This week our currency strategists focused on inflation and flash business survey data, specifically from Canada and the Euro area for potential high quality setups.

Out of the four scenario/price outlook discussions this week, only one discussion arguably saw both fundie & technical arguments triggered to become a potential candidate for a trade & risk management overlay. Check out our review on those discussions to see what happened!

Watchlists are price outlook & strategy discussions supported by both fundamental & technical analysis, a crucial step towards creating a high quality discretionary trade idea before working on a risk & trade management plan.

If you’d like to follow our “Watchlist” picks right when they are published throughout the week, you can subscribe to BabyPips Premium.

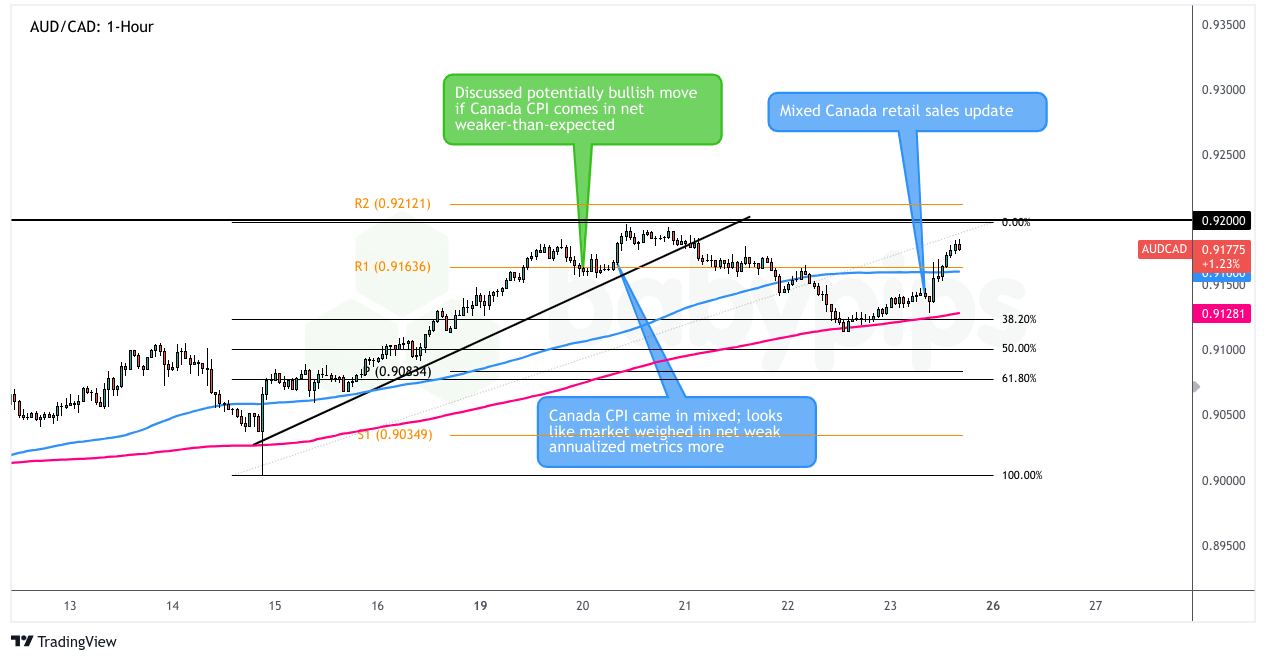

AUD/CAD: Tuesday – August 20, 2024

AUD/CAD 1-Hour Forex Chart by TradingView

On Tuesday, our strategists eyed the upcoming Canadian CPI report and its potential implications for the Canadian dollar. Based on our Event Guide for the CPI report, the markets were expecting numbers roughly inline to weak than previous reads. With those expectations and looking at the potential effects of upcoming events related to the Federal reserve, here’s what we were thinking:

The “Loonie Dive” Scenario: If the CPI came in as expected or lower, we figured the BOC might start eyeing those rate cut scissors. This could draw in fundamental CAD sellers, and with the RBA likely to keep interest rates elevated in Australia, we eyed AUD/CAD for potential long strategies to watch.

The “Loonie Bounce” Scenario: If Canada’s inflation growth decided to play tough and come in hotter than expected, we thought the BOC might keep those rate hike dreams alive. This could’ve been CAD buyers’ time to shine, prompting a look at CAD/CHF given the interest rate difference and if the market broke a major support area.

What Actually Happened

Well, folks, Wednesday rolled around, and Canada’s CPI decided to throw us a mixed set of numbers to cloudy up potential strategies and actions ahead.

The headline CPI showed a 0.4% month-on-month rebound as expected, but the annual reading slipped from a 2.7% year-over-year increase in June to just 2.5% in July – its lowest reading since March 2021. The core CPI reflected a 0.3% monthly uptick, but annual core inflation dipped from 1.9% to 1.7% instead of holding steady.

The market reacted with broad CAD weakness, an outcome that triggered our arguments for an AUD/CAD bullish bias, as the cooler-than-expected annualized inflation data increased the likelihood of a dovish BOC stance.

Market Reaction

The initial market reaction was swift, with the Loonie taking a tumble across the board. Looking at our AUD/CAD chart, we can see that the pair indeed saw an immediate bounce following the CPI release, climbing from around the 0.9100 level towards the R1 pivot point at 0.9163.

However, the pair’s upward momentum was somewhat tempered by broader market dynamics. The risk-on sentiment that prevailed early in the week, which had initially supported the Aussie, began to wane. Additionally, progress in Israel-Hamas ceasefire negotiations dampened crude oil supply concerns, further pressuring the oil-linked Loonie.

Interestingly, the chart shows that after the initial spike, AUD/CAD pulled back, possibly on some repositioning ahead of the highly anticipated Jackson Hole event, and possibly on the recovery in oil prices in the latter half of the week.

But by Thursday, risk-on vibes were back in play, arguably giving more lift to the Aussie than the Loonie as rate cut expectations rose and bond yields fell.

By the end of the week, AUD/CAD was hovering around the 0.9180 level, having broken above our R1 (0.9163) pivot point but still shy of the R2 (0.9212) level we had identified.

The Verdict

So, how’d we do? In our original discussion, we mentioned a potential pullback in the works and to “look out for any reversal candlesticks,” primarily around the rising moving averages. If that strategy was followed, it’s highly likely that lead to a net positive outcome.

But AUD/CAD shot higher after the weak annualized CPI numbers and the anticipated pullback came after the target event, so some discretion was needed on whether or not to move in on the spike higher or to stay patient for the pullback we discussed originally.

Overall, we’d rate this discussion as “neutral-to-likely” in supporting a potential positive outcome because while the strategy and outcome worked out well, individual trade execution planning and decisions would have been a strong factor in the outcome.

EUR/GBP: Wednesday – August 21, 2024

EUR/GBP 1-Hour Forex Chart by TradingView

On Wednesday, our strategists had their sights set on the upcoming Euro area PMI releases and their potential impact on the euro. Based on our Event Guide for the Euro area PMIs, the markets were expecting continued divergences between weak manufacturing signals and strong service sector updates.

With those expectations and looking at the potential effects of the recently released FOMC meeting minutes and the global PMI signals, here’s what our strategists were looking at:

The “Euro Stumble” Scenario:

If the Eurozone PMIs showed net weakness, especially in manufacturing, we anticipated EUR/GBP might extend its August downtrend. This scenario aligned with the pair’s inability to make new weekly highs above technical resistance.

The “Euro Bounce” Scenario:

If the Eurozone data surprised net to the upside, particularly in services, we thought EUR/CAD might find some bullish momentum after the weak annualized CPI read from Canada, and an upside triangle break that could draw in technical bulls.

What Actually Happened

Thursday rolled around, and the Euro area PMIs decided to serve up a mixed platter that would make even the most seasoned forex chef scratch their head.

- HCOB Flash Eurozone manufacturing PMI dipped from 45.8 to an eight-month low of 45.6 in August.

- Eurozone Services PMI shot up from 51.9 to a four-month high of 53.3.

- France saw its manufacturing PMI fall to an eight-month low of 42.1, while services jumped to a 27-month high of 55.0.

- Germany’s manufacturing PMI dipped to a five-month low of 42.1, with services expanding at a softer pace.

Meanwhile, across the Channel:

- U.K.’s private sector showed solid expansion in August.

- Manufacturing PMI rose from 52.1 to 52.5 (26-month high).

- Services PMI improved from 52.5 to 53.3 (four-month high).

- Composite PMI jumped from 52.8 to 53.4 (highest since April).

Market Reaction

This outcome triggered our fundamental arguments for an EUR/GBP bearish bias. The pair took a decisive dive following the PMI releases, breaking through multiple support levels faster than you can say “economic divergence.”

Looking at the 1-hour chart, EUR/GBP sliced through the pivot point (0.85380) like a hot knife through butter, barely pausing for breath as it crashed past S1 (0.84831) to the S2 (0.84550) support area.

The stark contrast between the weakening Eurozone manufacturing sector and the robust U.K. PMIs across the board gave GBP bulls all the ammunition they needed. Add to this the comments from ECB official Olli Rehn about slowing inflation and economic weakness in the euro-zone, and you’ve got a recipe for euro weakness that even the improved services PMI couldn’t offset.

The Verdict

So, how’d our strategy discussion do? Well, it was sharper than a trader’s pencil on NFP day. We’re rating this discussion as “highly likely” in supporting a potentially positive outcome.

The resulting move was clearly inline with our fundamental analysis for the bearish lean on EUR/GBP, correctly anticipating the impact of diverging economic performances between the Eurozone and the U.K.

The technical setup also played out beautifully, with the pair respecting the resistance levels we identified in our original discussion before plummeting on the news.

For those who leaned bearish when both fundamental and technical arguments were triggered on Thursday, they likely saw a substantial positive outcome. The strong momentum move offered multiple opportunities to capitalize, whether traders aimed for the S1 or S2 pivot support areas.