No big data? No problem!

Markets started the week on a high after Friday’s NFP report, but it wasn’t long before worries over Middle East tensions, shrinking Fed rate cut chances, and the upcoming U.S. CPI and PPI data weighed on risk assets.

Here’s how individual assets performed:

Headlines:

- Japan’s top currency diplomat Atsushi Mimura said they’ll monitor FX moves including speculative trading “with a sense of urgency”

- Germany factory orders plummeted by 5.8% m/m in August (-1.9% expected, 3.9% previous)

- U.K. Halifax house price index for September: 0.3% m/m (0.2% expected, 0.3% previous)

- Hezbollah fired rockets at Israel’s third-largest city, Haifa

- Euro Area Sentix investor confidence index improved from -15.4 to -13.8 (-14.6 expected) in October

- Euro Area retail sales accelerated from 0.0% m/m to 0.2% m/m as expected in August

- U.S. Conference Board Employment Trends Index inched lower from 109.54 to 108.48 in September, suggesting slower hiring

- FOMC non-voting member Alberto Musalem said further gradual reductions are”appropriate” but has no predetermined size or schedule for future adjustments

- FOMC non-voting member Kashkari sees neutral Fed funds rate at 3%, balance of risks shifted towards unemployment

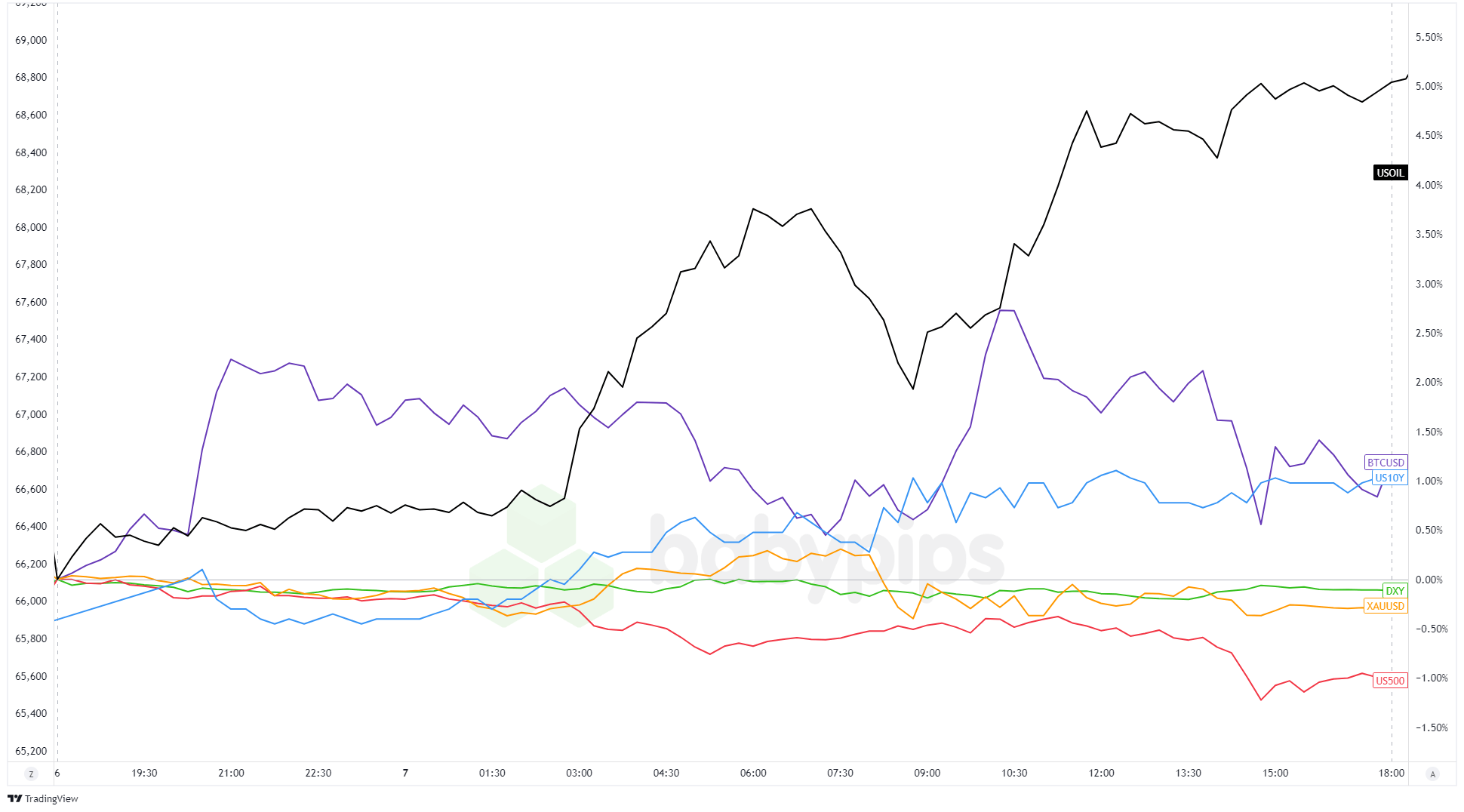

Broad Market Price Action:

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

With no major catalysts, volatility stayed low for most assets early in the week. Bitcoin (BTC/USD) was the standout, breaking above Friday’s highs and pushing toward $64,000 as the “Uptober” buzz among HODLers picked up steam.

Things got more interesting as the European session kicked off, with news of Hezbollah rockets hitting Haifa, Israel’s third-largest city, and talks of Israel expanding its offensive into Lebanon. Risk appetite took another hit with a weaker-than-expected factory report out of Germany.

WTI crude saw some action during the European and U.S. sessions, climbing steadily to close just under $77.50 at its intraday high.

In the U.S., attention shifted to the shrinking chances of aggressive Fed rate cuts after Friday’s solid NFP report. The CME FedWatch tool now shows 25bps cuts expected in both November and December, but the odds of no change in November have risen to 12.7%.

Less dovish Fed chatter pushed U.S. 10-year Treasury yields above 4.00% for the first time since August. Meanwhile, the U.S. Dollar Index stayed strong near its post-NFP highs, while gold—often seen as a dollar alternative—dropped, closing near $2,642 intraday lows. U.S. stock indices also took a hit, dragged down by uncertainty over bank earnings and the upcoming CPI and PPI reports, finishing the day in the red.

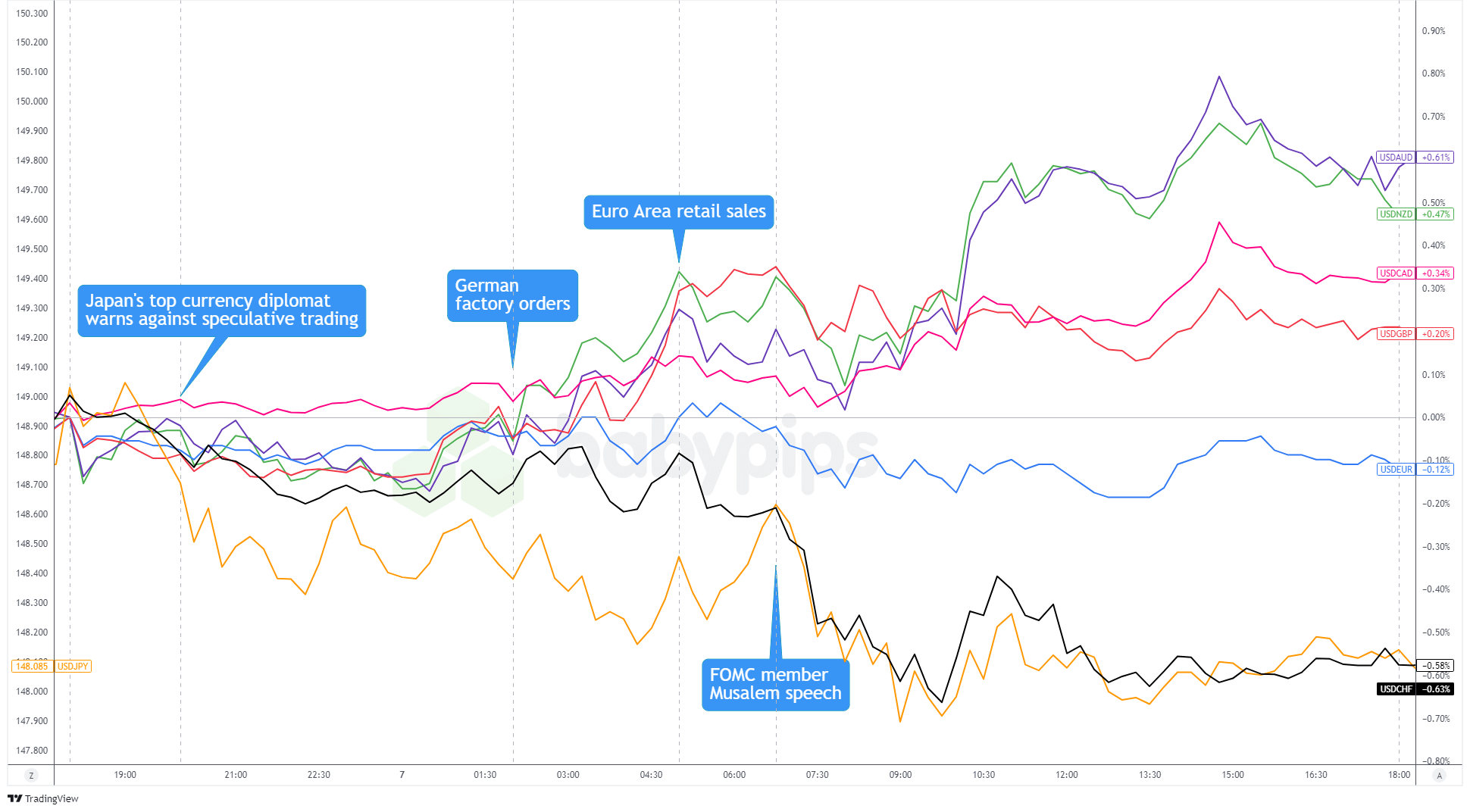

FX Market Behavior: U.S. Dollar vs. Majors:

Overlay of USD vs. Major Currencies Chart by TradingView

The U.S. dollar kicked off the week near its post-NFP highs, but pulled back a bit against the Japanese yen after some verbal intervention by Japanese officials.

Weak German factory orders and rising tensions in the Middle East sparked risk-off vibes during the European session, pushing the dollar higher against “risk” currencies like the commodity dollars and the British pound, while it slipped against other safe havens like the yen and Swiss franc.

This trend continued as the U.S. session got underway, leaving the dollar with mixed results by the end of the day.

Upcoming Potential Catalysts on the Economic Calendar:

- Germany industrial production at 6:00 am GMT

- France’s trade balance at 6:45 am GMT

- FOMC member Adriana Kugler to give a speech at 7:00 am GMT

- U.S. trade balance at 12:30 pm GMT

- Canada trade balance at 12:30 pm GMT

- FOMC member Raphael Bostic to give a speech at 4:45 pm GMT

- Bundesbank President Nagel to give a speech at 5:00 pm GMT

- FOMC member Susan Collins to give a speech at 8:00 pm GMT

- FOMC member Philip Jefferson to give a speech at 11:30 pm GMT

We’ll see a bit more mid-tier data releases as Germany drops an industrial production report while the U.S. and Canada print their latest trade data.

Unless we see geopolitical headlines, the focus may turn to central bankers and Fed policy speculations during the U.S. sessions. Keep your eyes peeled for voting FOMC members who could give us clues on the central bank’s moves in November and December!

Don’t forget to check out our brand new Forex Correlation Calculator!