Data flow was relatively light in the latest trading sessions, but that didn’t stop a handful of asset classes from chalking up big moves.

The U.S. dollar and Treasury yields got a bit of a boost from another upbeat leading jobs indicator while the energy commodity took cues from inventory data.

Check out these market updates!

Headlines:

- New Zealand GDT auction yielded 1.2% gain in dairy prices (0.8% previous)

- Japanese consumer confidence index in September improved from 36.7 to 36.9 (37.1 forecast)

- Japan’s new PM Shigeru Ishiba said the economy isn’t ready yet for further interest rate hikes, following a meeting with BOJ head Ueda

- Spanish unemployment change in September rose 3.2K (12.1K estimate, 21.9K previous)

- Eurozone unemployment rate unchanged at 6.4% in August as expected

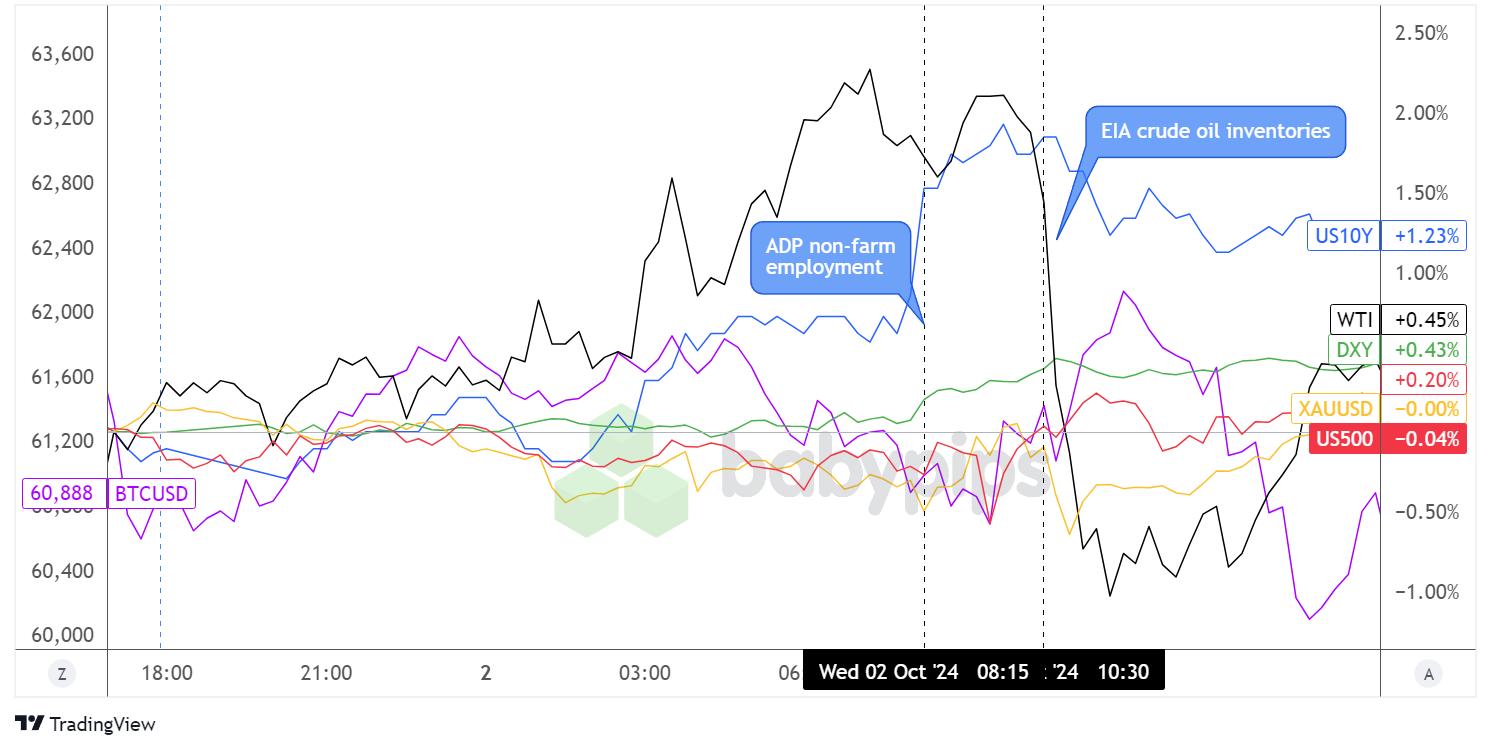

- U.S. ADP non-farm employment change in Sept: 143K (126K forecast, 103K previous)

- EIA crude oil inventories rose by 3.9 million barrels (-1.5M expected, -4.5M previous)

- FOMC official Barkin expressed support for 0.50% September rate cut since borrowing costs were out of sync with inflation and unemployment is near its sustainable level

Broad Market Price Action:

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Market correlations seemed to break down in the past trading sessions, as the lack of top-tier events left asset classes moving to their own individual catalysts.

Crude oil started off on a strong note and proceeded to bank on worsening geopolitical conflict in the Middle East, which sparked global supply concerns, throughout the Asian and London trading sessions. However, oil bulls hit a wall when the EIA report revealed a surprise build of 3.9 million barrels in stockpiles instead of the estimated reduction of 1.5 million barrels, suggesting weaker demand conditions.

U.S. equities still appeared to be bogged down by risk-off flows for the most part of the day, as investors were likely concerned about potential repercussions of geopolitical tensions on the world economy. Still, the S&P 500, Nasdaq, and Dow were all able to squeeze out small gains thanks to rising stocks of defense and energy stocks.

BTC/USD tossed back and forth between resistance around $61,600 and support near $60,500 but ended the day in the red due to dollar strength. U.S. bond yields, however, erased some of their earlier gains during the New York session shortly after the ADP numbers were printed.

FX Market Behavior: U.S. Dollar vs. Majors:

Overlay of USD vs. Major Currencies Chart by TradingView

Dollar pairs were off to a slow start, before some of its major counterparts broke off in different directions.

The yen was on shaky ground after the new Japanese Prime Minister met with BOJ Governor Ueda and declared that the economy is not yet ready for further rate hikes, leading USD/JPY to cruise higher for the most part of the day and close nearly 2% in the green.

Meanwhile, the Aussie and Kiwi snagged some gains versus the U.S. currency during Asian market hours, but eventually joined the rest of the majors in consolidation during the London session.

USD/CHF also broke away from the pack and started to climb prior to the ADP jobs report, which then ushered in a few more gains for the Greenback when the numbers turned out mostly better than expected.

Upcoming Potential Catalysts on the Economic Calendar:

- Chinese banks still closed for the holiday

- Swiss CPI at 6:30 am GMT

- Eurozone PPI at 9:00 am GMT

- U.S. Challenger job cuts at 11:30 am GMT

- U.S. initial jobless claims at 12:30 pm GMT

- U.S. ISM services PMI at 2:00 pm GMT

- U.S. factory orders at 2:00 pm GMT

- FOMC member Schmid’s speech at 2:00 pm GMT

- FOMC member Bostic’s speech at 2:40 pm GMT

Franc traders are likely gearing up for the release of Switzerland’s September CPI figure, as this could determine whether or not the SNB could carry on with another interest rate cut in their next meeting.

After that, we’ve got a couple more pieces of the U.S jobs puzzle, as the upcoming Challenger job cuts report and ISM services PMI could still shape NFP expectations and therefore dollar trends.

Don’t forget to check out our brand new Forex Correlation Calculator!