There were no major data releases, which left the major assets exposed to current market themes and increasing concerns about the U.S. economy.

How did your closely watched assets trade in the last trading sessions?

Let’s discuss them below:

Headlines:

- ECB member Olli Rehn said disinflaiton in the Euro Area is “well on track,” but that the growth outlook has weakened and could increase disinflationary pressures

- ECB member Robert Holzmann noted that “the deflationary process was much faster than we had thought,” adding that subsequent rate cuts will follow “not too far” into the future

- ECB member Mario Centeno called for a “gradual, steady and predictable reduction in interest rates” but won’t rule out larger cuts if the jobs market weakens

- ECB President Lagarde is confident inflation will hit target in 2025, and shared that the policy direction is “clear” but the pace of further cuts and the neutral rate is not

- BOE member Megan Greene believes interest rates will settle “a bit higher” than pre-pandemic levels

- Canada industrial product price index for September: -0.6% m/m (-0.4% expected, August reading revised lower from to -0.8% -0.9%); Raw materials price index fell by 3.1% m/m (-1.7% expected, -3.0% previous)

- U.S. Richmond manufacturing index for October: -14 (-19 expected, -21 previous); Employment improved from -22 to -17; Prices Received rose from 1.57 to 1.71

- API: U.S. crude oil inventories rose by 1.643M barrels vs 0.7M increase expected for the week ending Oct 18

- IMF kept its 2024 growth forecasts unchanged, and slightly downgraded 2025 GDP estimates. It also upgraded U.S. and U.K. projections, while downgrading growth expectations for China, Eurozone, and Japan

Broad Market Price Action:

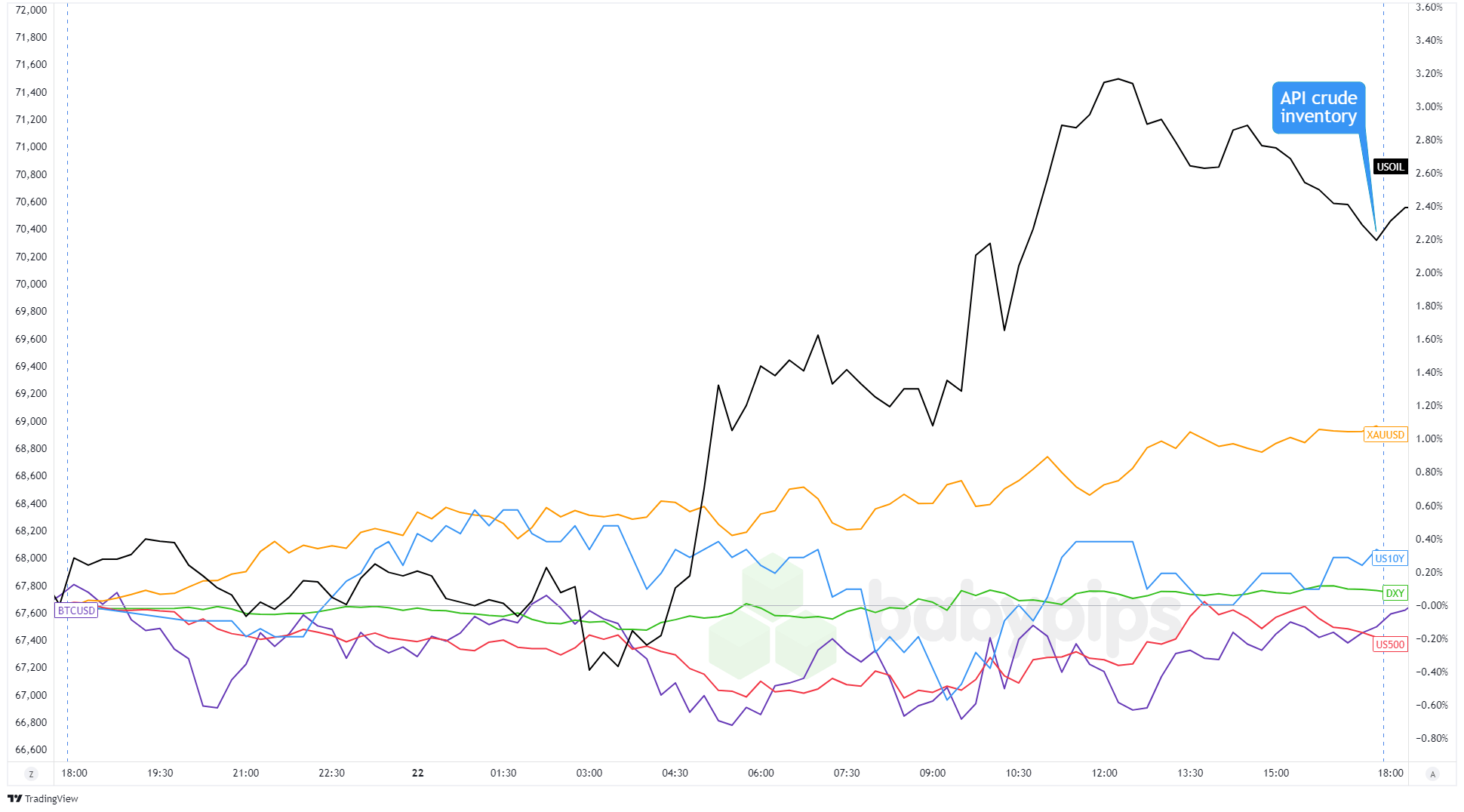

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

With no fresh catalysts in sight, major assets were left to ride the waves of existing market themes and concerns about the U.S. economy.

U.S. 10-year bond yields dipped to 4.17% but bounced back to the weekly high of 4.20% as the market tried to balance the Fed’s rate cut timeline with worries over the U.S. deficit ahead of the Presidential elections. Meanwhile, the U.S. dollar took a breather from its recent climb, which likely gave gold a boost. Prices hit a new all-time high, approaching $2,750, driven by Middle East tensions and expectations of lower global interest rates.

U.S. stock futures took an early hit, but the mood eventually shifted, and they closed mostly flat. Bitcoin, on the other hand, stayed stuck below $67,750.

Over in the oil markets, crude got a lift from optimism around China’s recent rate cut and the low chances of a ceasefire in Gaza, even after U.S. Secretary of State Antony Blinken’s visit to Israel. WTI surged past $70.00, testing $72.00 before settling at $71.30.

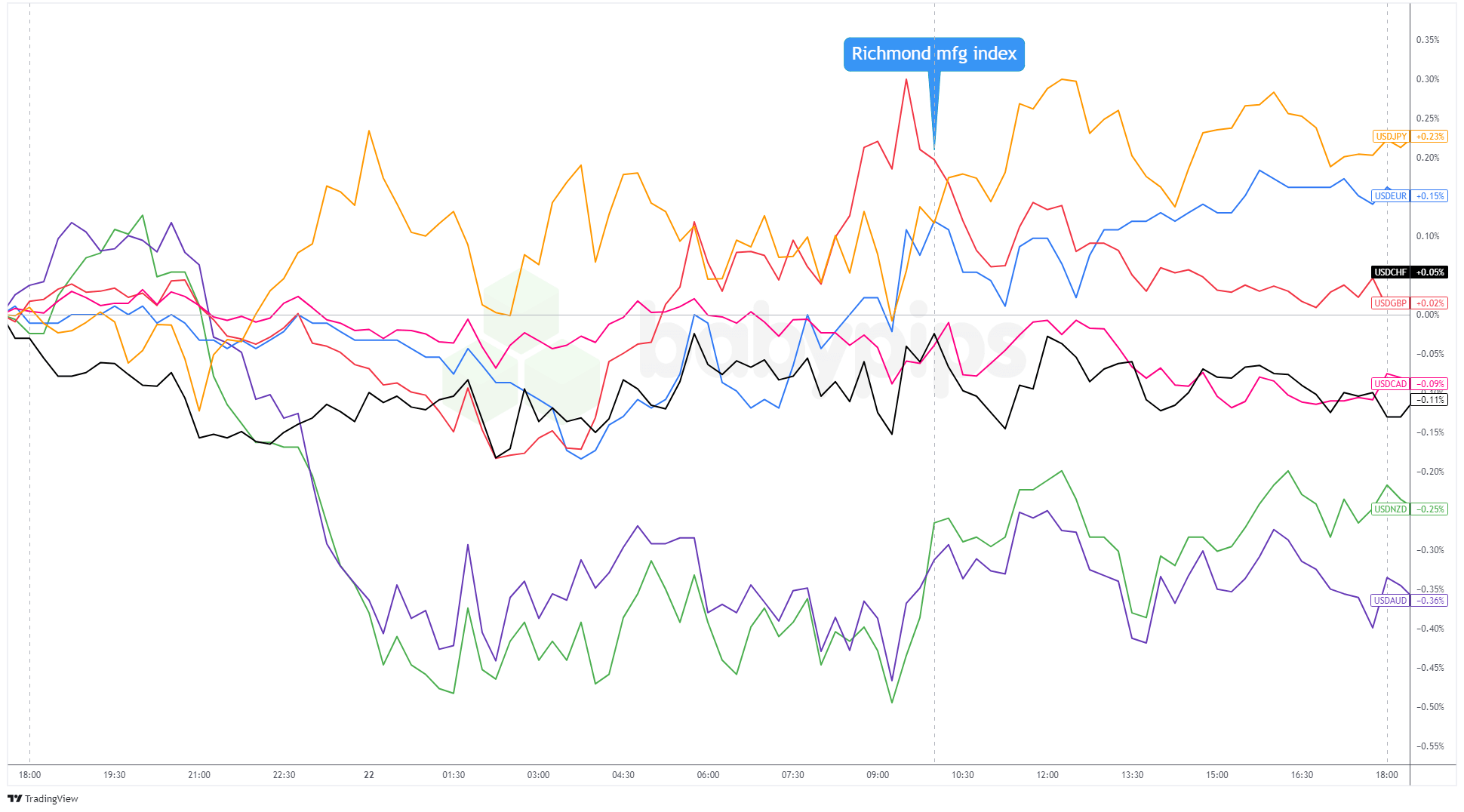

FX Market Behavior: U.S. Dollar vs. Majors:

Overlay of USD vs. Major Currencies Chart by TradingView

The U.S. dollar held near its weekly highs, thanks to the lack of fresh catalysts, higher U.S. bond yields, and ongoing concerns about global growth and geopolitical risks, which kept demand for safe havens strong. The dollar also got a boost as Japanese officials stayed quiet, even as USD/JPY flirted with the 151.00 level.

The Greenback would’ve ended the day stronger across the board, but it lost some ground to the Australian and New Zealand dollars during the Asian session. Optimism over China’s latest stimulus measures lifted risk sentiment, leaving the USD in the red against the Aussie and Kiwi, and slightly lower against stronger currencies like the Swiss franc and Canadian dollar.

Upcoming Potential Catalysts on the Economic Calendar:

- BOE member Breeden to give a speech at 1:00 pm GMT

- FOMC member Bowman to give a speech at 1:00 pm GMT

- BOC policy decision at 1:45 pm GMT; Presser to follow at 2:30 pm GMT

- ECB President Lagarde to give a speech at 2:00 pm GMT

- U.S. existing home sales at 2:00 pm GMT

- EIA crude oil inventories at 2:30 pm GMT

- FOMC member Barkin to give a speech at 4:00 pm GMT

- RBNZ Gov. Orr to give a speech at 5:00 pm GMT

- BOE Gov. Bailey to give a speech at 6:45 pm GMT

- Australia’s flash manufacturing and services PMIs at 10:00 pm GMT

Traders are in for a BUSY day as the Bank of Canada (BOC) drops its October policy statement! And if that’s not enough central bank activity for ya, Central bank Governors Lagarde, Bailey, and Orr will also take center stage and share potentially market-moving sentiments.

Meanwhile, the U.S. existing home sales report and speeches by FOMC members Bowman and Barkin could inspire increased volatility as traders eye the U.S. dollar’s recent strength.

Don’t forget to check out our brand new Forex Correlation Calculator!