Some risk-off flows were seen in the markets, as crude oil continued to sink and U.S. equity indices ended in the red.

Meanwhile, volatility picked up in the forex arena due to top-tier releases, including the U.K. jobs report and Canada’s CPI readings.

Here’s what you need to know!

Headlines:

- Japanese industrial production for August unchanged at -3.3% month-on-month as expected

- German wholesale price index sank 0.3% m/m vs. expected 0.2% uptick, previous 0.8% decline

- U.K. claimant count change at 27.9K in Sept (20.2K forecast, previous reading revised from 23.7K to 0.3K), jobless rate fell from 4.1% to 4.0% (4.1% forecast) and average earnings index slowed from upgraded 4.1% to 3.8% for the three-month period ending in Aug

- German ZEW economic sentiment index improved to 13.1 in Sept (10.2 expected, 3.6 previous); eurozone ZEW economic sentiment index at 20.1 (16.9 expected, 9.3 previous)

- Eurozone industrial production rose 1.8% m/m in August (1.8% expected, previous reading downgraded from -0.3% to -0.5%)

- Canadian headline CPI down 0.4% m/m in Sept (-0.2% expected, -0.2% previous); annual reading down from 2.0% to 1.6% (2.0% expected); core CPI at 0.0% (0.1% expected, -0.1% previous)

- Presidential candidate Donald Trump defended his plans to significantly raise tariffs on foreign imports, citing trade with Mexico, Europe, and China

- U.S. Empire State manufacturing index at -11.9 in Oct (+3.4 expected, +11.5 previous)

- New Zealand GDT auction yielded 0.3% drop in dairy prices (+1.2% previous)

- FOMC official Daly assured that monetary policy is still restrictive and working to lower inflation, 3% rate may be around neutral

Broad Market Price Action:

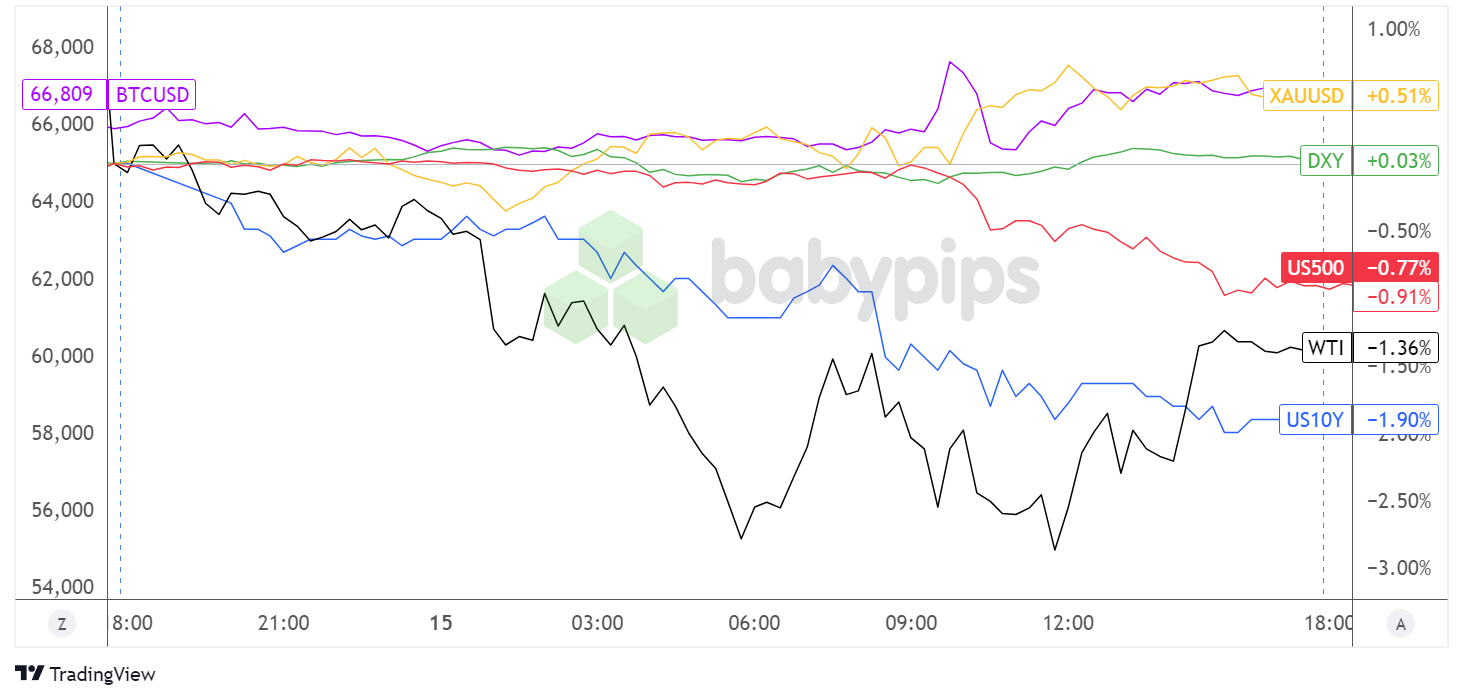

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

While most asset classes started the day on a chill note, WTI crude oil was eager to pick up where it left off the previous day by sliding throughout the Asian session. Israel’s assurances about avoiding any strikes on Iran’s oil facilities appear to be soothing global oil supply concerns despite elevated geopolitical tensions.

Treasury yields also seemed unstoppable in their decline, as government bonds picked up on risk-off flows and downbeat global inflation reports. U.S. equity indices ended the day in the red, dragged lower mostly by weak earnings from chip company ASML and its grim outlook on Chinese demand.

On the flip side, gold was able to bank on its safe-haven appeal as the precious metal closed 0.51% higher for the day, even with the dollar strengthening as well.

FX Market Behavior: U.S. Dollar vs. Majors:

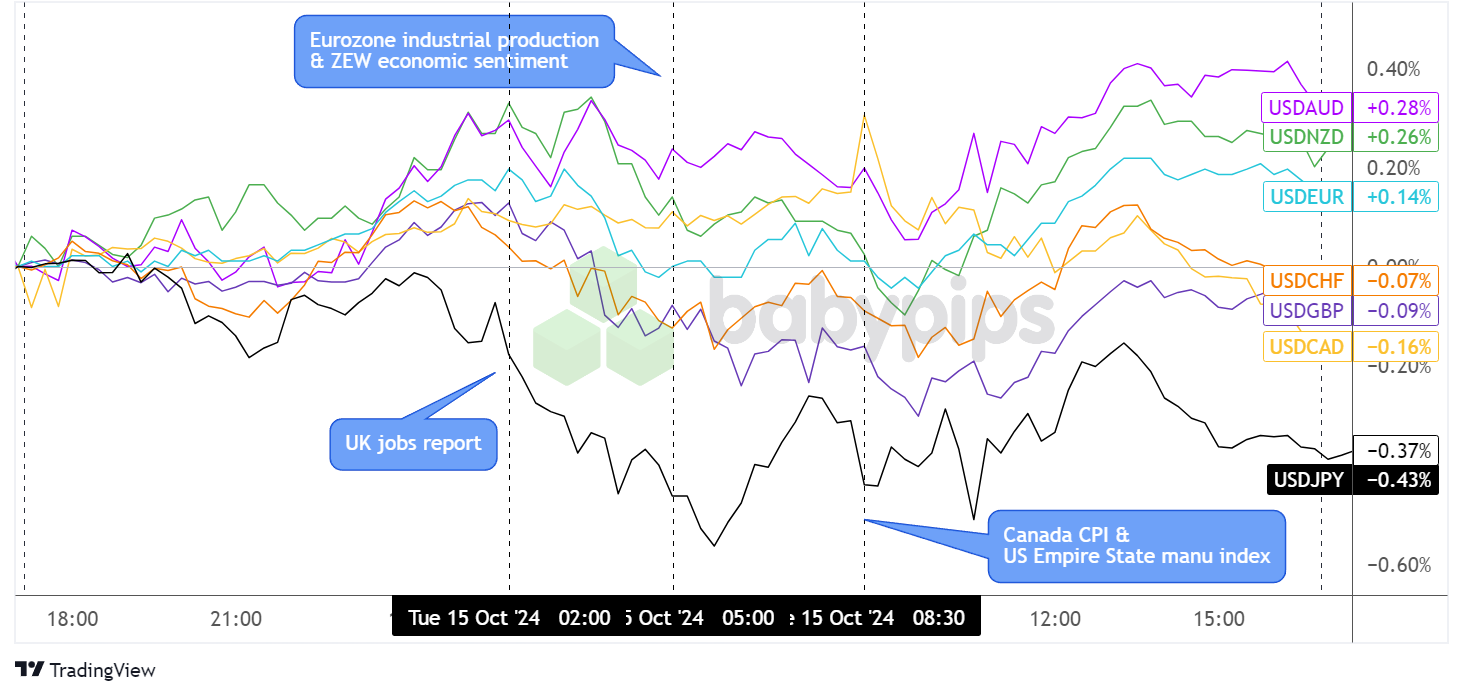

Overlay of USD vs. Major Currencies Chart by TradingView

Major pairs took off mixed during the early Asian session, but the U.S. dollar eventually found its groove and saw a bit of uniform price action later in the day.

Some risk-off vibes coming from market uncertainty surrounding geopolitical tensions in the Middle East lifted the safe-haven currency versus its higher-yielding counterparts while the yen was able to put up a pretty decent fight.

The U.S. currency took a turn lower during the early London market hours, giving up ground even against sterling despite downbeat U.K. jobs data and raking in steady gains versus the euro on upbeat industrial production and ZEW economic sentiment survey results.

The Greenback took a few more hits after seeing a downbeat Empire State manufacturing index, but USD/JPY and USD/CHF found support at intraday lows. USD/CAD popped sharply higher on weaker than expected Canadian inflation data which bolstered expectations for more BOC cuts.

Upcoming Potential Catalysts on the Economic Calendar:

- U.K. CPI report at 6:00 pm GMT

- U.K. PPI input and output data at 6:00 pm GMT

- Canada’s manufacturing sales at 12:30 pm GMT

- ECB head Lagarde’s testimony at 6:45 pm GMT

All eyes and ears could be on sterling for today, as the U.K. economy gears up to print its September CPI figures. Keep an eye out for any surprises that could influence policy expectations for the Bank of England (BOE)!

Don’t forget to check out our brand new Forex Correlation Calculator!