Consumer prices in the U.S. took an unexpected dip in June, dropping by 0.1% month-over-month. This marks the first decline since May 2020 and contrasts with the expected 0.1% increase. It’s also a shift from May’s flat reading.

When we strip out the volatile stuff like food and energy, the core CPI also came in lower at 0.1%, missing the market’s forecast of holding steady at May’s 0.2% rise.

This cooling off in prices helped bring annual inflation down a notch. The headline CPI eased from 3.3% to 3.0%, the lowest it’s been since June 2023. Similarly, the core CPI slowed from 3.4% to 3.3%, marking the slowest increase since April 2021.

Link to U.S. Consumer Price Index for May 2024

The report detailed that energy costs fell by another 2.0% m/m, with sub-indices like energy commodities, gasoline, and fuel oil falling faster compared to the previous month.

Shelter costs also eased, up by only 0.2% after clocking in a 0.4% monthly gain since February.

Last but not least, auto prices declined with new vehicle prices dipping by 0.2% after May’s 0.5% decrease while used cars and trucks dropped by 1.5% after a 0.6% gain in May.

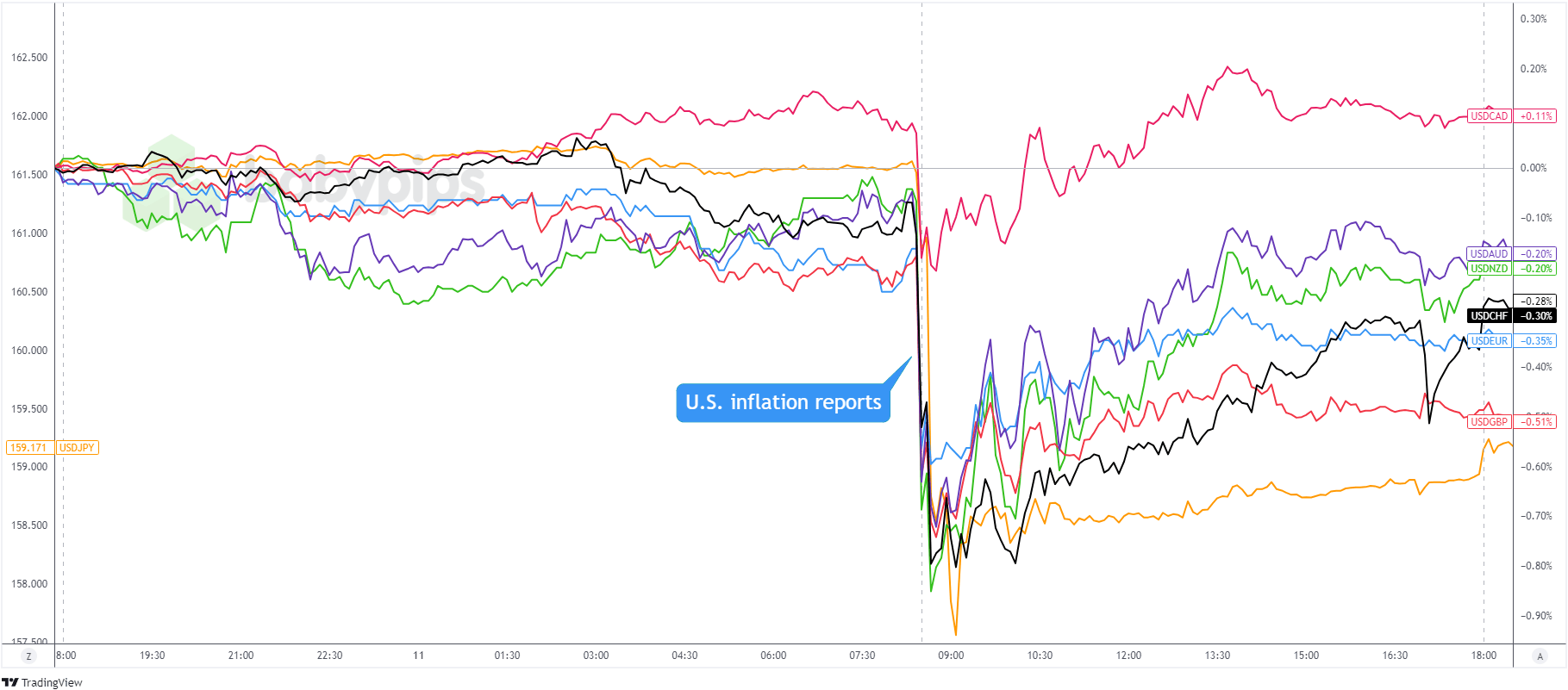

Market Reaction

U.S. Dollar vs. Major Currencies: 5-min

Overlay of USD vs. Major Currencies Chart by TradingView

The odds of a Fed rate cut by September was already at 70% after Powell talked about cooler labor market pressures earlier this week.

Those odds rose to 84.6% after the U.S. inflation report came out. Not only that, but traders are now pricing in multiple rate cuts in 2024. The CME FedWatch Tool puts the odds of a second rate cut in November at 50.3% and a third one in December at 43.9%

The U.S. dollar, which was trading in ranges since the start of the European session, dropped sharply at the broadly weak CPI reports.

The post-report spike lower marked the Greenback’s intraday lows, however. USD buyers soon stepped in and caused pullbacks across the board.. One possible reason is that a weakness in U.S. equities may have inspired risk aversion and improved USD demand. Talks of Japanese officials intervening also made rounds and encouraged USD-buying.

The dollar capped the day much higher than its post-CPI lows but still in the red against most of its major counterparts. It saw the heaviest losses against JPY, GBP, and EUR but still ended the day positive against the Canadian dollar.