Market correlations seemed to be all over the place on Monday, as crude oil had a massive selloff while U.S. equities raked in decent gains.

What’s up with that?!

Read on to see the latest headlines and economic reports driving price action so far:

Headlines:

- China’s finance minister said on Saturday the government would “significantly increase” debt issuance to boost economic growth and help the property market but did not provide details

- China held large-scale military exercises surrounding Taiwan and its outlying islands to warn against “independence forces” on the Beijing-claimed island

- OPEC further trimmed outlook for growth in oil demand forecast for 2024 by 106,000 barrels a day to 1.9 million barrels a day and lowered its forecast for 2025 by 102,000 barrels a day

- Israel PM Netanyahu tells U.S. he’s willing to strike military rather than oil or nuclear facilities in Iran

- China’s CPI unexpectedly eased from 0.6% y/y to 0.4% y/y (0.6% expected) while producer price deflation deepened from -1.8% y/y to -2.8% y/y (-2.5% expected) in September

- BusinessNZ New Zealand services index is unchanged at 45.7 in September; Employment plummeted from 49.4 to 45.7

- New Zealand retail purchases on credit and debit cards fell by another 0.7% q/q in Q3 after a 2.5% decline in the previous quarter

- Chinese trade surplus narrowed from 91 billion USD to 81.7 billion USD in Sept (91.5B USD forecast) as exports rose 2.4% while imports grew 0.2%

- U.S. markets closed in observance of Columbus Day, Canadian markets closed for Thanksgiving Day

- FOMC non-voting member Neel Kashkari said “further modest reductions” is likely and will be appropriate in the coming quarters

- FOMC voting member Christopher Waller thinks the Fed should “proceed with more caution on the pace of rate cuts than was needed at the September meeting”

Broad Market Price Action:

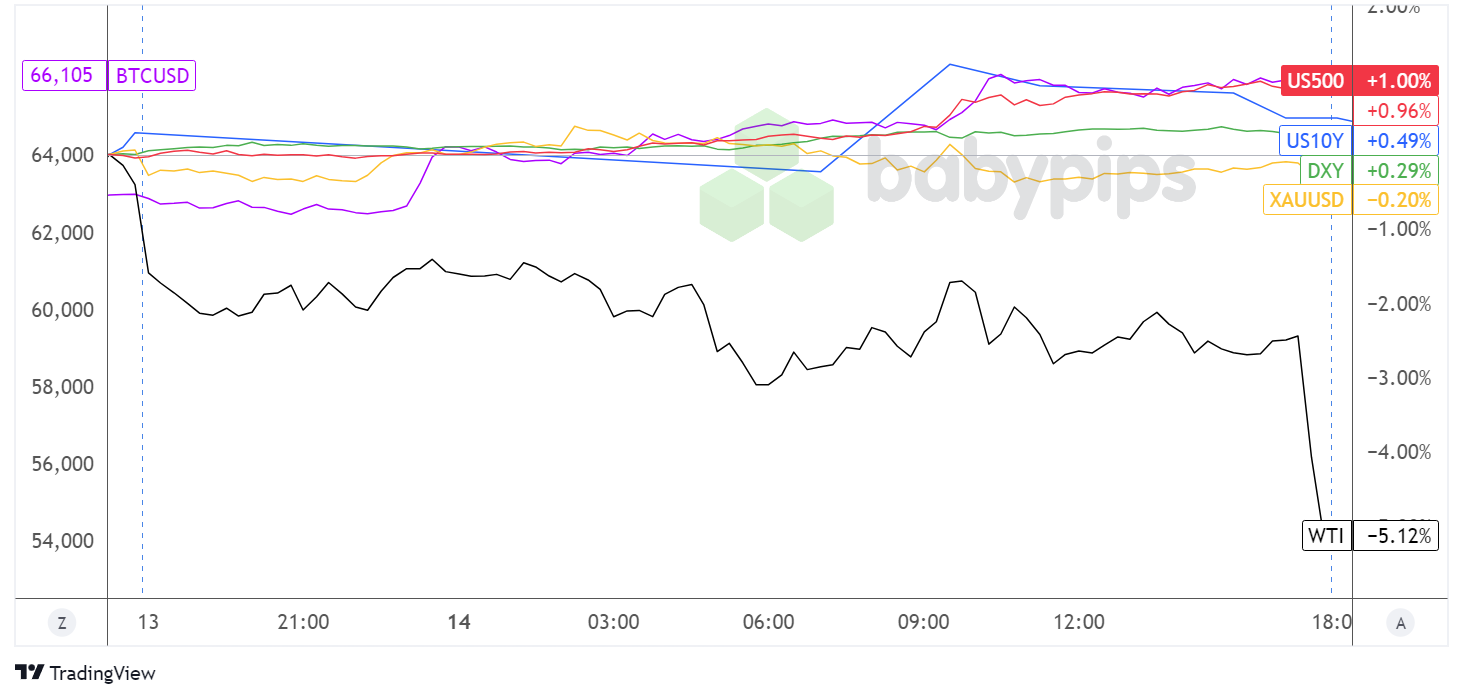

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Not even the market holidays in the U.S. and Canada were enough to stop major asset classes from making big moves on Monday!

Crude oil started off on weak footing, reacting to weekend updates related to the commodity’s demand outlook. For one, the OPEC announced downgrades to its global consumption forecasts for this year and the next, its third cut so far this year. To top it off, Chinese authorities once again failed to impress the markets with their stimulus plans since they failed to provide concrete details.

The energy commodity cruised sideways as the Asian session went on, before taking another tumble as London markets opened and chalking up an even deeper dive towards the end of the U.S. session.

In contrast, U.S. equity indices were able to get a boost from a strong showing in the tech sector, led by Nvidia shares which closed at record highs. The S&P 500 and Dow Jones reached new record highs, gaining 0.77% and 0.47% respectively while BTC/USD also caught some risk-on moves as it climbed back above $66,000.

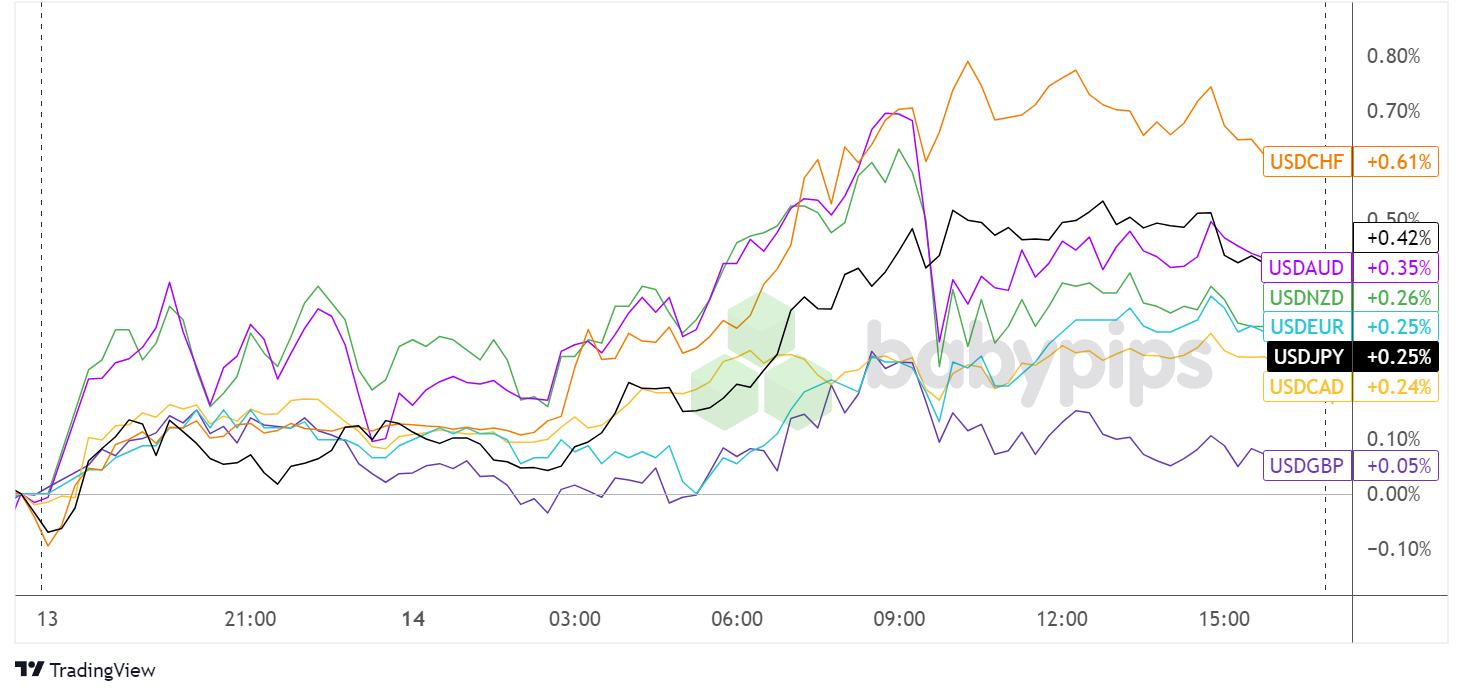

FX Market Behavior: U.S. Dollar vs. Majors:

Overlay of USD vs. Major Currencies Chart by TradingView

The U.S. dollar was off to a running start, likely taking advantage of risk-off vibes from weekend headlines. Apart from another lackluster reaction to China’s stimulus announcement, investors remained on edge while keeping an eye out for Israel’s attacks, even though officials said they will not be targeting Iran’s oil facilities.

AUD/USD and NZD/USD saw steep losses from the get-go and continued to edge lower for the most part of the day, as China’s inflation reports printed on Sunday fell short of estimates. This was followed by a downbeat trade balance, which indicated a slower than expected pickup in import and export activity.

Most major currencies were also on weaker footing versus the dollar throughout the day, except for sterling which managed to trim its losses before the end of the New York session. USD/CHF raked in the most gains at 0.61% as the franc was likely weighed down by the downbeat Swiss PPI release.

Upcoming Potential Catalysts on the Economic Calendar:

- U.K. employment data at 6:00 am GMT

- German and eurozone ZEW economic sentiment index at 9:00 am GMT

- Canadian CPI figures at 12:30 pm GMT

- U.S. Empire State manufacturing index at 12:30 pm GMT

- FOMC member Daly’s speech at 3:30 pm GMT

- FOMC member Kugler’s speech at 5:00 pm GMT

- New Zealand quarterly CPI at 9:45 pm GMT

There’s no shortage of potential catalysts on today’s economic schedule, as volatility could be elevated for the pound, Loonie, dollar and Kiwi!

Keep an eye out for the release of the U.K. labor market figures, followed by Canada’s inflation report and the U.S. Empire State manufacturing index. After that, New Zealand has its quarterly CPI update coming up, possibly affecting RBNZ policy expectations.

Don’t forget to check out our brand new Forex Correlation Calculator!