Market correlations moved out of sync on Wednesday, as major asset classes seemed to respond to their individual catalysts.

Forex price action was mostly a mess, too, although the U.S. dollar was generally weaker throughout the day.

Here are the latest economic updates and headlines that pushed markets around:

Headlines:

- New Zealand ANZ commodity prices rebounded 2.1% year-on-year in August vs. previous 1.7% decline

- Australian economy expanded 0.2% q/q as expected in Q2 2024, previous GDP reading upgraded from 0.1% to 0.2%

- Chinese Caixin services PMI fell from 52.1 to 51.6 in August vs. estimated 51.9 figure

- Eurozone final services PMI in August downgraded from 53.3 to 52.9 vs. expectations of no change

- U.K. final services PMI in August upgraded from 53.3 to 53.7 to reflect faster pace of growth

- Eurozone PPI accelerated from upgraded 0.6% m/m in June to 0.8% in July vs. 0.3% forecast

- OPEC+ reportedly considering a delay in output boost since Libya will resume production

- Bank of Canada (BOC) cut interest rates by 0.25% from 4.50% to 4.25% and hinted at more easing to come

- U.S. JOLTS job openings fell from downgraded 7.91M (8.18M initial) in June to 7.67M in July (8.09M) forecast

- Fed Beige Book highlighted “flat or declining” economic activity, disappointing labor market

Broad Market Price Action:

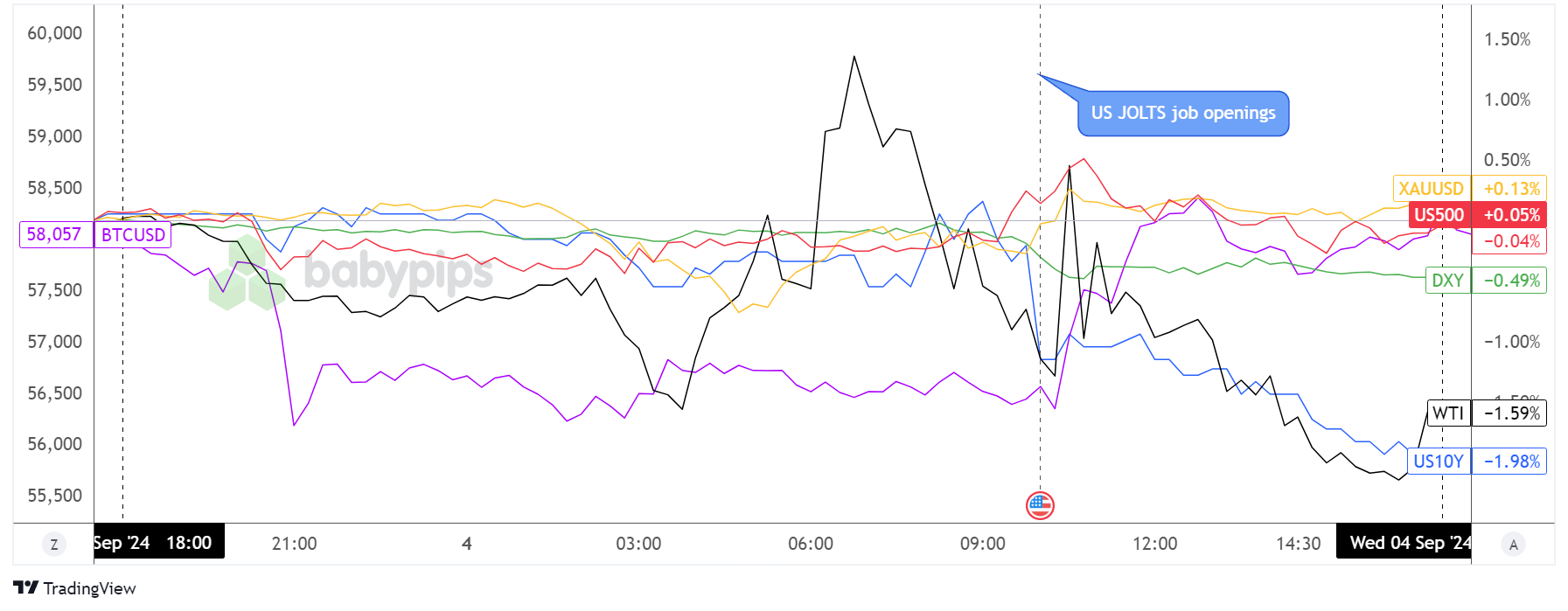

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

While most asset classes moved cautiously during Asian market hours, bitcoin and crude oil kicked the day off in the red, possibly still in the aftermath of the previous session’s selloff.

Energy commodities cruised further south upon seeing weaker than expected Chinese Caixin services PMI data, as this reinforced demand concerns. Prices turned higher around the London trading session when investors started buzzing about a potential delay in the OPEC+ output boost now that Libya is set to resume oil production, but the gains were erased towards the start of the New York session.

Treasury yields carried on with their slide upon seeing lower than expected U.S. JOLTS job openings data while bitcoin took advantage of USD weakness then. U.S. equity indices took a breather from their earlier slump, as the downbeat employment figures once again sparked talks of a larger Fed rate cut later this month.

FX Market Behavior: U.S. Dollar vs. Majors:

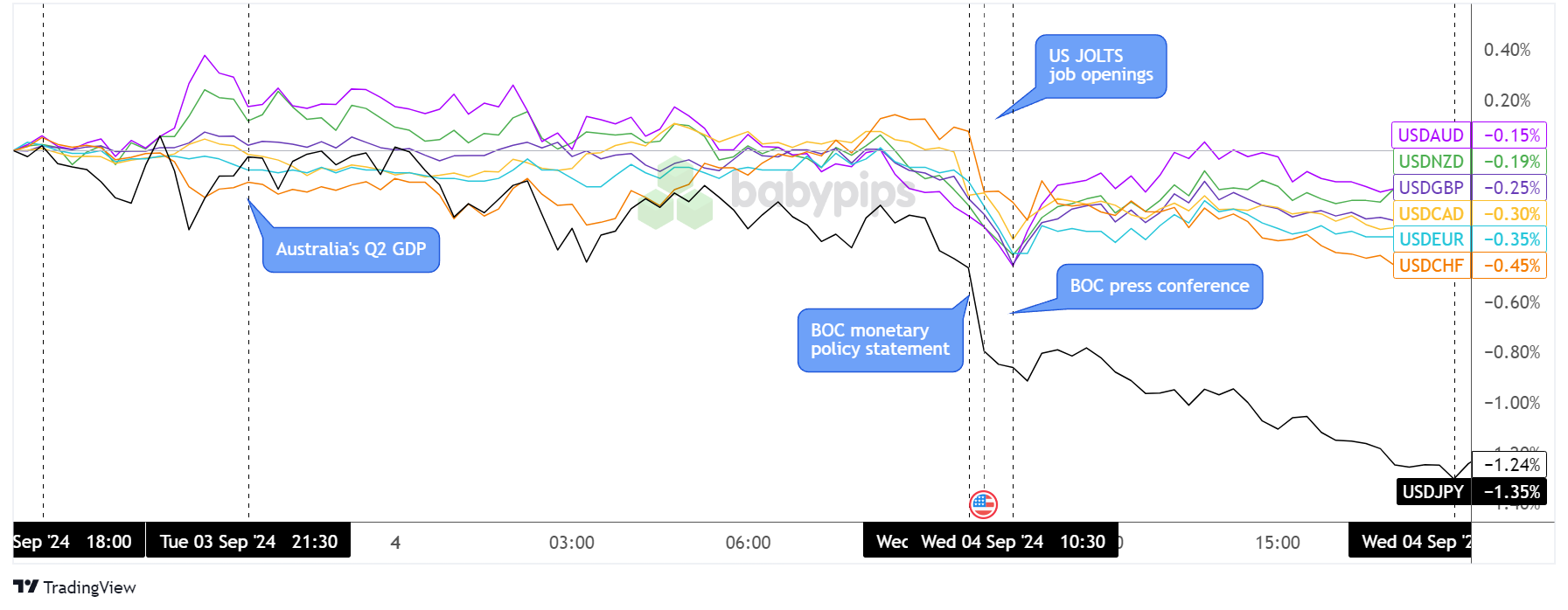

Overlay of USD vs. Major Currencies Chart by TradingView

Major pairs traded in wider than usual ranges with a slight bearish tilt for the U.S. currency during the Asian trading session. The Aussie and Kiwi started the day off on the back foot, and the Australian GDP and Caixin services PMI did little to steer these commodity currencies in a clearer direction.

A bit of sideways price action was seen around the start of the London session, before the dollar turned lower again. The U.S. JOLTS job openings figure for July came in below expectations and saw a negative revision to the previous month’s reading, spurring expectations of a potential NFP miss later this week.

The Bank of Canada (BOC) also announced its monetary policy decision to cut rates by 0.25% as expected and signaled more easing to come, but this didn’t really spark additional volatility for USD/CAD.

While majority of the dollar’s counterparts resumed rangebound action after the JOLTS report, USD/JPY carried on with its decline and closed more than 1% lower for the day.

Upcoming Potential Catalysts on the Economic Calendar:

- RBA Governor Bullock’s speech at 2:00 am GMT

- Swiss jobless rate at 5:45 am GMT

- U.S. Challenger job cuts at 11:30 am GMT

- U.S. ADP non-farm employment change at 12:15 pm GMT

- U.S. initial jobless claims at 12:30 pm GMT

- U.S. ISM services PMI at 2:00 pm GMT

- EIA crude oil inventories at 3:00 pm GMT

We’ve got a fresh set of leading U.S. jobs indicators on deck today, namely the Challenger job cuts, ADP non-farm employment change, and ISM services PMI. Keep an eye out for additional USD volatility since these could contain hints for the highly-anticipated non-farm payrolls report due Friday.

Don’t forget to check out our brand new Forex Correlation Calculator!