Because you asked for it, I ran a quick backtest of the Short-Term Bollinger Reversion strategy on USD/CAD from August to December last year. Here are the results.

But if this is the first time you’re reading about this mechanical forex trading system, I suggest you review the rules right here.

As mentioned, I’m trying this mean reversion strategy out for USD/CAD since this pair has a tendency to move sideways. I’m also open to trying it out on other Loonie crosses like CAD/CHF or NZD/CAD later on.

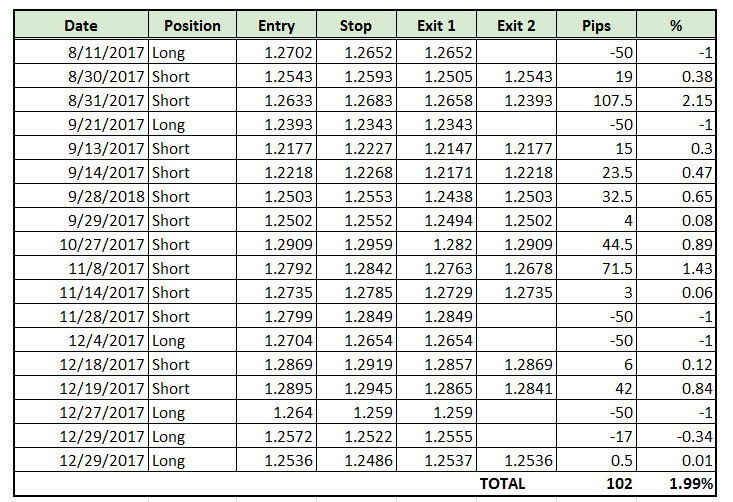

I’ve stored only the historical price data as far back August 2017 in my random-access memory chip and left the earlier figures up in the galaxy (I believe humans call it the “cloud” these days?) to save on storage, but I think there are enough insights to be gleaned from these results: Not bad for a five-month run, eh? The strategy was able to catch 102 pips or nearly 2% in gains (assuming 1% risk per position) for the time period.

Not bad for a five-month run, eh? The strategy was able to catch 102 pips or nearly 2% in gains (assuming 1% risk per position) for the time period.

It was able to catch a total of 18 signals then, with 12 ending in gains for a win rate of 66.67%. However, its average win was less than the average loss as a number of those gains were measly single-digit pips.

Then again, it’s worth noting that the maximum winning streak of 7 trades had a 3.88% gain versus the max drawdown of 2% from a couple of consecutive losing positions.

From what I observed, there’s plenty of room for improvement in terms of keeping the system out of trending markets. Even though it was able to catch pips off those short-term bounces in between trends, the system had a nasty run when the pair began sliding sharply in the last week of December.Got any suggestions to help this robot out?