When the markets are hotly debating the Fed’s next policy moves, U.S. labor market updates – which Fed members said they’re looking closely at – will likely cause increased volatility among major U.S. dollar pairs.

On Thursday, a report from Challenger, Gray, & Christmas reflected 72,821 planned job cuts in September, slightly lower than the 75,891 cuts planned in August.

The report noted that “it will take a few months for the drop in interest rates to impact employer costs,” but that it will also increase consumer spending which may lead to more demand for workers in consumer-facing sectors.

This may explain why out of 403,891 hiring plans in September, 401,850 of them were from seasonal employers in the Retail and Transportation/Warehousing sectors.

Link to the September The Challenger Report

Later, the Labor Department’s weekly initial jobless claims printed at 225K in the week ending September 28, a smidge higher than the 222K estimates and the upwardly revised 219K figure from the previous week.

The report added that the four-week moving average was revised 250 higher from 224,750 to 225,000.

Link to Department of Labor’s weekly initial jobless claims report

Meanwhile, S&P Global’s final services PMI also showed a downward revision from 55.4 to 55.2 for the month.

The details revealed that the Employment component fell ‘only marginally,’ though it still marked its second consecutive monthly decline. Respondents reported lowering staffing levels and staff shortages as reasons for weaker job prospects.

Link to S&P Global’s September final services PMI

Last but not least, ISM’s services PMI jumped from 51.5 to 54.9 in September. Not only did it mark its seventh consecutive month of expansion, but it also logged its highest reading since February 2023.

However, the report’s Employment Index contracted for the first time in three months, down 2.1 points from 50.2 to 48.1.

Link to ISM’s September services PMI

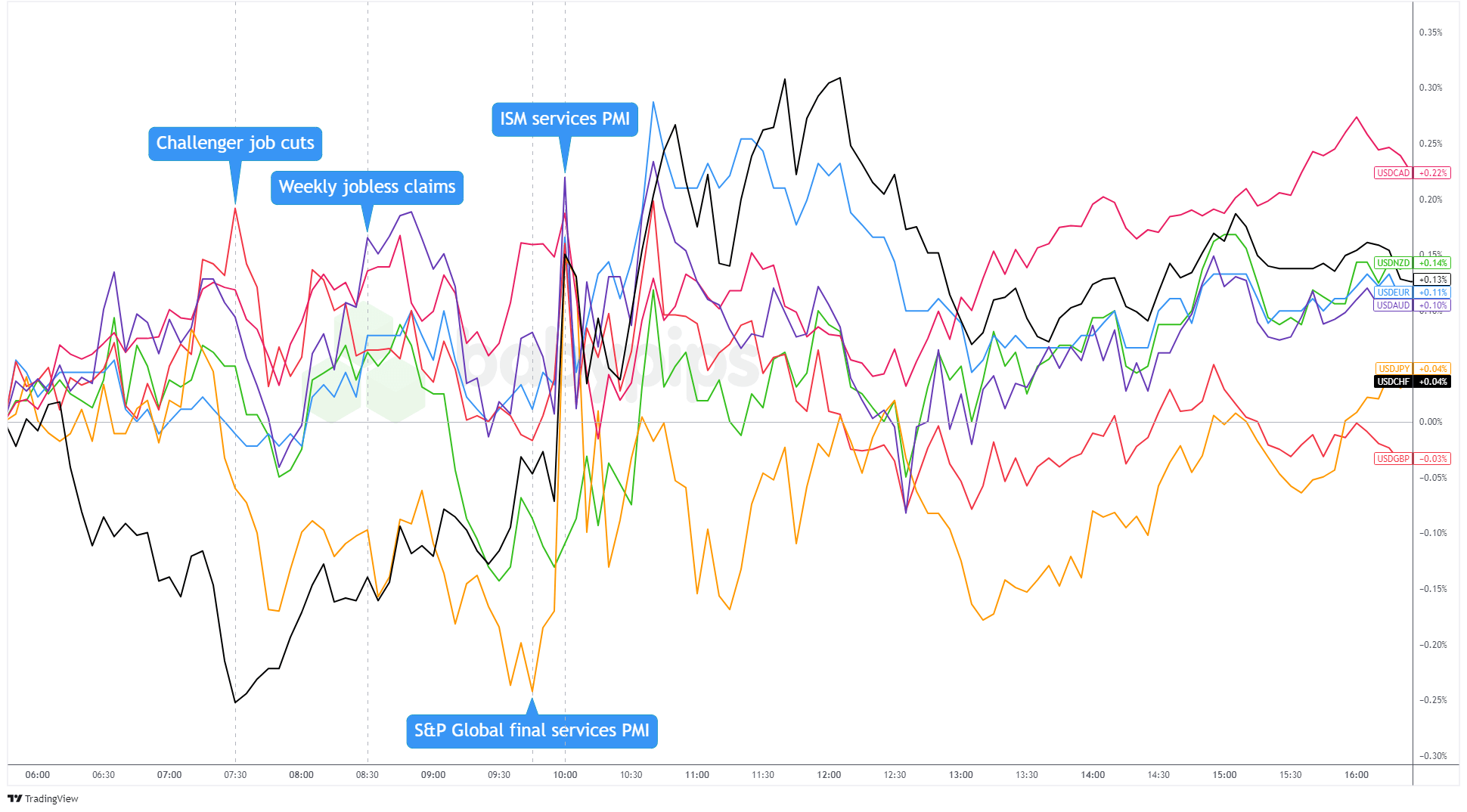

U.S. dollar vs. Major Currencies: 5-min

Overlay of USD vs. Major Currencies Chart by TradingView

Aside from the Swiss franc, the U.S. dollar held onto modest gains against other major currencies, driven by concerns over the Middle East conflict and ahead of key U.S. labor market data.

The Challenger report initially triggered some dips, but the greenback bounced back before the weekly jobless claims came out. However, the dollar slipped again until we saw the S&P Global final services PMI and ISM PMIs.

There was extra volatility around the ISM PMI release, likely because the headline PMI hit multi-month highs, while the Employment Index showed contraction. To add to the uncertainty, President Biden suggested Israel might target Iran’s oil infrastructure, which could have rattled some risk-takers.

The dollar rode the wave of positive ISM PMI data and geopolitical concerns, but it looks like profit-taking may have set in ahead of Friday’s NFP report.