The major assets were all over the charts on Wednesday. U.S. Treasury yields continued to rise, boosting the U.S. dollar higher and dragging gold prices lower.

Risk assets like equities and bitcoin weakened, while crude oil prices failed to make new weekly highs.

Which catalysts moved the major assets around yesterday? Let’s discuss:

Headlines:

- BOC Cuts Rates by 50bps, Now Aims to Stick the Landing on Inflation Control

- ECB President Lagarde said she’s “satisfied” with the inflation progress, but warned that they need to be “cautious” and look to data for future decisions

- Euro Area consumer confidence for October: -13 (-12 expected, -13 previous)

- U.S. existing home sales for September: 3.84M (3.88M expected and previous)

- EIA: U.S. crude oil inventories increased by 5.5M barrels in the week ending October 18 against 0.9M increase expectations and last week’s 2.2M-barrel draw

- RBNZ Gov. Orr hinted at a more measured pace of easing, saying that they can be more “incremental” amidst “calmer waters”

- BOE Gov. Bailey said disinflation is happening faster than officials had expected but repeated his concerns about sticky high services inflation

- Fed’s Beige Book report showed flat or slightly declining growth in September

Broad Market Price Action:

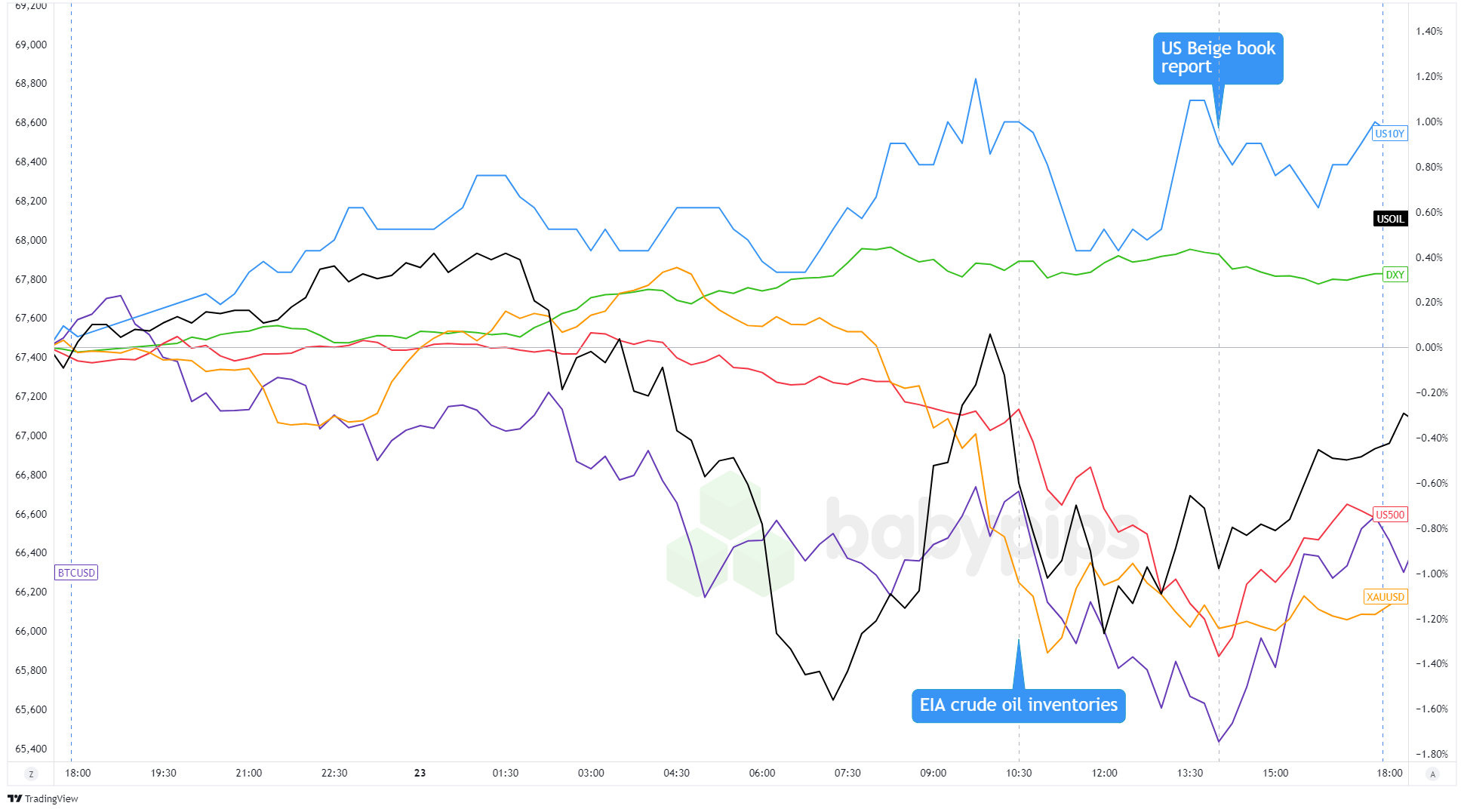

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

With no fresh catalysts during the Asian session, major assets stayed range-bound early on. Volatility picked up around the European session, as rising bond yields and ongoing geopolitical risks kept traders cautious and limited risk-taking.

Crude oil prices began slipping from the $71.50 level, while bitcoin, after failing to break past $67,750, started its downswing toward $65,250 lows.

In the U.S., a mix of election uncertainty, bearish corporate news from McDonald’s (MCD), Coca-Cola (KO), and Apple (AAPL), along with fears of higher inflation and interest rates if Trump wins, led to more profit-taking in equities and pushed U.S. 10-year yields higher.

The US10Y hit a three-month high near 4.26%, the U.S. dollar continued its weekly rally, and safe haven gold dropped from $2,760 highs to $2,712 before settling at $2,715.

FX Market Behavior: U.S. Dollar vs. Majors:

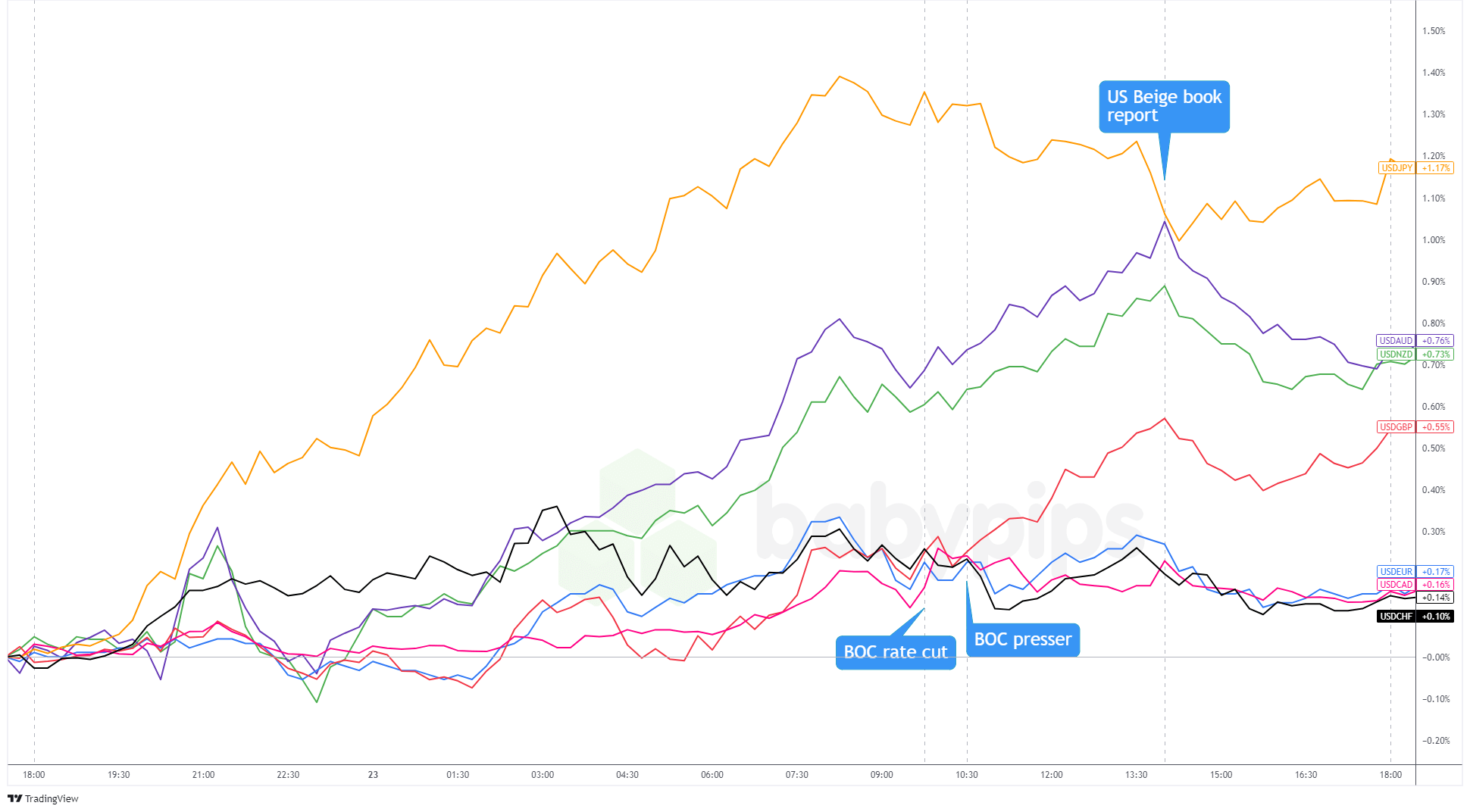

Overlay of USD vs. Major Currencies Chart by TradingView

The U.S. dollar kept its winning streak going, benefiting from risk aversion and higher U.S. Treasury yields, adding to the Greenback’s weekly gains.

USD/JPY kicked off early, with no intervention from Japanese officials and concerns over Japan’s coalition government possibly losing its majority in Sunday’s election pushing the yen (and other yen pairs) higher.

Later, a handful of European Central Bank (ECB) officials reiterated that inflation is on track, backing a more cautious pace of policy easing. The Bank of Canada (BOC) also cut rates by 50 bps, celebrating progress against high inflation and suggesting future moves would aim to “stick the landing” on inflation.

Bank of England (BOE) Governor Bailey and Reserve Bank of New Zealand (RBNZ) Governor Orr echoed similar sentiments, supporting further easing as inflation inches closer to their respective targets.

The U.S. dollar extended gains against “risk” currencies like AUD, NZD, and GBP during the early U.S. session but started to lose steam against other currencies. The Greenback saw more broad-based weakness after the Fed’s Beige Book report hinted at the need for looser monetary policies.

Upcoming Potential Catalysts on the Economic Calendar:

- France flash manufacturing and services PMIs at 7:15 am GMT

- Germany flash manufacturing and services PMIs at 7:30 am GMT

- Eurozone flash manufacturing and services PMIs at 8:00 am GMT

- U.K. flash manufacturing and services PMIs at 8:30 am GMT

- U.K. CBI industrial order expectations at 10:00 am GMT

- U.S. initial jobless claims at 12:30 pm GMT

- FOMC member Hammack to give a speech at 12:45 pm GMT

- BOE member Mann to give a speech at 1:00 pm GMT

- U.S. flash manufacturing and services PMIs at 1:45 pm GMT

- U.S. new home sales at 2:00 pm GMT

- BOE Gov. Bailey to give a speech at 7:45 pm GMT

- U.K. GfK consumer confidence at 11:01 pm GMT

- Japan Tokyo core CPI at 11:30 pm GMT

The markets will keep an eye on flash PMIs from France, Germany, the Eurozone, and the U.K., which will offer key insights into the health of the region’s manufacturing and services sectors.

In the U.S., initial jobless claims and flash PMIs will guide expectations on economic resilience, while speeches from central bankers like FOMC member Hammack and BOE Governor Bailey could inspire repricings of central bank expectations later in the day.

Don’t forget to check out our brand new Forex Correlation Calculator!