The latest U.K. economic activity update reveals a stagnant picture for July 2024, with flat GDP growth and mixed performance across sectors, likely leaving the Bank of England (BoE) in a delicate position as it considers future monetary policy decisions.

Key Points:

- U.K. GDP showed no growth (0.0%) in July 2024, following flat growth in June 2024.

- The services sector grew by 0.1% in July 2024, while production fell by 0.8% and construction decreased by 0.4%.

- In the three months to July 2024, the economy grew by 0.5% compared with the three months to April 2024.

- Information and communication was the largest positive contributor to services growth, increasing by 0.8% in July 2024.

- Manufacturing output decreased by 1.0%, being the largest negative contributor to production.

- Consumer-facing services increased by 0.3% in July 2024, following a decrease of 0.7% in June 2024.

Link to the July 2024 ONS GDP Monthly Estimate

The U.K. economy showed no growth in July 2024, with a slight expansion in the services sector offset by declines in production and construction.

While this does somewhat support the idea of future rate cuts ahead from the Bank of England, it arguably doesn’t look to be enough for the BOE to cut at the upcoming policy meeting and statement on September 19.

Market Reactions

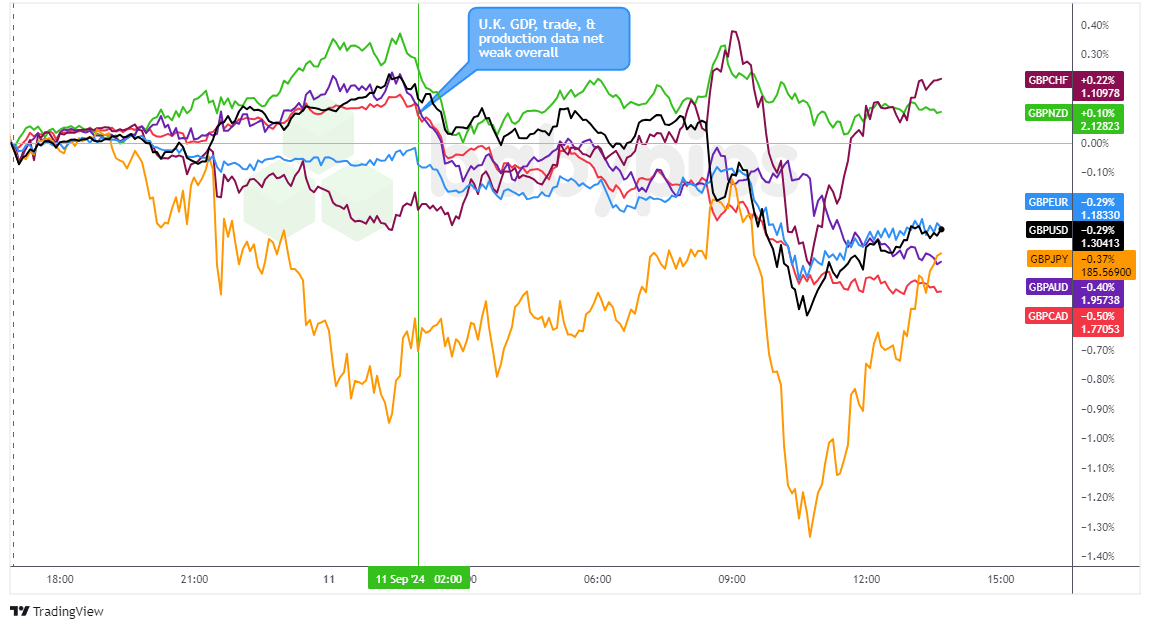

British Pound vs. Major Currencies: 5-min

Overlay of GBP vs. Major Currencies Chart by TradingView

The initial market response for Sterling was a net negative one, with GBP falling against the majors, with exception to the Swiss franc and Japanese yen.

This suggests that while the U.K. economic update (and its support for BOE rate cuts ahead) was the main driver, broad risk-on sentiment was arguably just as big of a weight to GBP given the strength against the “safe havens.”

Sterling did take a bigger dive during the following U.S. trading session, with no fresh catalysts to directly point to. This may have been a delayed reaction to the U.K. data updates from U.S. traders, but it’s more likely that the bearish turn in broad risk sentiment was the bigger driver as U.S. equities, crypto and oil dumped right at the U.S. equity session open.

This sudden broad market turn was likely a reaction to a ever-so-slightly higher-than-expected U.S. Core CPI update an hour before the open. This was arguably was another signal that inflation isn’t ready to go away, which is likely to keep the Fed from getting too carried away on rate cuts ahead.