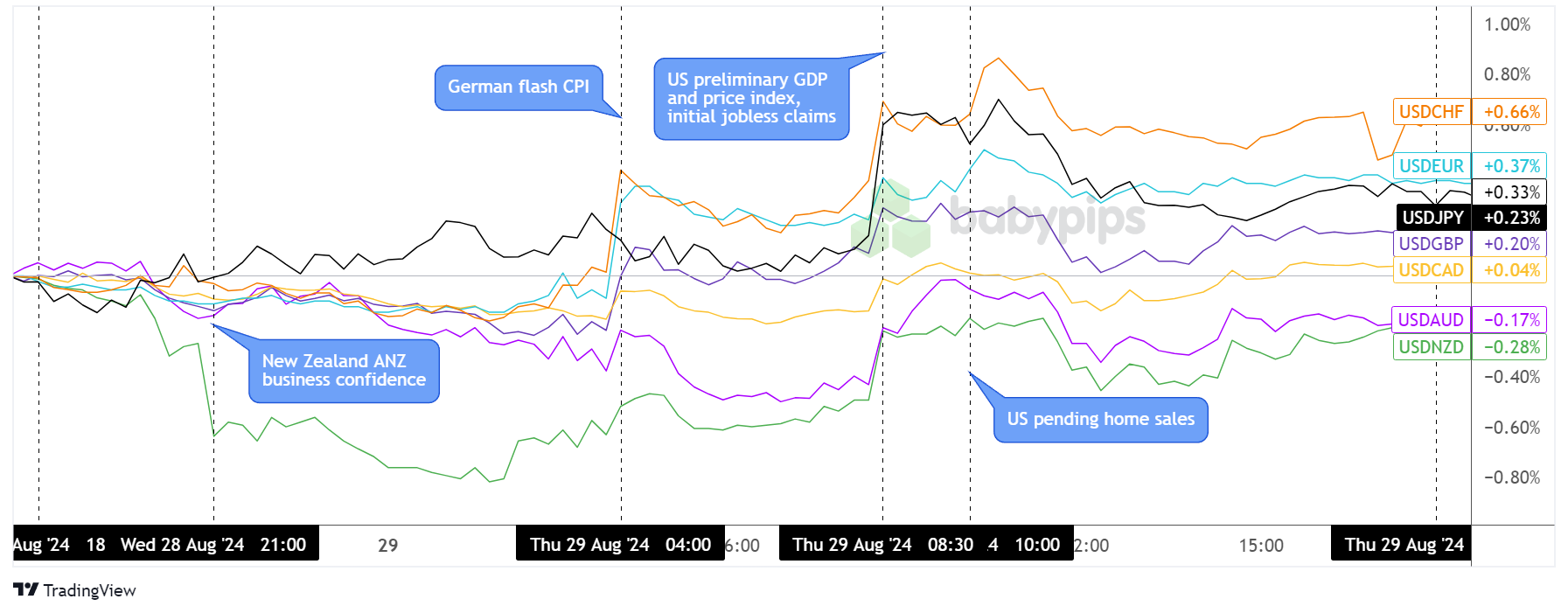

Most major pairs were off to a generally slow start, with the exception of NZD/USD which popped higher early in the Asian session thanks to a notable improvement in New Zealand’s business confidence index for August.

The dollar cruised gradually lower against majority of its peers throughout most of the Asian trading session, except against the Japanese yen which was likely bogged down by the lack of improvement in the country’s consumer confidence index for July.

Weaker than expected inflation data from eurozone economies namely Germany and Spain led to a dip for the shared currency, along with its fellow European currencies, around the start of the London session.

A bit more consolidation followed, before the dollar staged an intraday rally across the board thanks to upgrades in the U.S. Q2 2024 preliminary GDP reading. The initial jobless claims figure also came in somewhat better than expected at 231K versus the 232K forecast.

However, the U.S. currency pared most of its post-GDP winnings later on, as the pending home sales report reflected a sharp tumble to record lows due to higher borrowing costs. Still, the Greenback managed to close out in the green versus the yen and European currencies, as well as the Canadian dollar.

Upcoming Potential Catalysts on the Economic Calendar:

- Australia retail sales at 1:30 am GMT

- German retail sales and import prices at 6:00 am GMT

- French preliminary GDP and CPI at 6:45 am GMT

- Swiss KOF economic barometer at 7:00 am GMT

- German unemployment rate at 7:55 am GMT

- Eurozone flash CPI estimates at 9:00 am GMT

- Canadian GDP at 12:30 pm GMT

- U.S. core PCE price index at 12:30 pm GMT

- Chicago PMI at 1:45 pm GMT

- U.S. revised UoM consumer sentiment index at 2:00 pm GMT

Today could be all about inflation updates, as the eurozone is gearing up to print its flash headline and core CPI readings for July, potentially affecting ECB policy expectations.

Uncle Sam is also due to release the core PCE price index, which is said to be the Fed’s preferred inflation measure, so better stay on your toes for additional financial market volatility and month-end profit-taking activity!

And if you’re trading multiple major currency pairs at the same time, be aware of currency correlations to avoid accidentally overexposing your trading account to larger-than-expected risk.