Major currencies and asset classes seem to be taking cues from their own individual catalysts, with U.K. inflation data and the “Trump trade” taking center stage.

Crude oil had its usual bearish run, although the energy commodity managed to limit its losses in the past sessions compared to its steep selloff earlier in the week.

Here are the updates driving price action lately.

Headlines:

- New Zealand Q2 2024 CPI at 0.6% (0.7% expected, 0.4% previous), annual reading down from 3.3% to 2.2% to mark the first time it reached the RBNZ target range in over 3 years

- BOJ board member Adachi said that conditions are already in place to normalize monetary policy, but emphasized that the central bank must raise interest rates at a “very moderate” pace

- Japan August core machinery orders fell by 1.9% m/m in August (0.1% expected, -0.1% previous)

- U.K. annual headline CPI eased from 2.2% to 1.7% (1.9% expected); Core CPI slowed from 3.6% to 3.2% (3.4% expected)

- U.K. monthly PPI input prices fell faster, from -0.3% to -1.0% (-0.5% expected) in September; PPI output prices declined further from -0.3% to -0.5% (-0.3% expected)

- U.K. retail price index eased from 3.5% y/y to 2.7% y/y (3.1% expected) in September

- U.K. house price index accelerated from 1.8% y/y to 2.8% y/y (2.5% expected) in September

- U.S. import prices down 0.4% m/m in Sept vs. expected 0.3% decline, previous 0.2% dip

Broad Market Price Action:

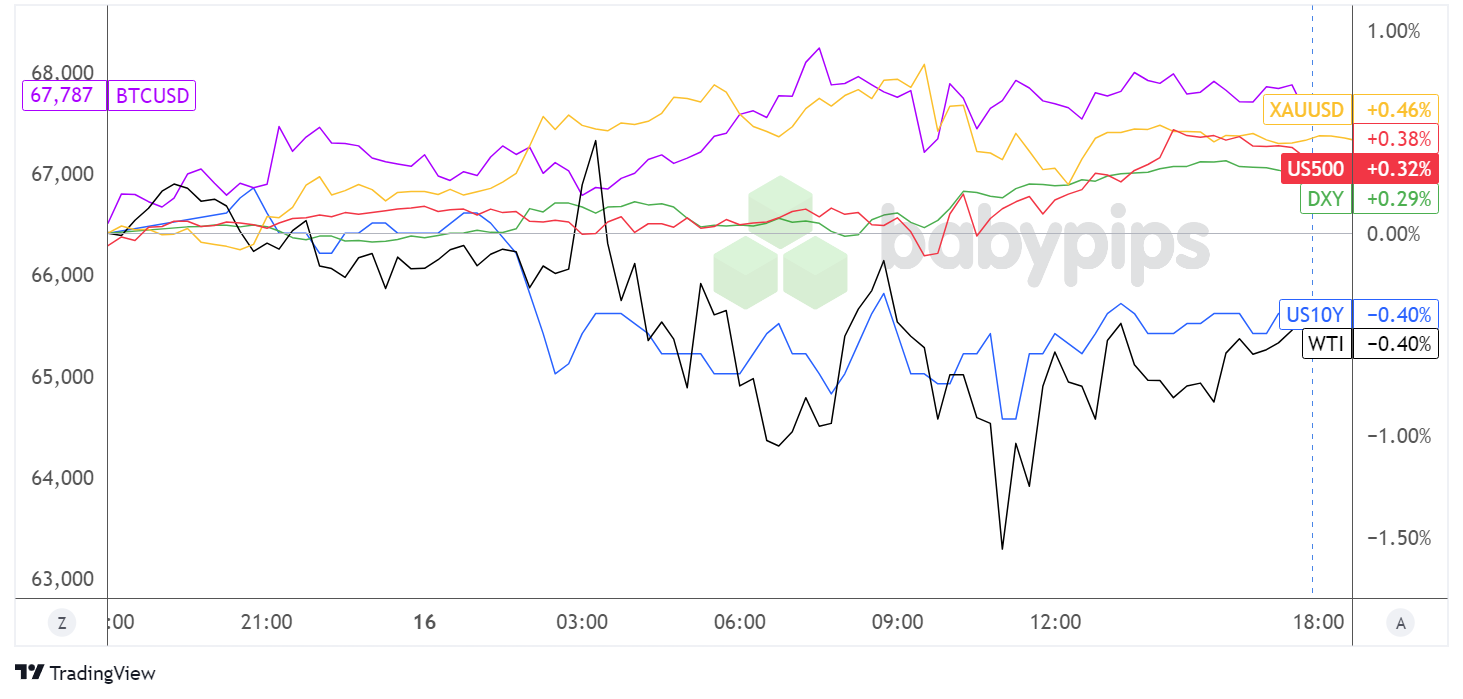

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Major asset classes started the day off by diverging in different directions, with crude oil ready to carry on with its slide while gold and bitcoin advanced.

Although investors continue to monitor geopolitical tensions in the Middle East, oil traders still seem to be easing up on global supply concerns after Israel recently pledged to avoid attacking Iran’s production facilities.

Still, WTI crude oil pulled up briefly during the start of the London session after the API reported a draw of 1.58 million barrels in stockpiles, before resuming its tumble then trimming its losses to just 0.40% for the day.

Meanwhile, U.S. equity indices found themselves slightly in the green, thanks to positive earnings data from Morgan Stanley, Abbott, and Nvidia. Gold prices remained elevated for the most part of the day, likely reflecting unease in the markets that also lifted other safe-havens like government bonds and the U.S. dollar.

FX Market Behavior: U.S. Dollar vs. Majors:

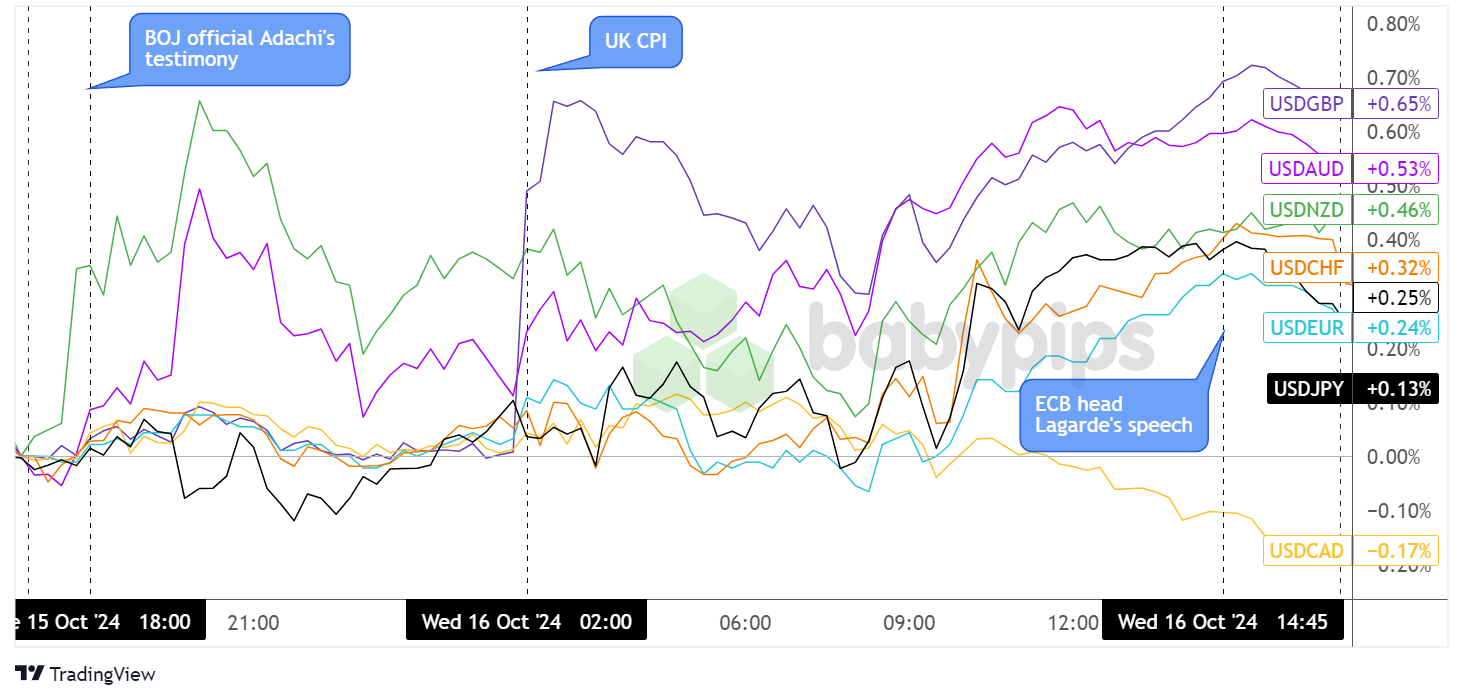

Overlay of USD vs. Major Currencies Chart by TradingView

Price action among major currency pairs also diverged from the get-go, with the Kiwi chalking up steep losses after seeing weaker than expected quarterly CPI data from New Zealand. Its buddy the Aussie trailed behind, also dragged lower by fading Chinese stimulus hopes.

On the flip side, the Japanese yen drew a bit of support from hawkish remarks by BOJ official Adachi who noted that economic conditions are in place to normalize policy (a.k.a. hike interest rates) but that they plan on tightening gradually.

During the London session, sterling tumbled across the board upon seeing the U.K. inflation figures come in the red, as weaker than expected CPI and PPI data increased the odds of further BOE rate cuts. After a bit of profit-taking, the pound remained heavy throughout the day, leading Cable to close 0.65% lower, followed by NZD/USD and AUD/USD which ended roughly 0.50% in the red.

The dollar also ended in the green against the rest of its counterparts, as opinion polls have been showing rising odds of a Trump presidential win, with the exception of the Loonie as USD/CAD closed 0.17% lower.

Upcoming Potential Catalysts on the Economic Calendar:

- Japanese tertiary industry activity index at 4:30 am GMT

- Swiss trade balance at 6:00 am GMT

- Eurozone final headline and core CPI at 9:00 am GMT

- ECB monetary policy decision at 12:15 pm GMT

- U.S. headline and core retail sales at 12:30 pm GMT

- U.S. initial jobless claims at 12:30 pm GMT

- U.S. Philly Fed index at 12:30 pm GMT

- ECB head Lagarde’s press conference at 12:45 pm GMT

- U.S. industrial production and capacity utilization at 1:15 pm GMT

- EIA crude oil inventories at 3:00 pm GMT

- FOMC member Goolsbee’s speech at 3:00 pm GMT

It’s a busy economic schedule today, with the European Central Bank’s (ECB) monetary policy decision in the spotlight!

Expectations for an interest rate cut have been priced in for a while now, but keep an eye out for any surprises or change in rhetoric that could influence future policy expectations and EUR trends.

After that, stay on your toes for USD volatility right around the release of the U.S. retail sales and initial jobless claims data.

Don’t forget to check out our brand new Forex Correlation Calculator!