The September U.S. CPI report reflected slowing price pressures for the month, but the annual headline and core inflation readings were still hotter than expected.

Headline CPI rose another 0.2% month-on-month, slightly higher than the projected 0.1% uptick, while the core CPI logged in a 0.3% monthly gain versus the expected 0.2% increase. This brought the annual headline CPI down from 2.5% to 2.4%, a notch higher than the 2.3% consensus and still above the central bank’s 2% target.

Link to official U.S. CPI Report (September 2024)

Underlying components revealed that the gains were spurred by a 0.2% monthly increase in shelter costs and a 0.4% rise in food prices while the energy index fell 1.9% for the month.

The CME FedWatch tool showed an 84.4% chance of a 0.25% rate cut in the next Fed meeting, up from the previous day’s 80.3% likelihood, as traders see lower odds of another 0.50% reduction in borrowing costs.

Market Reactions

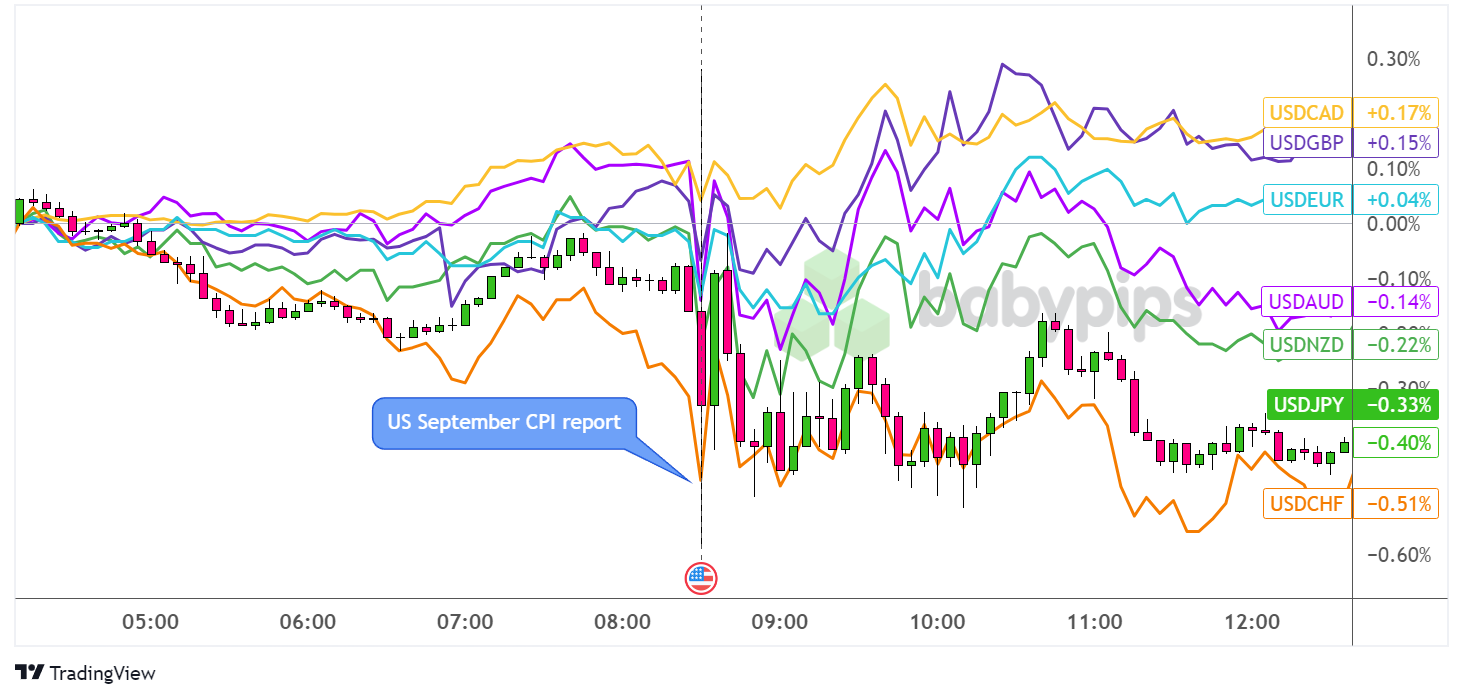

U.S. dollar vs. Major Currencies: 5-min

Overlay of USD vs. Major Currencies Chart by TradingView

The U.S. dollar, which started picking up on additional volatility in the hours leading up to the U.S. CPI release, tossed this way and that after seeing the actual numbers.

Although the results came in the green, the U.S. currency continued to edge lower versus the yen and franc while also dipping briefly against the rest of its counterparts, except against the Canadian dollar.

From there, the dollar pulled higher versus its higher-yielding peers roughly an hour after the CPI figures were printed then proceeded to slump once again towards the end of the trading session.