Caution ahead of Friday’s U.S. NFP release may have kept overall volatility in check, but asset-specific catalysts still brought some action to the major markets.

So, which headlines stole the spotlight on Thursday?

Let’s break it down below:

Headlines:

- BOJ member Asahi Noguchi favors adjusting monetary policies “at a slow pace” and pausing to assess the impact of the first rate hike before raising rates again

- Switzerland’s inflation fell by 0.3% m/m in September (-0.1% expected, 0.0% previous) over cheaper petrol, accommodation, and holidays. Annually, prices rose by 0.8%, the slowest increase since July 2021

- HCOB Germany final services PMI confirmed at 50.6 as expected in September; “Prices charged also rose more slowly than in August;” Employment fell at the quickest rate in more than four years”

- HCOB Eurozone final services PMI adjusted higher from 50.5 to 51.4 in September; “Output charges increased only modestly;” “Job creation was fractionally faster than in August”

- S&P Global U.K. final services PMI revised lower from 52.8 to 52.4 in September

- BOE Gov. Bailey said the central bank could be “a bit more aggressive” in cutting interest rates if inflation continues to improve

- Euro Area industrial producer prices increased by 0.6% m/m in August (0.4% expected, July reading revised lower from 0.8% to 0.7%)

- U.S. Challenger job cuts eased from 75,891 to 72,821 in September and noted that most of the hiring planned are from seasonal employers

- U.S. weekly initial jobless claims in the week ending September 28: 225K (222K expected, 219K previous)

- U.S. S&P Global final services PMI was revised lower from 55.4 to 55.2 in September

- U.S. POTUS Biden said the U.S. is discussing with Israel the possibility of striking Iran’s oil infrastructure

- U.S. ISM services PMI jumped from 51.5 to 54.9 in September, but the Employment Index contracted for the first time in three months

- U.S. factory orders dipped by 0.2% m/m (0.1% expected) in August following a 4.9% jump in July

Broad Market Price Action:

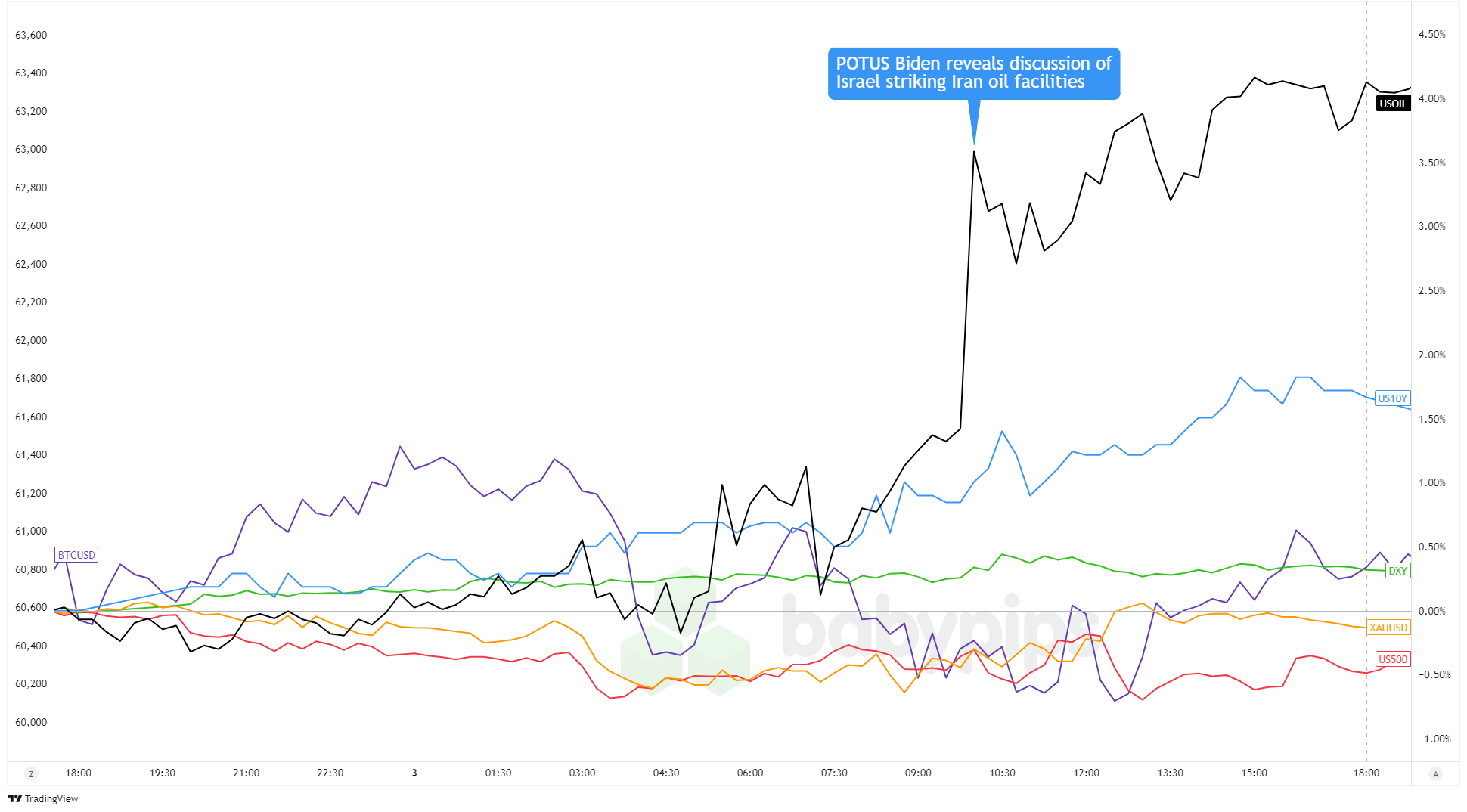

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

A lack of top-tier data releases kept the major assets in ranges early in the day.

Volatility picked up as the European session kicked off, with U.S. dollar alternatives like gold, crude oil, bitcoin, and U.S. stock futures sliding lower. Rising tensions in the Middle East, along with traders likely taking profits ahead of Friday’s U.S. NFP report, may have driven the moves.

During the U.S. session, the 10-year Treasury yield gained bullish momentum as jobs data fueled expectations for further Fed rate cuts. Crude oil also spiked after President Biden mentioned talks of Israel potentially targeting Iran’s oil infrastructure.

Gold rallied on the news, revisiting its daily highs before closing at $2,655, while WTI crude rebounded from $70.60 to hit $73.80. The 10-year Treasury yield capped the day near 3.85%, bitcoin held below $61,000, and U.S. stock indices ended slightly lower than their opening levels.

FX Market Behavior: U.S. Dollar vs. Majors:

Overlay of USD vs. Major Currencies Chart by TradingView

The U.S. dollar started strong against the yen, Swiss franc, and the Australian and New Zealand dollars, likely due to weak data from Australia and New Zealand and traders pricing in Tuesday’s stronger-than-expected ADP report.

USD/JPY initially gained on dovish BOJ speculation but lost momentum after BOJ member Noguchi clarified that policy adjustments are still possible, though at a slower pace.

Later, the British pound took a hit after BOE Governor Bailey hinted at the possibility of “more aggressive” rate cuts in a newspaper interview. Meanwhile, a weaker-than-expected Swiss CPI report increased the odds of an SNB rate cut, weighing on the franc.

The U.S. dollar held its gains against AUD, NZD, and GBP before U.S. labor market data triggered choppy price action. Ultimately, the dollar pushed toward its highs, supported by a stronger-than-expected ISM services PMI and concerns over Israel possibly targeting Iran’s oil infrastructure.

Upcoming Potential Catalysts on the Economic Calendar:

- Switzerland unemployment rate at 5:45 am GMT

- France industrial production at 6:45 am GMT

- BOE member Huw Pill to give a speech at 7:55 am GMT

- U.K. construction PMI at 8:30 am GMT

- U.S. NFP reports at 12:30 pm GMT

- FOMC member John Williams to give a speech at 1:00 pm GMT

- Canada IVEY PMI at 2:00 pm GMT

It’s NFP Friday, errbody! Price action will likely be muted ahead of the release, but we could see pockets of volatility when Switzerland drops its unemployment rate and BOE Chief Economist Huw Pill give a speech in London.

In the U.S., labor market numbers are expected to come in weaker in September, which may fuel aggressive Fed rate cut expectations. Make sure you’ve read our U.S. NFP Report Event Guide if you’re trading the release!

Don’t forget to check out our brand new Forex Correlation Calculator!