U.S. and Canadian traders were out enjoying the Labor Day holiday on Monday, but that didn’t stop global markets from making big moves!

Crude oil had a topsy-turvy run, as it gapped down over the weekend but eventually pulled higher to close in the green.

Check out which headlines pushed the rest of the major asset classes around:

Headlines:

- Chinese official manufacturing PMI dipped further into contraction to 49.1 in August from 49.4 while the non-manufacturing PMI picked up slightly to 50.3 from 50.2 in July

- OPEC+ confirmed plans to increase production by 180,000 barrels per day starting in October despite the loss of Libyan output

- Australia’s Melbourne Institute inflation gauge dipped by 0.1% m/m in August after rising by 0.4% m/m in July

- ANZ-Indeed Australian job ads slipped by another 2.1% m/m after a 2.7% decline in July

- Australia’s company operating profits tumbled 5.3% q/q in Q2 vs. projected 0.6% gain, previous 2.5% decline

- Australia building approvals jumped by 10.4% m/m in July (vs 2.4% expected, -6.4% previous)

- Australia’s commodity prices slipped 5.2% y/y in August, previous reading downgraded from -3.0% to -4.2%

- China’s Caixin manufacturing PMI for August showed a surprise jump to expansion territory coming in at 50.4 from 49.8 in July.

- Swiss retail sales jumped 2.7% y/y in July vs. projected 0.2% dip, previous reading downgraded from -2.2% to -2.6%

- Swiss manufacturing PMI rose from 43.5 to 49.0 in August vs. 43.7 forecast

- Spanish manufacturing PMI fell from 51.0 to 50.5 vs. 51.4 forecast in August

- US and Canadian markets closed for Labor Day holiday

- Libya’s Sarir, Messla, and Nafoura oilfields were instructed to resume operations after a political standoff

- EIA data revealed that U.S. oil consumption in June slowed to its lowest seasonal levels since the 2020 pandemic

- New Zealand overseas trade index in Q2 2024 slowed to 2.1% from previous 5.1%, forecast at 2.6% q/q

- U.K. BRC retail sales monitor rose from 0.3% to 0.8% y/y in August

Broad Market Price Action:

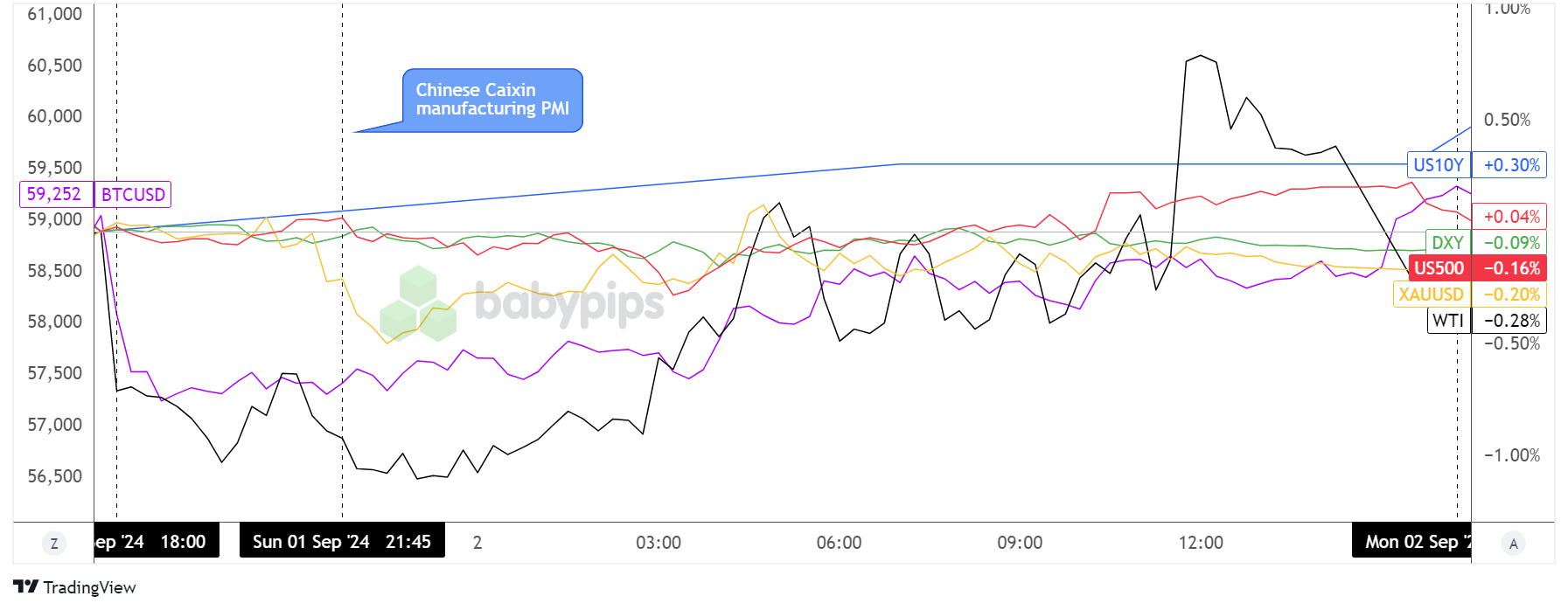

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Crude oil bears were quick to react to weekend news of the OPEC+ confirming that they will increase production in October, leading the energy commodity to gap down once the markets opened. It didn’t help that China’s official manufacturing PMI figures also released over the weekend failed to impress.

Bitcoin was also off to a rough start, as it tumbled to the $57,500 area from the get-go before gradually recovering back to its open price around $59,000 throughout the day.

Meanwhile, gold prices dipped upon seeing China’s Caixin manufacturing PMI, which came in better than expected and reflected industry expansion. The precious metal spent most of the day trading below its record highs while crude oil managed to bottom out and pull higher as London session traders got to their desks.

However, the commodity tumbled once again upon hearing news of Libya’s oilfields being instructed to resume production and the EIA reporting that oil consumption in June fell to its lowest seasonal levels since 2020.

U.S. and Canadian markets were closed during the Labor Day holiday, translating to subdued volatility for equities and dollar pairs during New York market hours.

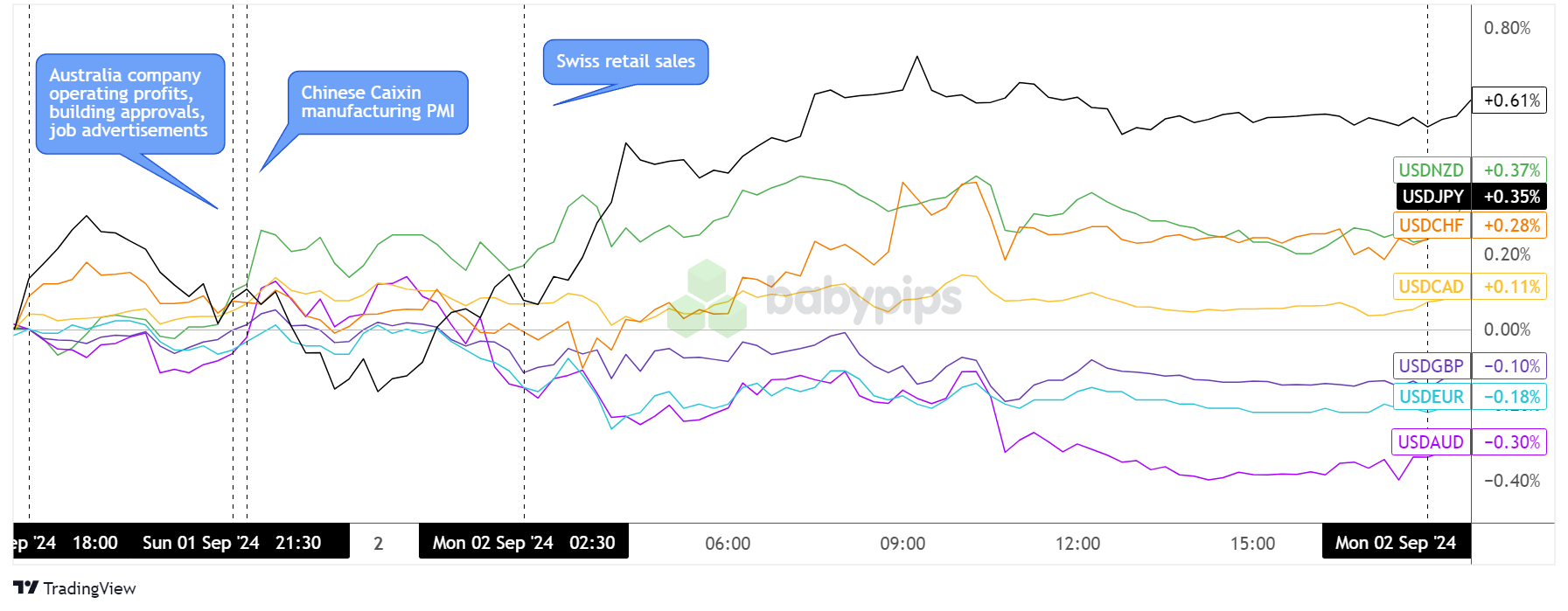

FX Market Behavior: U.S. Dollar vs. Majors:

Overlay of USD vs. Major Currencies Chart by TradingView

USD/JPY was off to a running start, as the pair still seemed to be enjoying the aftermath of Friday’s post-core PCE rally. However, the pair retreated for the most part of the Asian trading session before eventually pulling higher during London market hours.

Most major pairs moved generally sideways early on, with the exception of NZD/USD and AUD/USD which appeared to be bogged down by China’s downbeat official PMI readings and net negative economic updates from Australia.

USD/CHF edged slightly lower upon seeing upbeat Swiss retail sales and manufacturing PMI data, but dollar strength took over. The U.S. currency held on to its gains versus the yen, Loonie, and Kiwi until the end of the day while giving up ground to sterling, the euro and the Aussie.

Upcoming Potential Catalysts on the Economic Calendar:

- Swiss CPI at 6:30 am GMT

- Swiss GDP at 7:00 am GMT

- U.S. ISM manufacturing PMI at 2:00 pm GMT

- New Zealand Global Dairy Trade auction coming up

- ECB official and German Bundesbank head Nagel’s testimony at 4:45 pm GMT

We’ve got a couple of potential market movers on deck today, starting off with Switzerland’s CPI reading that could strongly impact SNB policy expectations.

After that, all eyes and ears are likely to be on Uncle Sam’s August ISM manufacturing PMI since traders are looking out for clues ahead of this week’s highly-anticipated NFP release.

And if you’re trading multiple major currency pairs at the same time, be aware of currency correlations to avoid accidentally overexposing your trading account to larger-than-expected risk.

Don’t forget to check out our brand new Forex Correlation Calculator!