The market spotlight was on global flash PMI reports, which printed mixed results across major economies.

How did asset classes and currencies fare?

Check out the latest headlines that influenced price action:

Headlines:

- Australia Judo Bank flash manufacturing PMI dipped from 46.7 to 46.6 in Oct, flash services PMI up from 50.5 to 50.6

- Japan’s au Jibun flash manufacturing PMI fell from 49.7 to 49.0 in October (49.9 forecast)

-

Japanese monetary authorities attempt to jawbone currency:

- Finance Chief Kato says rapid moves are seen in the FX market, gives warning on yen’s slide

- Deputy Chief Cabinet Secretary Kazuhiko Aoki said govt watching forex moves closely including for speculative moves

-

Eurozone October PMI readings came in mixed:

- French HCOB flash manufacturing PMI dipped to 44.5 instead of climbing to 44.9 (previous reading upgraded from 44.0 to 44.6)

- French HCOB services PMI came in at 48.3 instead of the 49.8 consensus (previous reading revised from 48.3 to 49.6)

- German HCOB flash manufacturing PMI jumped from 40.6 to 42.6, outpacing the 40.7 estimate, and the flash services PMI rose from 50.6 to 51.4 (50.6 consensus)

- Eurozone HCOB flash manufacturing PMI up from 45.0 to 49.9 (45.1 consensus); flash services PMI down from an upgraded 51.4 figure to 51.2 (51.5 consensus)

- U.K. Oct flash manufacturing PMI down from 51.5 to 50.3 (51.5 consensus); flash services PMI fell from downgraded 52.4 to 51.8 (52.3 forecast)

- U.K. CBI industrial order expectations index up from -35 to -27 (-28 consensus) but output volumes still lower

- U.S. Secretary of State Blinken mentioned that some progress was being made in Israel-Hamas ceasefire negotiations

- U.S. weekly initial jobless claims at 224K in the week ending Oct. 17 (243K expected, 242K previous)

- U.S. Oct flash manufacturing PMI improved from 47.3 to 47.8 (47.5 forecast); flash services PMI up from 55.2 to 55.3 (55.0 forecast)

- U.S. new home sales rose from downgraded 709K to 738K (719K consensus) in Sept

- U.K. GfK consumer confidence index slipped from -20 to -21 in Oct (-20 forecast) as possible tax hikes weigh on sentiment

Broad Market Price Action:

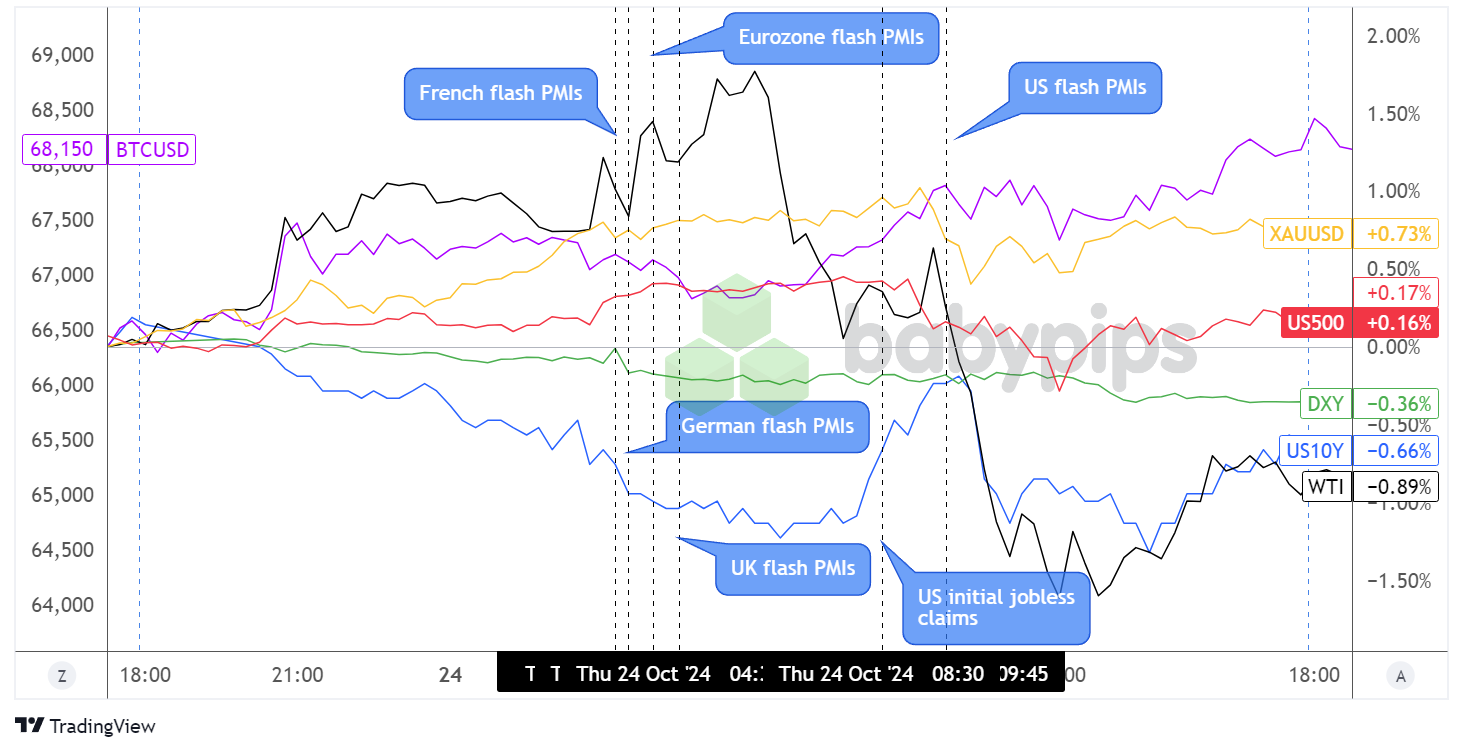

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

A bit of risk-taking was seen in the markets in the past trading sessions, as commodities and bitcoin kicked higher right around the start of the Asian session while the U.S. dollar and Treasury yields cruised south for the most part of the day.

Additional volatility came in for crude oil right around the release of the eurozone flash PMI figures, as mixed results were seen from the region’s top economies, but the commodity eventually peaked around $72.25 per barrel then took a nasty tumble during London market hours.

As it turned out, U.S. Secretary of State Blinken suggested that some progress was being made in ceasefire talks between Israel and Hamas, further easing global oil supply concerns.

A bit of a bounce was seen around the release of better than expected U.S. initial jobless claims data, although risk assets tumbled when the U.S. flash PMI figures were printed. Stronger than expected earnings figures from Tesla pulled U.S. stock indices higher towards the close, allowing the Nasdaq to catch a 0.8% gain and the S&P 500 to cap off its three-day losing streak.

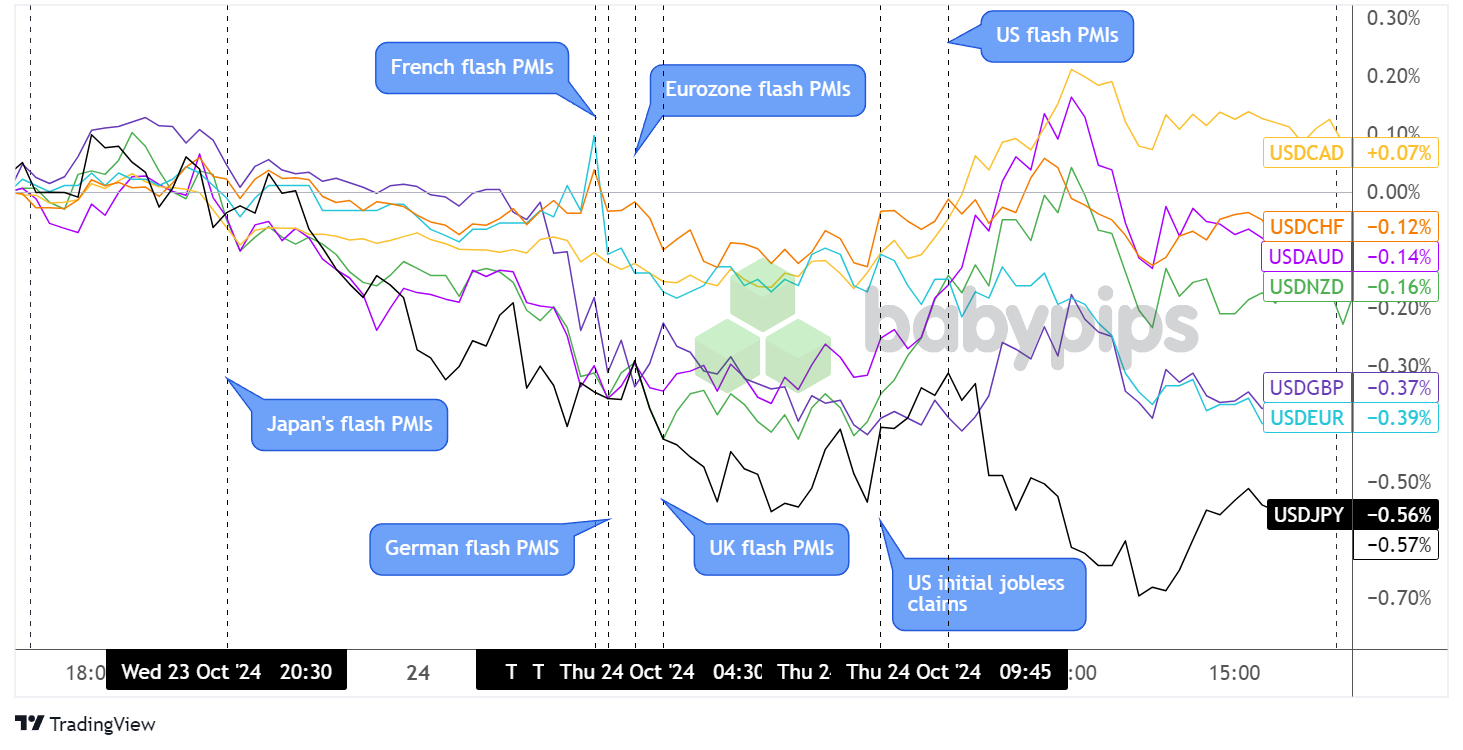

FX Market Behavior: U.S. Dollar vs. Majors:

Overlay of USD vs. Major Currencies Chart by TradingView

After raking in a few gains versus the yen, Kiwi, and Aussie, the U.S. dollar slid lower throughout the Asian trading session, as investors appeared to be in a better mood for risk-taking. The yen took another hit during the release of weaker than expected Japanese flash manufacturing PMI, but the currency went on to advance against the dollar for the rest of the session.

EUR/USD dipped to negative territory when French flash manufacturing and services PMIs fell short of estimates, but the shared currency quickly regained ground after Germany’s results turned out better than expected. The U.K. economy also reported weaker than expected PMI readings, but sterling fought to hold its ground against the dollar during London market hours.

Lower than expected U.S. weekly initial jobless claims allowed the dollar to recover across the board later on, extending its rally versus the commodity currencies, pound and Swiss franc after the U.S. flash manufacturing and services PMIs came in broadly in line with estimates. Price action diverged among the rest of the majors, however, with the yen and euro going for more gains.

Upcoming Potential Catalysts on the Economic Calendar:

- Chinese foreign direct investment data lined up

- German Ifo business climate index at 8:00 am GMT

- Canada’s headline and core retail sales at 12:30 pm GMT

- U.S. headline and core durable goods orders at 12:30 pm GMT

- BOE monetary policy report hearings coming up

- U.S. revised UoM consumer sentiment index at 2:00 pm GMT

Price action could calm down after yesterday’s PMI chaos, as the economic calendar only has a few notable catalysts on deck. This includes Canada’s consumer spending data, as well as the BOE Monetary Policy Report hearings, that could bring additional volatility for CAD and GBP pairs.

As always, keep an eye out for headlines that impact overall market sentiment, and don’t forget to check out our brand new Forex Correlation Calculator!