Our strategists focused on Euro area business surveys and the Bank of Canada interest rate statement this week, this time prompting our strategists to focus on the euro and the Loonie.

Out of the four scenario/price outlook discussions this week, two discussions arguably saw both fundie & technical arguments triggered to become a potential candidates for a trade & risk management overlay. Check out our review on that discussion to see what happened!

Watchlists are price outlook & strategy discussions supported by both fundamental & technical analysis, a crucial step towards creating a high quality discretionary trade idea before working on a risk & trade management plan.

If you’d like to follow our “Watchlist” picks right when they are published throughout the week, you can subscribe to BabyPips Premium.

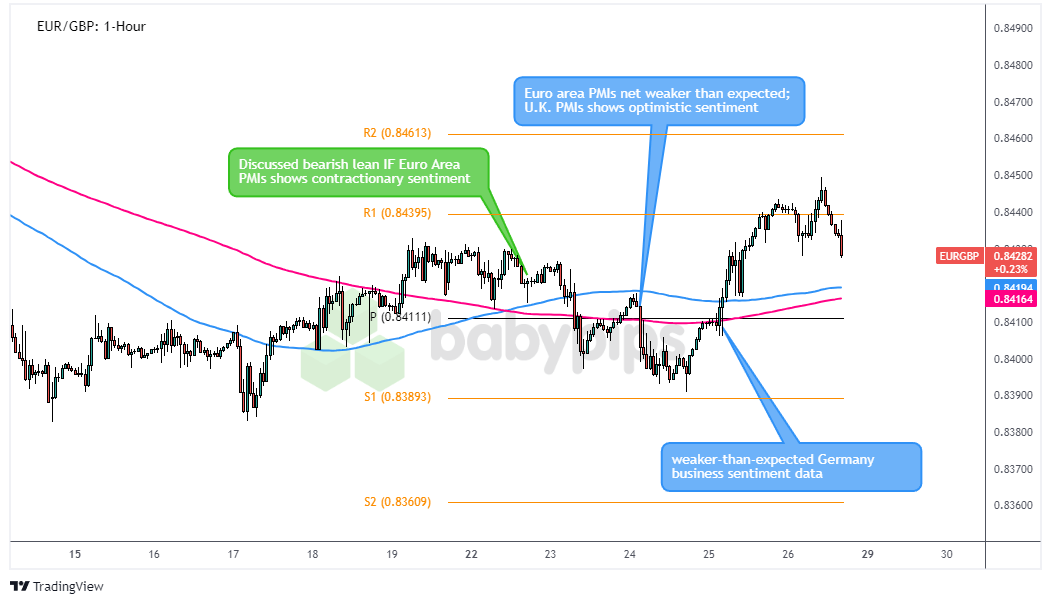

EUR/GBP: Tuesday – July 23, 2024

EUR/GBP 1-Hour Forex Chart by TradingView

On Tuesday, Babypips strategists were focused on the upcoming Eurozone flash PMIs, with a side of potential British business sentiment optimism for flavor. Here’s what we were thinking:

The “Euro Stumble” Scenario: If the Eurozone PMIs showed their manufacturing sector was still stuck in reverse and services were losing their mojo, we figured EUR/GBP might take a tumble faster than a tourist on a London sidewalk, especially if U.K. PMI came in relatively better than Eurozone PMIs.

The “Euro Bounce” Scenario: If the Eurozone data surprised to the upside on net, we figured EUR/NZD may climb higher due to the broad risk-off vibes and Kiwi’s relative weakness lately as the Asia region’s largest influence, China, was showing signs of weakness.

What Actually Happened

Well, folks, Wednesday rolled around, and the Eurozone PMIs decided to throw us a tiny bit of a curveball that would make even the best cricket players jealous.

- Eurozone flash manufacturing PMI: 45.6 (46.0 expected, 45.8 previous)

- Eurozone flash services PMI: 51.9 (52.9 expected, 52.8 previous)

Meanwhile, across the Channel:

- UK flash manufacturing PMI: 51.8 (51.1 expected, previous revised to 50.9)

- UK flash services PMI: 52.4 (52.5 expected, previous revised to 52.1)

The Eurozone numbers were a mixed bag, like a handful of jellybeans where you’re not sure if you’ve got tutti-frutti or earwax flavor. Manufacturing was weaker than expected, but services managed to keep their head above water, albeit barely.

The UK, on the other hand, decided to show off its stiff upper lip, with manufacturing surprising to the upside and services holding steady. It’s like they ordered a full English breakfast while the Eurozone was stuck with continental fare.

Market Reaction

This outcome triggered our arguments for a EUR/GBP bearish bias, which took an immediate dip on the session, dropping roughly 20 pips before finding buyers between 0.8390 – 0.8400.

It was there during the afternoon U.S. session that broad risk sentiment leaned strongly negative, likely lead by the significant selloff in U.S. equities, prompting EUR/GBP to climb back up faster than you can say “God save the King.”

By the end of the week, EUR/GBP was hovering around the .8425 level, caught between our R1 (.8439) and P (.8411) pivot points like a tourist stuck between Buckingham Palace and Big Ben.

The Verdict

So, how’d our crystal ball do? Well, it was about as accurate as British weather forecasting – we got some parts right, but missed a few showers along the way. Our fundamental analysis was spot on, with the Eurozone PMIs indeed showing weakness. However, we underestimated the immense strength in broad risk sentiment as negative risk vibes basically dominated everything this past week, as discussed in our Global Market Recap.

Overall, we’d rate this discussion as “neutral-to-not-likely” in supporting a potential positive outcome. For those who immediately shorted when the fundamental arguments were triggered on Wednesday, they had a chance to see a positive outcome depending on the trade plan selected and how it was executed.

But for those who leaned short after the Wednesday U.S. session through the Friday Asia session, they likely got caught up in the broad risk-off vibes (which almost always benefits the euro over the pound) and likely saw a net negative outcome at the end.

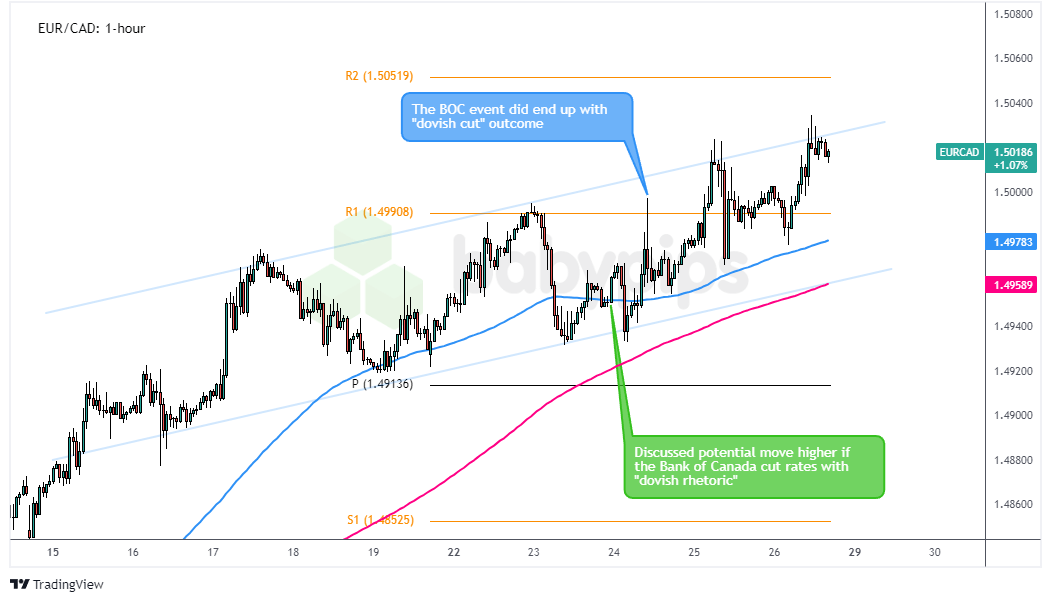

EUR/CAD: Wednesday – July 24, 2024

EUR/CAD 1-Hour Forex Chart by TradingView

On Wednesday, our strategists were focused on the upcoming Bank of Canada (BOC) Monetary Policy Statement, while keeping an eye on Euro area PMIs and broad risk vibes.

The “Loonie Dive” Scenario: If the BOC cut rates by the expected 25 basis points (as discussed in our Event Guide) and hinted at more cuts to come, we figured EUR/CAD might extend its uptrend faster than a hockey player on a breakaway. We were eyeing the previous highs near 1.5000, with potential to hit 1.5050 if the momentum held strong.

The “Hawkish Cut” Scenario: If the BOC’s rate cut came with a lack of downward revisions in economic forecasts and/or absence of additional dovish rhetoric, we figured CAD/CHF may bullishly break out of its consolidation faster than a bear raiding a campsite. We were eyeing a move past the pivot point level (.6500) with potential to reach R1 (.6550) or even the July highs near R2 (.6620).

What Actually Happened

Well, folks, Wednesday rolled around, and the BOC decided to serve up a dish of dovish poutine that would make even the most hardened Quebecois raise an eyebrow.

- BOC cut interest rates by 25 basis points to 4.50% (as widely expected)

- BOC downgraded growth forecast for 2024 from 1.5% to 1.2%

- BOC kept 2024 inflation estimate unchanged at 2.6%, but revised 2025 estimate up from 2.2% to 2.4%

- BOC signaled “further cuts” to come on downside risks from excess supply

Governor Tiff Macklem didn’t mince words, emphasizing that “downside risks are taking on increased weight in our monetary policy deliberations.” He even went as far as saying, “If inflation continues to ease broadly in line with our forecast, it is reasonable to expect further cuts in our policy interest rate.” That’s about as dovish as you can get without actually dressing up as a bird!

And as discussed above, Eurozone numbers were a mixed bag, but arguably net negative and drew a very short-term bearish reaction from traders.

Market Reaction

This outcome triggered our EUR/CAD long bias, which popped higher after the BOC event but quickly found resistance, possibly due to bearish forces on the euro for the session.

But as mentioned above, negative broad risk vibes ran strong this past week, signaled by a selloff in most major risk-on financial markets, as a mix of equity sector rotation and macro economic activity slowdown concerns were likely the main drivers. In this environment, the euro tends to outperform the Canadian dollar.

Overall, we’re giving this discussion a “likely” rating in supporting a potentially positive outcome, mainly due to the market spending most of the week above the discussion price area and above the target event area. Very little trade management complexity would have been needed given the upward momentum.

We didn’t rate it “highly likely” due to the the weak Euro area PMIs outcome, which would have made this a tough gametime decision on going long or not, and we underestimated the strength of the broad risk aversion environment, the main reason this strategy would have worked out.

But that’s how it goes sometimes. The outcome you hoped for still materializes even if it wasn’t in the way you expected and vice versa (like what we saw in EUR/GBP).

All we can do is focus on finding the best probability setups and manage our risk as best we can according to our expectations. With that and good psychology and discipline, hopefully that leads to net positive outcomes over the long-term.