A lack of top-tier data releases left the major assets room to continue pricing in existing market themes on Tuesday.

Can you guess which assets saw further adjustments?

Let’s discuss:

Headlines:

- RBA’s meeting minutes showed members prefer “sufficiently restrictive” policies until they’re more confident about inflation, but are not ruling out cash rate changes

- Japan’s average cash earnings slowed from 3.4% to 3.0% y/y as expected in August

- China’s NDRC is “fully confident” it will achieve its economic targets, adds 100B yuan from next year’s budget and another 100B yuan for key investment projects by year end

- Germany industrial production rose by 2.9% m/m in August (0.8% expected, August reading revised lower to -2.9%)

- NFIB U.S. Small Business Optimism Index for September 2024: 91.5 (92.0 forecast; 91.2 previous)

- U.S. trade deficit shrank from $78.9B to $70.4B ($70.1 expected) in August as exports (+2.0%) outpaced imports (-0.9%)

- Canada trade deficit widened from 0.3B CAD to 1.1B CAD (0.4B CAD expected) in August as exports fell on lower energy prices

- RealClearMarkets/TIPP Economic Optimism Index jumped from 46.1 to 46.9 (47.2 expected) in October

- FOMC voting member Raphael Bostic said the labor market has slowed down but is not slow, and he remains “laser-focused” against the inflation that’s still “too high”

- FOMC voting member Adriana Kugler supports further rate cuts and favors shifting the Fed’s focus from lowering inflation to supporting the labor market

- FOMC voting member Susan Collins said “further adjustments of policy will likely be needed” but not on a pre-set path

- FOMC voting member Philip Jefferson favors a meeting-by-meeting approach to rate cuts and said the Fed’s balance of risks has changed as inflation has diminished and employment risks have risen

- API: U.S. crude oil stocks rose by 10.9M barrels in the week ending October 4 (vs. 1.95M-barrel build expected, 1.5M-barrel previous decrease)

Broad Market Price Action:

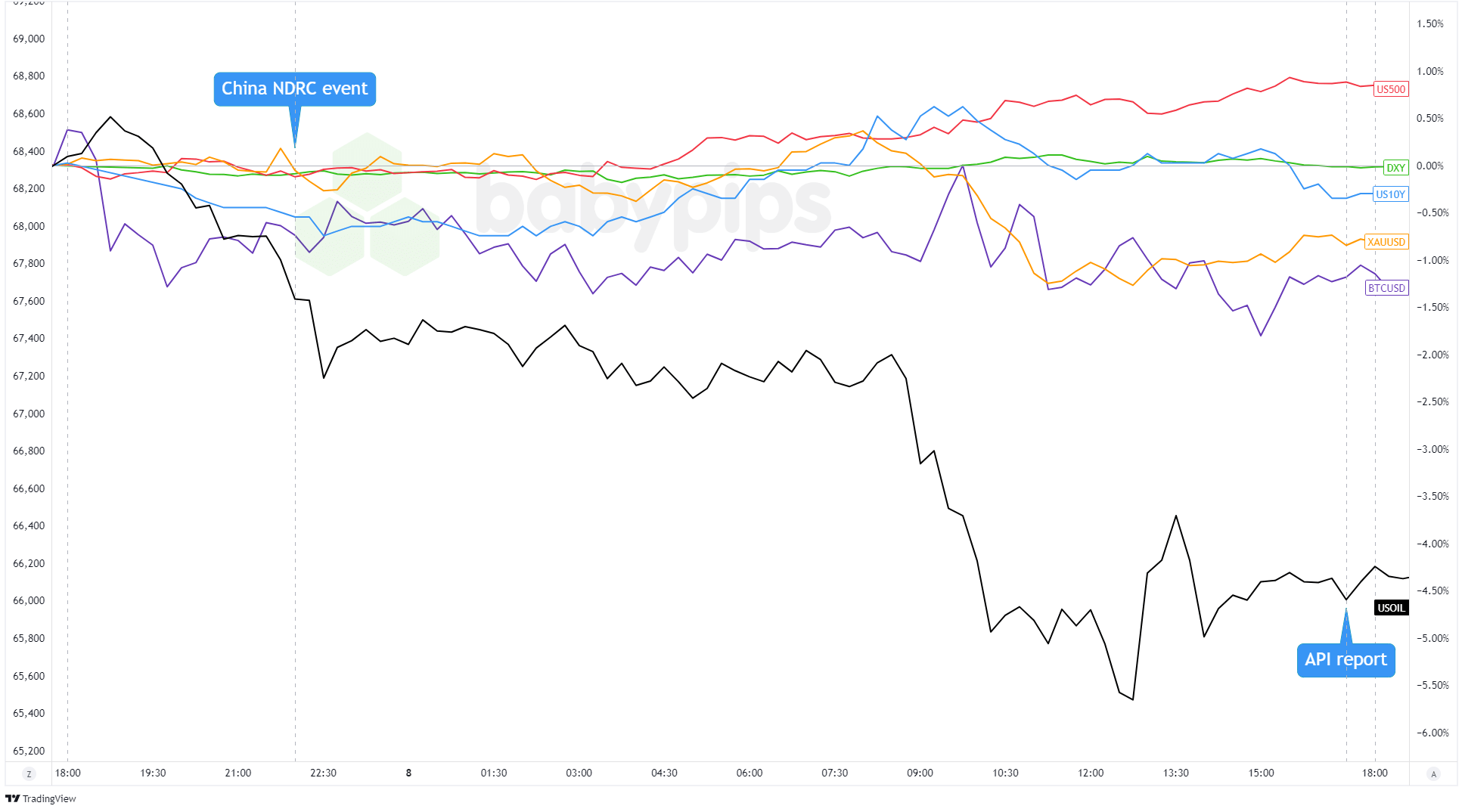

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

The markets opened on a calm note, with the RBA and China in the spotlight. China’s NDRC pledged to support the economy but didn’t give much detail. Meanwhile, the RBA’s meeting minutes revealed a preference for keeping policies tight until inflation shows clearer signs of cooling.

European equities saw some losses after China’s vague announcement, though this was softened by reduced concerns over Israel targeting Iran’s oil facilities and more ECB members supporting a potential October rate cut.

WTI crude slid in Asian trading after China’s underwhelming meeting and faced resistance at $78.00, falling further in the U.S. session as tensions in the Middle East eased.

In the U.S., attention turned to stabilizing Fed rate cut expectations after a strong NFP report, with FOMC members favoring a slower pace of easing. Gold fell from $2,650, hit lows of $2,605, and settled at $2,620. U.S. 10-year yields rose to 4.05% before dipping to 4.01%. U.S. stocks, supported by tech gains and optimism ahead of earnings, all traded higher on Tuesday.

FX Market Behavior: U.S. Dollar vs. Majors:

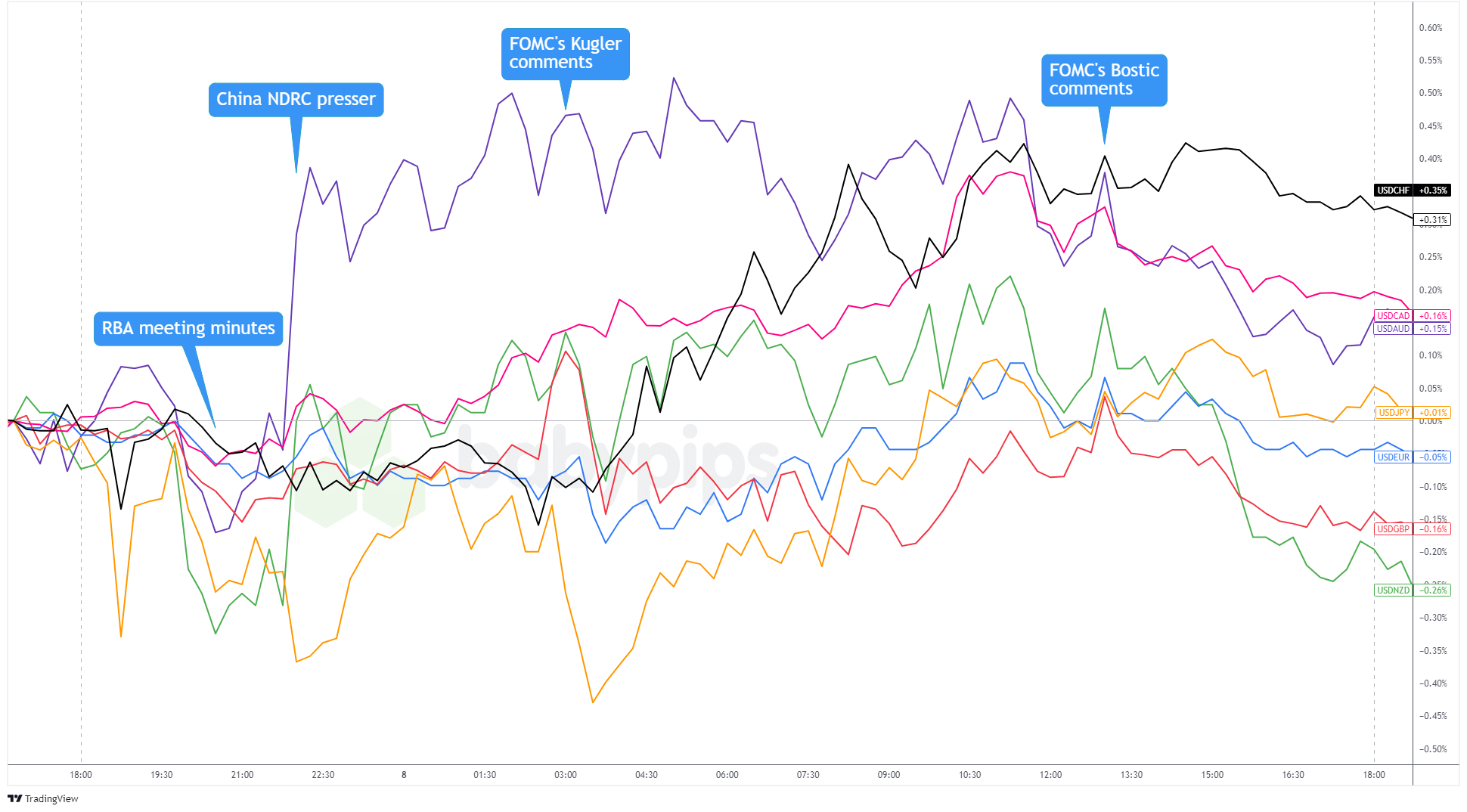

Overlay of USD vs. Major Currencies Chart by TradingView

The U.S. dollar stayed mostly flat as expectations for the Fed’s next rate cuts held steady. AUD/USD saw some gains early on thanks to the RBA’s hawkish meeting minutes but turned lower as China’s National Development and Reform Commission (NDRC) failed to detail its planned support for the economy.

The Greenback dipped briefly during early European trading after FOMC member Kugler backed further rate cuts, but it bounced back, especially against safe-haven currencies like CHF and JPY.

With no major U.S. data releases, the dollar stayed range-bound for the rest of the U.S. session. Volatility was more noticeable in the U.S. 10-year Treasury yields and equities, where the Fed’s economic confidence and fading hopes for bigger rate cuts led to lower bond yields and encouraged some risk-taking.

Upcoming Potential Catalysts on the Economic Calendar:

- Germany trade balance at 6:00 am GMT

- Japan preliminary machine tool orders at 6:00 am GMT

- FOMC member Bostic to give a speech at 12:00 pm GMT

- FOMC member Logan to give a speech at 1:15 pm GMT

- EIA crude oil inventories at 2:00 pm GMT

- FOMC member Goolsbee to give a speech at 12:00 pm GMT

- FOMC member Jefferson to give a speech at 4:30 pm GMT

- FOMC meeting minutes at 6:00 pm GMT

- FOMC member Collins to give a speech at 9:00 pm GMT

- FOMC member Daly to give a speech at 10:00 pm GMT

The FOMC gang will be under the spotlight today as more voting members are scheduled to share their two cents. But all eyes will be on the FOMC meeting minutes, which may shed more clues on the pace and magnitude of the Fed’s potential policy changes for the rest of the year.

Meanwhile, Germany’s trade balance report may shake some points out of the major assets during the European session. Don’t even think of missing these potential catalysts!

Don’t forget to check out our brand new Forex Correlation Calculator!