This week our currency strategists focused on inflation and GDP data, specifically from Australia and the U.S. for potential high quality setups.

Out of the four scenario/price outlook discussions this week, two discussions arguably saw both fundie & technical arguments triggered to become potential candidates for a trade & risk management overlay. Check out our review on those discussions to see what happened!

Watchlists are price outlook & strategy discussions supported by both fundamental & technical analysis, a crucial step towards creating a high quality discretionary trade idea before working on a risk & trade management plan.

If you’d like to follow our “Watchlist” picks right when they are published throughout the week, you can subscribe to BabyPips Premium.

GBP/AUD: Tuesday – August 27, 2024

GBP/AUD 1-Hour Forex Chart by TradingView

On Tuesday, our strategists had their sights set on the Australian CPI update for July 2024 and its potential impact on the Australian dollar. Based on our Event Guide, expectations ranged from a dip to 3.6% to 3.4% year-on-year, down from the earlier 3.8% annual CPI reading. While this would be favorable for the Reserve Bank of Australia’s goals, even at 3.4% y/y, the rate of price growth is still uncomfortably high.

With those expectations in mind, here’s what we were thinking:

The “Aussie Avalanche” Scenario:

If the CPI came in as expected or lower, we figured the RBA might start eyeing those rate cut scissors. This could draw in fundamental AUD sellers, drawing us to AUD/CAD which recently saw an uptrend broken. This scenario may draw in technical sellers along with fundie players in this scenario.

The “Kangaroo Bounce” Scenario:

If Australia’s inflation growth came in hotter than expected, we thought the RBA might keep their neutral-to-hawkish stance. This could be AUD buyers’ time to shine, prompting a look at GBP/AUD for potential short strategies as the pair retested (and was finding resistance) at the top of its recent ranging behavior.

What Actually Happened

Well, folks, Wednesday rolled around, and Australia’s CPI update decided to give us mixed signals. The data from the Australian Bureau of Statistics (ABS) showed that inflation in Australia rose by 3.5% y/y in July, slower than June’s 3.8% increase and the lowest since March, but higher than the 3.4% uptick that markets had expected.

Key points from the CPI report:

- Excluding volatile items, CPI slowed down from 4.0% to 3.7% from a year ago in July.

- RBA’s trimmed mean inflation came in at 3.8%, lower than the 4.1% annual increase in June and marked the lowest since early 2022.

- Housing (+4.0%), Food and non-alcoholic beverages (+3.8%), Alcohol and tobacco (+7.2%), and Transport (+3.4%) saw the biggest gains for the month.

Market Reaction

The cooler-than-expected – but still elevated – July inflation update initially boosted the Aussie. This triggered our arguments for a GBP/AUD short bias, and we can see that the pair saw an immediate drop following the CPI release, falling from around the 1.9500 level towards the pivot point (P) at 1.9413.

The pair’s downward momentum was somewhat supported by broader market dynamics. The risk-off sentiment that prevailed mid-week, which had initially supported the pound, began to wane and likely bring more interest in the Aussie over Sterling. But, we saw weak capex data from Australia on Thursday and stagnant retail sales data on Friday, which were likely putting the caps on the Aussies bull run.

By the end of the week, GBP/AUD was hovering around the 1.9400 level, having found supported just above the S1 (1.9290) pivot support area before hitting a wall of bears around the pivot point (P) at 1.9413 we had identified.

The Verdict

So, how’d we do? In our original discussion, we mentioned potential short setups on GBP/AUD if the AU CPI came in net positive, which it did. If that strategy was followed, it’s “likely” that it was supportive of a net positive outcome, given that the market saw strong bearish momentum and closed below both discussion and event price areas at the Friday close.

For those who leaned bearish on GBP/AUD when both fundamental and technical arguments were triggered on Wednesday, they likely saw the best potential return on risk, and those who waited for the trendline break also likely set net gains, even if they didn’t manage the positive for a profit when it started to bottom out below the 1.9350 handle.

USD/JPY: Wednesday – August 28, 2024

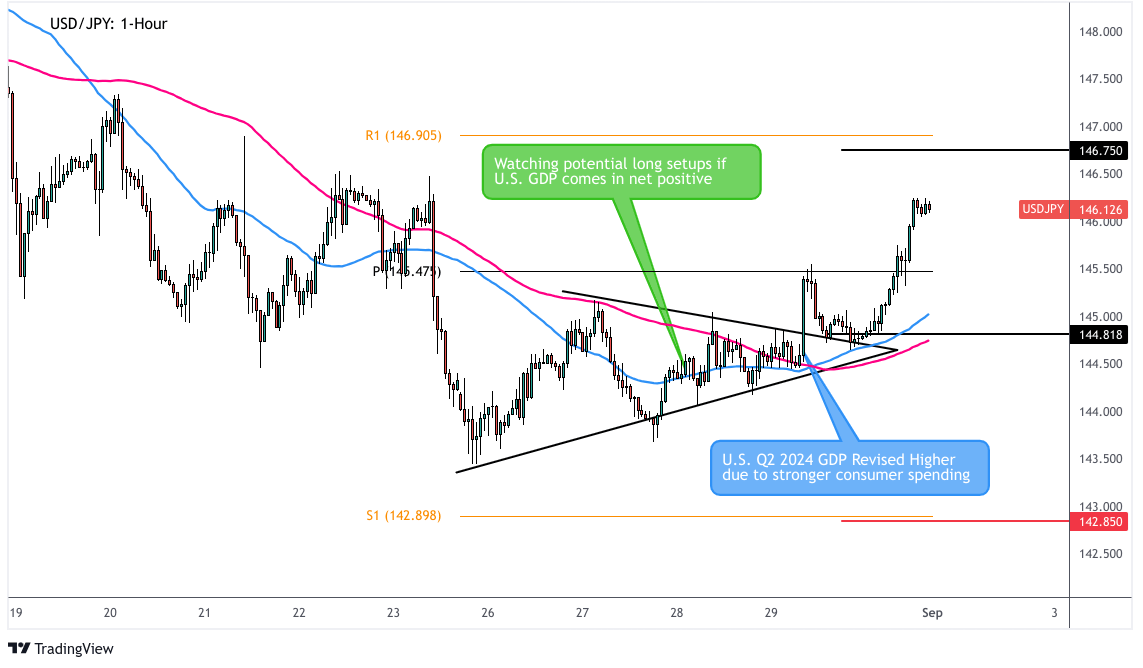

USD/JPY 1-Hour Forex Chart by TradingView

On Wednesday, our strategists had their sights set on the U.S. Preliminary GDP release for Q2 2024 and its potential impact on the U.S. dollar. Based on our Event Guide for Q2 2024 U.S. GDP, the markets were expecting little to negative revisions from the advanced 2.8% q/q reading. Based on that, we had two main scenarios in mind:

The “Dollar Dive” Scenario:

If the GDP came in as expected or lower, we figured the Fed might lean more towards a September rate cut, potentially a larger 50 basis point move. This could draw in fundamental USD sellers, and we had our eyes on AUD/USD for this particular scenario, given the pair’s upward momentum and recent strong Australian CPI data.

The “Greenback Gain” Scenario:

If the U.S. GDP surprised to the upside, we thought this could ease U.S. recession concerns and boost the dollar. We were watching USD/JPY for this scenario, as the pair’s recent behavior had been showing signs of a potential reversal from its recent downtrend.

What Actually Happened

Well, Thursday rolled around, and the U.S. GDP decided to throw us a curveball that would make even Shohei Ohtani proud. The second version of the U.S. GDP reading was upgraded to show a faster 3.0% expansion in Q2 2024, surpassing both the initially reported 2.8% figure and market expectations.

The positive revision mostly came from higher consumer spending on services and goods, particularly gasoline and other energy commodities. However, components like non-residential fixed investment, exports, and private inventory investment were downgraded.

Adding to the dollar-positive sentiment, the preliminary price index for the same period was upgraded from 2.3% to 2.5%, exceeding expectations of an unchanged reading. The core PCE price index (excluding food and energy) saw a slight downgrade to 2.8% from the initial 2.9% estimate.

Market Reaction

The market reaction was swift and decisive, aligning perfectly with our “Greenback Gain” scenario. USD/JPY, which had been consolidating in a triangle pattern on the hourly chart, broke out to the upside following the GDP release.

Looking at our USD/JPY chart, we can see that the pair indeed saw an immediate bounce following the GDP release, climbing from around the 144.50 level and breaking through the 145.00 “neckline” we had identified in our original discussion. The pair continued its ascent, pushing past the 145.50 Pivot Point and reaching towards the R1 level at 146.91.

The stronger-than-expected GDP data, coupled with the upward revision in the price index, significantly reduced market expectations for aggressive Fed rate cuts. This shift in sentiment provided strong support for the dollar across the board, but particularly against the yen, which had been under pressure due to the Bank of Japan’s continued wide interest rate differential with the major central banks.

Interestingly, the USD/JPY rally extended well into Friday’s session, fueled by additional positive U.S. economic data. The release of the core PCE price index (the Fed’s preferred inflation gauge) showed persistent inflationary pressures, further dampening expectations of near-term rate cuts and providing additional momentum for the dollar.

The Verdict

So, how’d we do? In our original discussion, we mentioned watching for bullish candlesticks above the 145.00 “neckline”, 100 SMA, or the 145.50 Pivot Point area for clues of an upside breakout. If that strategy was followed, it’s “highly likely” that this discussion supported a net positive outcome.

For traders who executed based on this outlook, there were multiple opportunities to capitalize on the move:

- An initial entry could have been taken on the break above the 145.00 “neckline”, with a stop loss below the breakout point.

- Traders could have added to their positions or entered on a retest of the 145.50 Pivot Point.

- More conservative traders might have waited for the break above the recent swing high around 146.00 before entering, and still captured some pips before the weekend.

In all cases, the strong momentum provided ample opportunity to trail stops and capture a significant portion of the move.