Volatility was relatively subdued for most asset classes early on with the exception of crude oil, as geopolitical headlines were front and center, before risk-off flows picked up.

Meanwhile mixed U.S. leading indicators, namely the ISM manufacturing PMI and JOLTS job openings data, still wound up net positive for the dollar.

Here are the market updates you need to know!

Headlines:

- Japan’s Tankan manufacturing index for June: 13 (12 expected, 13 previous); non-manufacturing index at 34 (33 previous, 32 expected)

- Japan’s au Jibun Bank final manufacturing PMI revised higher from 49.6 to 49.7 in September

- Bank of Japan Summary of Opinions highlighted uncertainties from overseas economies

- Iran launched a missile attack on Israel in retaliation for elimination of Hezbollah leader

- Australia retail sales in Aug at 0.7% m/m (0.4% expected, previous reading upgraded from 0.0% to 0.1%)

- Australian building approvals fell by 6.1% m/m (-4.3% expected) in August, July’s uptick upgraded from 10.4% to 11.0%

- Australia’s commodity prices slipped 10.1% y/y in Sept, previous reading downgraded from 5.4% drop to 6.0% decline

- Switzerland retail sales improved from 2.9% to 3.2% (2.6% expected) in August, July’s data revised higher from 2.7%

- Swiss Procure.ch manufacturing PMI improved from 49.0 to 49.9 (47.9 expected) in September; services PMI dropped from 52.9 to 49.8, with all subcomponents losing momentum

- Euro Area Flash CPI for September 2024: 1.8% y/y as expected vs. 2.2% y/y previous

- HCOB Eurozone final manufacturing PMI revised from 44.8 to a nine-month low of 45.0 (44.8 expected) in September

- U.S. ISM manufacturing PMI for September: 47.2 (48.3 forecast; 47.2 previous); Prices index falls to 48.3 vs. 54.0; Employment Index falls to 43.9 vs. 46.0

- U.S. JOLTS job openings in Aug: 8.04M (7.64M expected, 7.71M previous)

- SNB official Martin Schlegel noted that Swiss inflation is only being driven by services sector

- New Zealand GDT auction yielded 1.2% gain in dairy prices (0.8% previous)

Broad Market Price Action:

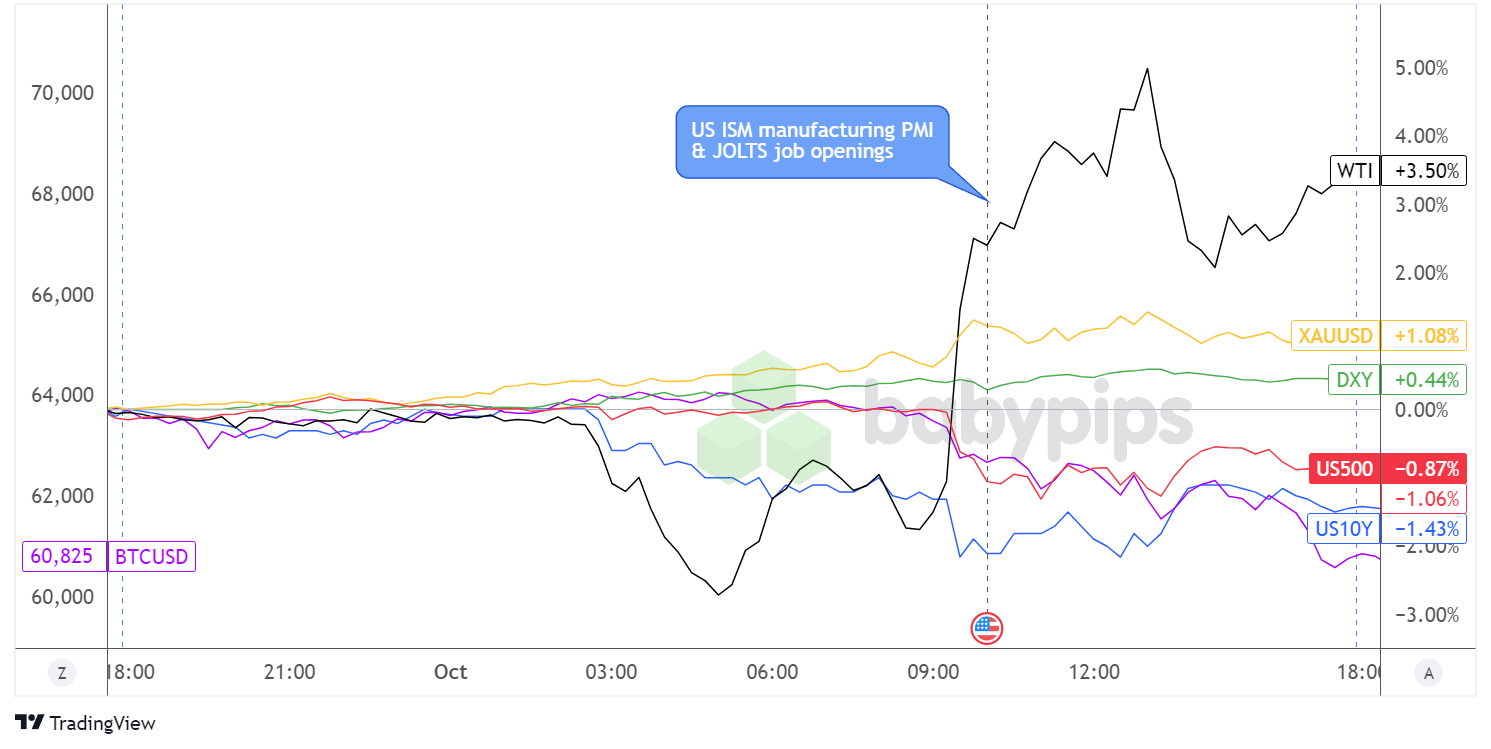

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Major asset classes started the day off in consolidation, likely due to thin liquidity during Asian market hours while Chinese banks were closed for the holiday. Risk-off flows became evident as the day went on since geopolitical tensions in the Middle East continued to escalate.

As it turned out, Iran responded with a missile attack on Israel, following the latter’s ground invasion of southern Lebanon and in retaliation for the killing of Hezbollah leaders. Crude oil, which initially chalked up losses at the start of the London session, turned sharply higher later in the day since global supply fears resurfaced.

Gold also took advantage of safe-haven demand, as the precious metal edged higher and closed at $2,663.23 per troy ounce. On the flip side, U.S. equities caved to risk aversion, with the Dow falling 200 points and the S&P and Nasdaq closing more than 1% lower, while the CBOE Volatility Index a.k.a. Wall Street’s fear gauge reached a high of 20 for the day.

FX Market Behavior: U.S. Dollar vs. Majors:

Overlay of USD vs. Major Currencies Chart by TradingView

Price action also looked mixed in the forex scene, as USD/JPY was off to a bullish start despite mostly positive economic releases from Japan. The Kiwi also chalked up losses to the dollar early on, following mixed data points from New Zealand.

Meanwhile, the Aussie caught a few bids during the Asian trading session thanks to upbeat retail sales data, which indicated stronger consumer spending growth of 0.7% month-on-month in August versus the earlier 0.1% uptick.

USD/JPY soon returned its gains towards the end of the Asian trading session while AUD/USD retreated back to its open price as well. EUR/USD, which was already on shaky ground ahead of the region’s flash CPI releases, chalked up more losses after the actual numbers reflected a slowdown in price pressures as expected.

Later on, the U.S. ISM manufacturing PMI report and JOLTS job openings data triggered a mixed reaction from the Greenback, as USD/JPY and USD/CHF carried on with their bearish trajectory while higher-yielding currencies (except for the oil-related Loonie) went on with their risk-off declines.

Upcoming Potential Catalysts on the Economic Calendar:

- Chinese banks still closed for the holiday

- OPEC-JMMC meetings going on

- U.S. ADP non-farm employment change at 12:30 pm GMT

- FOMC member Hammack’s speech at 1:00 pm GMT

- FOMC member Musalem’s speech at 2:05 pm GMT

- EIA crude oil inventories at 2:30 pm GMT

- FOMC member Bowman’s speech at 3:00 pm GMT

- FOMC member Barkin’s speech at 4:15 pm GMT

All eyes and ears could still be on leading U.S. jobs indicators as traders gear up for the NFP release on Friday. For today, we’ve got the ADP non-farm employment change report that’s expected to show a slightly higher increase in hiring for September.

Don’t forget to check out our brand new Forex Correlation Calculator!