Markets got an extra dose of risk-on vibes thanks to yet another set of stimulus measures from China.

Meanwhile, the Swiss National Bank (SNB) announced its third interest rate cut in a row and hinted at more to come.

How did your favorite asset classes perform?

Headlines:

- German GfK consumer climate index in Sept: -21.2 (-22.4 expected, -21.9 previous)

-

Chinese government unveiled additional set of stimulus measures:

- China’s leaders promised to make the “necessary fiscal spending” help hit the government’s growth targets

- China is considering injecting up to 1 trillion yuan ($142B) of capital to its biggest state banks

- State TV in China reported that Ministry of Finance and Ministry of Civil Affairs will issue living subsidies to disadvantaged groups before the National Day holiday next week

- SNB announced a “dovish cut” in lowering rates by 0.25% from 1.25% to 1.00% and keeping the door open for further easing

- Outgoing SNB Chairperson Jordan said that “further rate cuts may be necessary in order to stabilize inflation within the range of price stability in the next three months”

- Saudi Arabia will reportedly give up its $100 oil price target and raise its output along with its OPEC allies in December

- U.S. final GDP reading unchanged at 3.0% as expected for Q2 2024; final GDP price index also unchanged at 2.5%

- U.S. weekly initial jobless claims for week ending Sept 19: 218K (224K forecast, 222K previous)

- U.S. headline durable goods orders in Aug: 0.0% m/m (-2.8% expected, +9.8% previous); core durable goods orders: 0.5% m/m (0.1% expected, -0.2% previous)

- U.S. pending home sales in Aug: 0.6% m/m (0.9% expected, 0.5% previous

- Treasury Secretary and former Fed head Yellen acknowledged that there is more slack in the labor market than before

- Tokyo core CPI slowed from 2.4% y/y to 2.0% in Aug as expected

Broad Market Price Action:

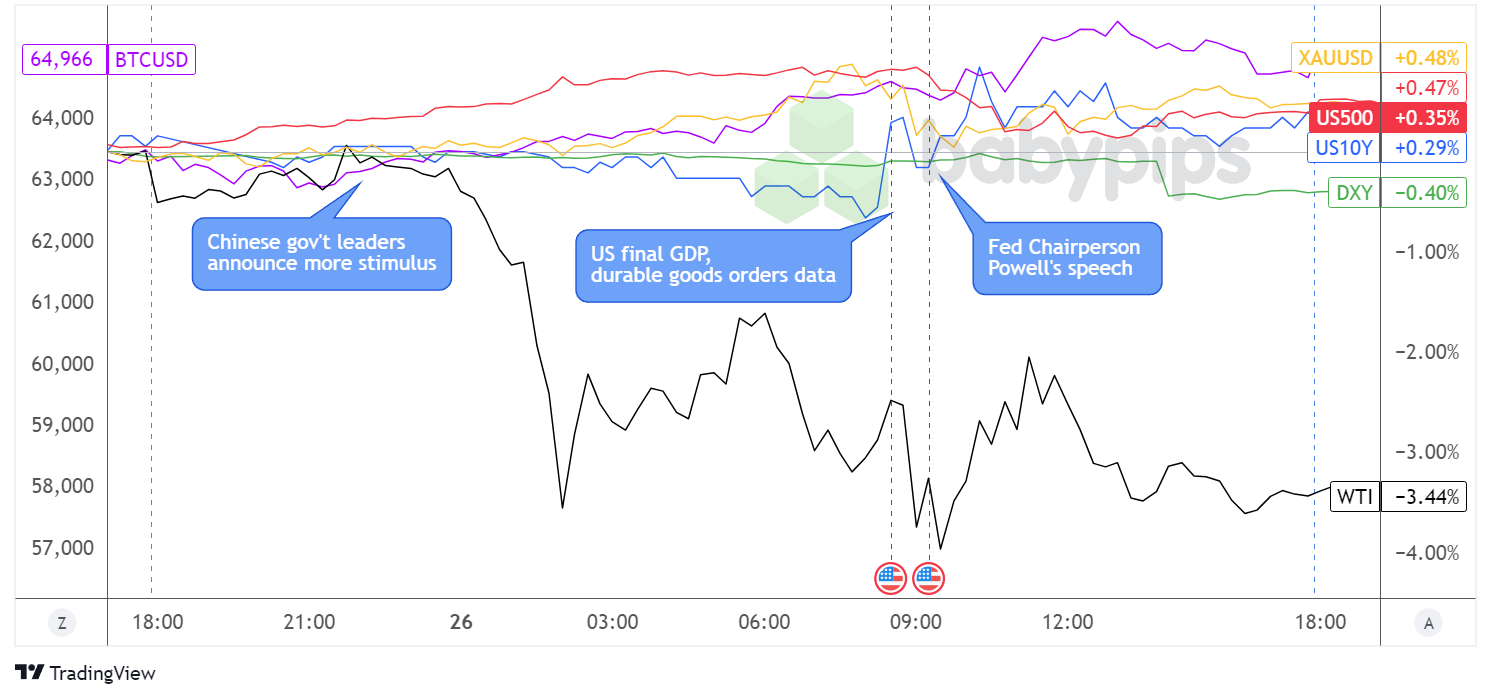

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

After yesterday’s market doubts about China following through on its stimulus plans, the Politburo came out with an announcement of concrete plans to provide fiscal support and enable the economy reach the government’s growth targets.

This sparked a pickup in risk-taking during the Asian trading session, putting equity futures on a steady climb and lifting higher-yielding assets like gold and bitcoin as well. BTC/USD went on to test the $65,000 mark later in the day while the S&P 500 and Dow surged to fresh record highs.

However, crude oil was barely able to take part in these rallies, as the energy commodity tanked on news that Saudi Arabia ditching its $100/barrel price target and will instead join the rest of its OPEC+ allies in boosting output in December. After a slight pullback during the London session, crude oil resumed its slump to end more than 3% lower for the day.

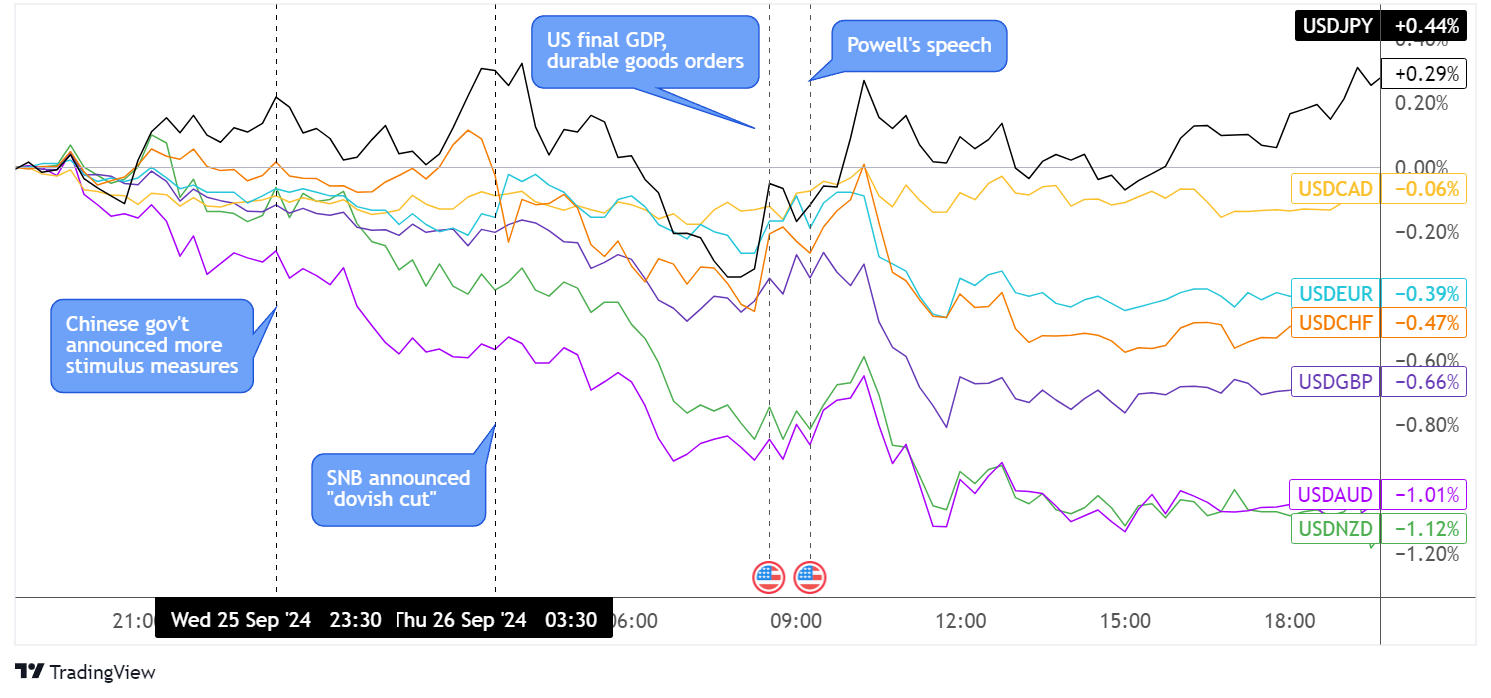

FX Market Behavior: U.S. Dollar vs. Majors:

Overlay of USD vs. Major Currencies Chart by TradingView

Forex traders were in a risk-on mood early in the day, thanks to the Chinese Politburo’s announcement of fiscal support measures and the central bank’s 0.50% reserve ratio requirement cut. The safe-haven dollar slipped as markets digested the potential impact of these aggressive stimulus efforts on the global economy while AUD and NZD took the lead.

USD/JPY managed to hold its ground, though, bouncing back in the green after a bit of a tumble during the London session. The U.S. dollar drew some support from relatively upbeat mid-tier economic data, as there were no revisions to the 3.0% growth figure for Q2 2024 and the initial jobless claims figure turned out better than expected.

The Greenback also extended its climb against most of its peers when Fed head Powell delivered some opening remarks during the Treasury Market Conference, but eventually returned its gains as risk appetite favored higher-yielding currencies. Consolidation came back in play for most of the dollar pairs before the end of the U.S. session.

Upcoming Potential Catalysts on the Economic Calendar:

- Spanish flash CPI at 7:00 am GMT

- German unemployment change at 7:55 am GMT

- Canadian monthly GDP at 12:30 pm GMT

- U.S. core PCE price index at 12:30 pm GMT

- U.S. personal income and spending data at 12:30 pm GMT

- U.S. revised UoM consumer sentiment index at 2:00 pm GMT

Data flow could be lighter than usual today, leaving traders with plenty of room to prep for the release of the U.S. core PCE price index a.k.a. the Fed’s preferred inflation measure. Expectations are for another 0.2% monthly uptick in price levels, although any major surprises could still rock the dollar’s trends.

Don’t forget to check out our brand new Forex Correlation Calculator!