Markets still seem uneasy ahead of this week’s FOMC decision, as intermarket correlations appeared to be a mess even while the U.S. dollar cheered the upside surprise in headline retail sales.

Crude oil had its usual volatile run while gold prices eased further from its all-time highs. Meanwhile equity indices closed nearly flat while investors are biting their nails ahead of the Fed’s big announcement.

What else is driving price action lately? Check out these latest headlines and economic updates:

Headlines:

- Chinese banks still closed for the Mid-Autumn Festival holidays

- Japanese tertiary industry activity index rebounded by 1.4% month-on-month in July vs. expected 0.8% uptick and previous 1.2% decline

- German ZEW economic sentiment index in September: 3.6 (17.1 expected, 19.2 previous)

- Eurozone ZEW economic sentiment index in September: 9.3 (16.3 expected, 17.9 previous)

- Canadian housing starts slowed from 280K to 217K in August vs. 252K forecast

- Canada’s headline monthly CPI in August: -0.2% (0.0% expected, +0.4% previous); annual reading slowed from 2.5% year-on-year to 2.1% – lowest reading since Feb 2021

- Canada’s core monthly CPI down 0.1% (previous +0.3% gain); annual reading fell from 1.7% to 1.5% as expected

- U.S. headline retail sales in August: +0.1% m/m (-0.2% forecast, previous reading upgraded from 1.0% to 1.1%); core retail sales up 0.1% m/m (0.2% forecast, 0.4% previous)

- U.S. industrial production in August: 0.8% m/m (0.2% forecast, previous reading downgraded from -0.6% to -0.9%); capacity utilization at 78% (77.9% forecast, previous reading revised to 77.4%)

- U.S. NAHB housing market index up from 39 to 41 as expected in August

- Australia’s CB leading index recovered 0.1% m/m in July vs. previous 0.2% dip

- New Zealand GDT auction yielded 0.8% increase in dairy prices after earlier 0.4% decline

- New Zealand Westpac consumer sentiment index improved from 82.2 to 90.8 in Q3 2024

Broad Market Price Action:

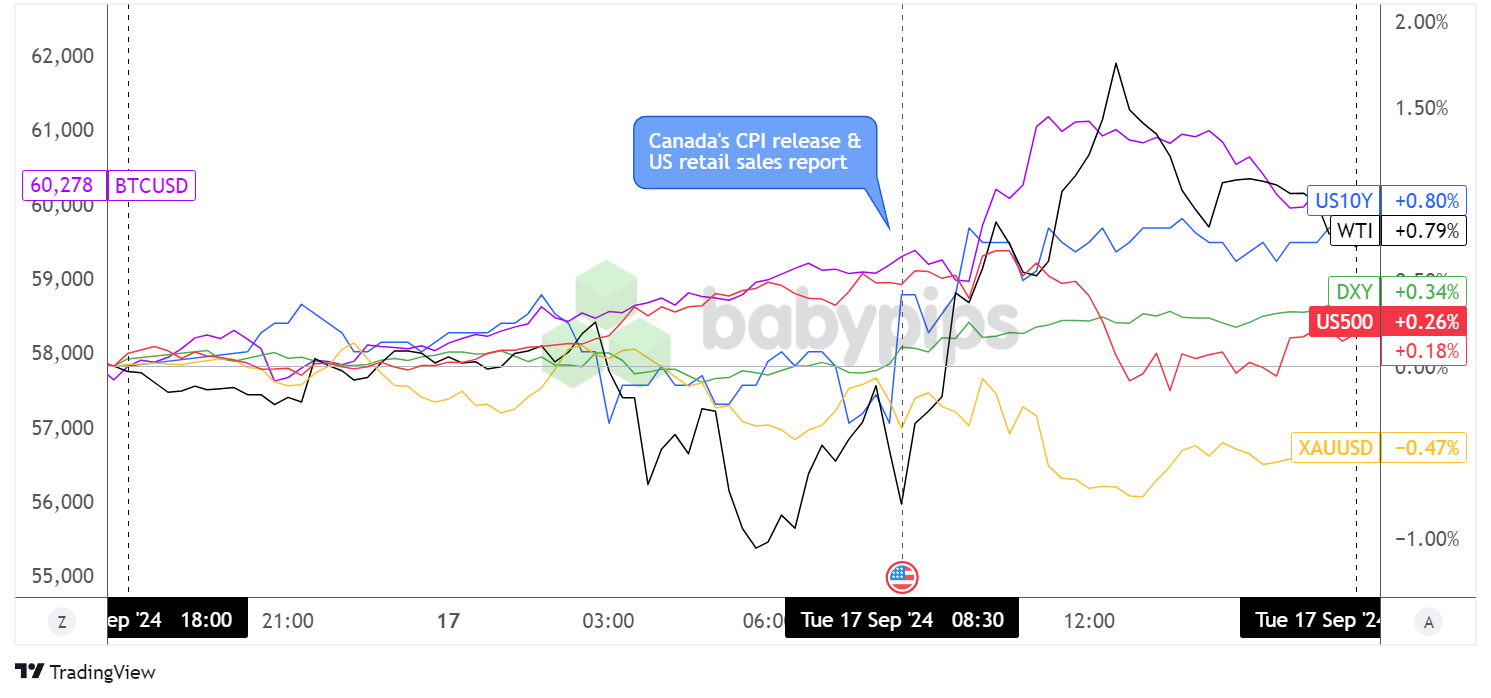

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Although volatility was slightly more elevated compared to the previous day’s Asian trading session, major asset classes still seemed to struggle to find a clear direction based on sentiment.

Treasury yields kept tossing and turning, as traders weighed the likelihood of a 0.25% Fed rate cut versus a 0.50% reduction in borrowing costs for the upcoming FOMC decision, before turning higher upon seeing upbeat U.S. headline retail sales data.

U.S. equity indices, which had already been cruising higher in the earlier trading session, fought to stay afloat during the first few hours of the New York session before eventually ending the day mostly flat.

Bitcoin, which started a steady climb early in the day, staged a steeper ascent to test the $61,000 mark then retreated back to the $60,000 handle. On the flip side, gold slipped further from its all-time highs while USD strength returned.

After its shaky run during the London session, crude oil also picked up upon seeing mostly upbeat U.S. consumer spending figures, as these could be indicative of stronger demand for energy commodities down the line.

FX Market Behavior: U.S. Dollar vs. Majors:

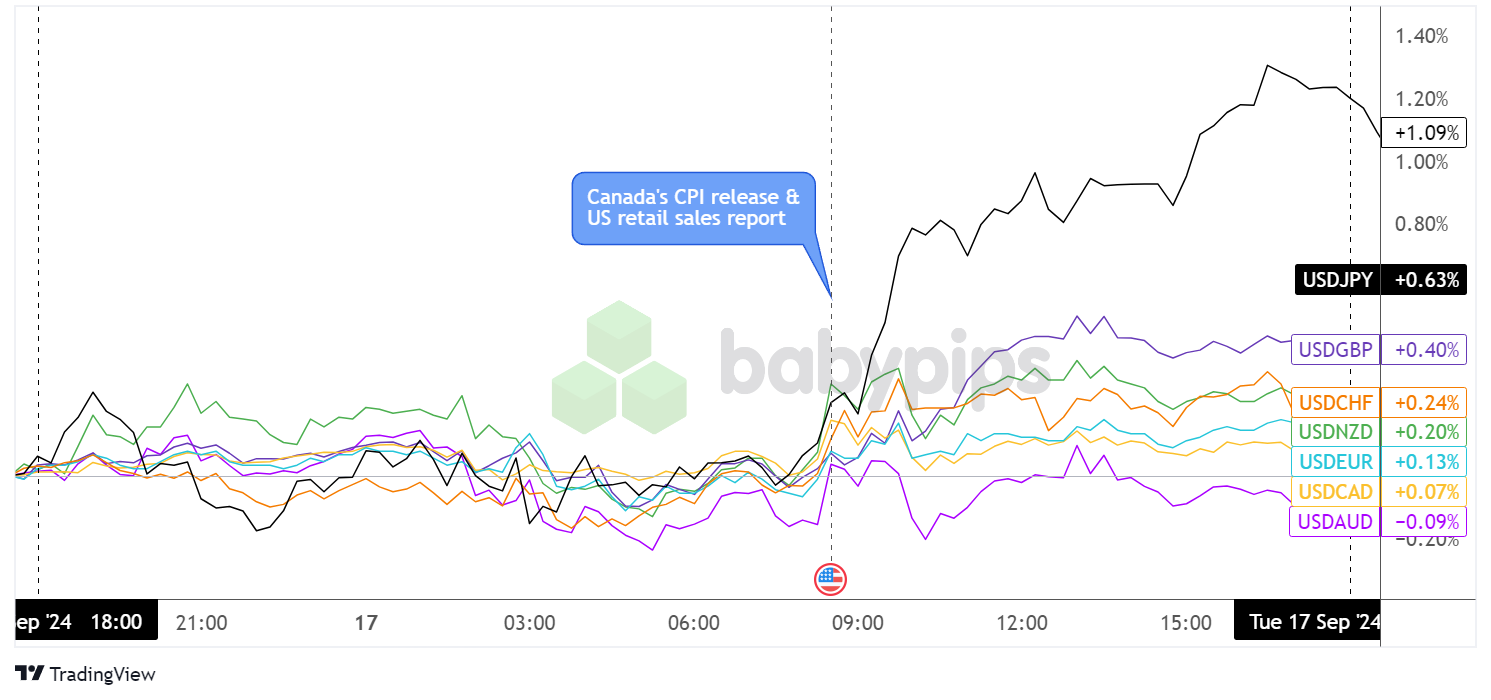

Overlay of USD vs. Major Currencies Chart by TradingView

After trading mostly sideways in Asian market hours and during the early London session, the U.S. dollar managed to chalk up some gains against majority of its peers during the U.S. retail sales release.

The headline reading for August turned out better than expected with a 0.1% monthly uptick versus expectations of a 0.2% dip while the July consumer spending figure was upgraded from 1.0% to 1.1%. Meanwhile, the core reading fell short of estimates with a meager 0.1% month-on-month increase instead of the projected 0.2% gain.

The dollar chalked up its strongest gains versus the yen, as USD/JPY proceeded to rally and close more than 1% higher for the day, followed by GBP, CHF, and NZD.

Weaker than expected Canadian CPI readings also dragged the Loonie south versus the dollar, but losses were short-lived likely because the rally in crude oil helped keep the correlated Canadian currency afloat. Only the Aussie ended the day higher versus the dollar, despite the dip in gold prices.

Upcoming Potential Catalysts on the Economic Calendar:

- U.K. CPI report at 6:00 am GMT

- U.K. PPI figures at 6:00 am GMT

- Eurozone final headline and core CPI at 9:00 am GMT

- U.S. building permits and housing starts at 12:30 am GMT

- U.S. EIA crude oil inventories at 2:30 pm GMT

- BOC Summary of Deliberations at 5:30 pm GMT

- FOMC statement and economic projections at 6:00 pm GMT

- FOMC press conference at 6:30 pm GMT

- New Zealand GDP at 10:45 pm GMT

It’s gonna be a big day for the markets, as investors are gearing up for the main event: the September FOMC decision!

Will they cut rates by the standard 0.25% or deliver a jumbo 0.50% rate reduction? Check out our Event Guide for the September FOMC Statement to see what number crunchers are expecting and how USD pairs could react.

Before all that, the U.K. CPI release could also make waves among GBP pairs since this inflation report is due a day ahead of the Bank of England (BOE) monetary policy decision.

Don’t forget to check out our brand new Forex Correlation Calculator!