The Reserve Bank of Australia (RBA) kept its cash rate target unchanged at 4.35% today, maintaining its hawkish stance on inflation while acknowledging economic uncertainties. This decision was widely expected by market participants, as covered and anticipated in the Babypips.com Event Guide.

Key points from the RBA statement:

- Inflation remains above target and is proving persistent

- Current forecasts do not see inflation returning sustainably to target until 2026

- GDP data for June quarter confirmed weak growth

- Labour market conditions remain tight despite some signs of gradual easing

- The Board remains resolute in its determination to return inflation to target

Link to the September RBA Statement

In its statement, the RBA emphasized that “inflation remains above target and is proving persistent.” The Board noted that while inflation has fallen substantially since its peak in 2022, it is still “some way above the midpoint of the 2–3 per cent target range.” The trimmed mean measure of underlying inflation was 3.9% over the year to the June quarter.

The central bank highlighted ongoing economic uncertainties, including the lag in monetary policy effects, firms’ pricing decisions, wage responses, and geopolitical factors. Despite these concerns, the RBA maintained that its current policy stance is “restrictive and working broadly as anticipated.”

During the following press conference, RBA Governor Michele Bullock stressed the Board’s commitment to curbing inflation: “Sustainably returning inflation to target within a reasonable timeframe remains the Board’s highest priority. This is consistent with the RBA’s mandate for price stability and full employment.”

She also noted that the economic outlook is uncertain, as well as achieving the goal of disinflation without causing a recession, so for now, the RBA is prepared to adjust policy in either direction if needed.

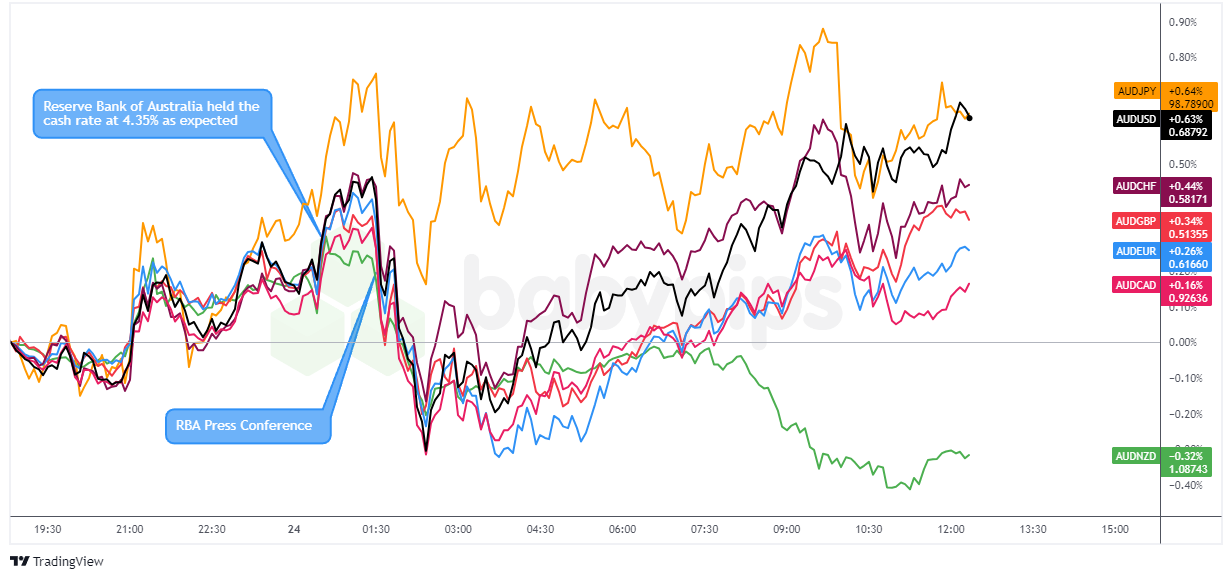

Market Reactions

Overlay of AUD vs. Major Currencies Chart by TradingView

The initial reaction to the RBA’s decision saw the Australian dollar strengthen across the board. This “buy the fact” response likely reflected the market’s interpretation that the RBA’s persistent focus on inflation and its reluctance to signal any near-term easing was slightly more hawkish than anticipated.

Selling pressure did emerge during the press conference, possibly a combination of some profit-taking, net negative comments from the RBA Governor on productivity concerns and subdued GDP growth, and/or possibly reactions to comments that interest rate hikes were not considered at this month’s meeting.

Whatever the case may be for the dip, buyers quickly stepped in at the London session open. This was arguably due to fundamental buyers who still see an outlook where the odds of rate cuts ahead remain low for now, and the interest rate differential outlook still looks relatively favorable for the Aussie.

Additionally, fresh news of stimulative action from the People’s Bank of China was supportive of broad risk-on sentiment for the session, which may have been a contributor to the Australian dollar’s bid as well.