This week our currency strategists focused on the Australian CPI update and the monetary policy statement from the Swiss National Bank for potential high-quality setups.

Out of the four scenario/price outlook discussions this week, two discussions arguably saw both fundie & technical arguments triggered to become potential candidates for a trade & risk management overlay. Check out our review on those discussions to see what happened!

Watchlists are price outlook & strategy discussions supported by both fundamental & technical analysis, a crucial step towards creating a high quality discretionary trade idea before working on a risk & trade management plan.

If you’d like to follow our “Watchlist” picks right when they are published throughout the week, you can subscribe to BabyPips Premium.

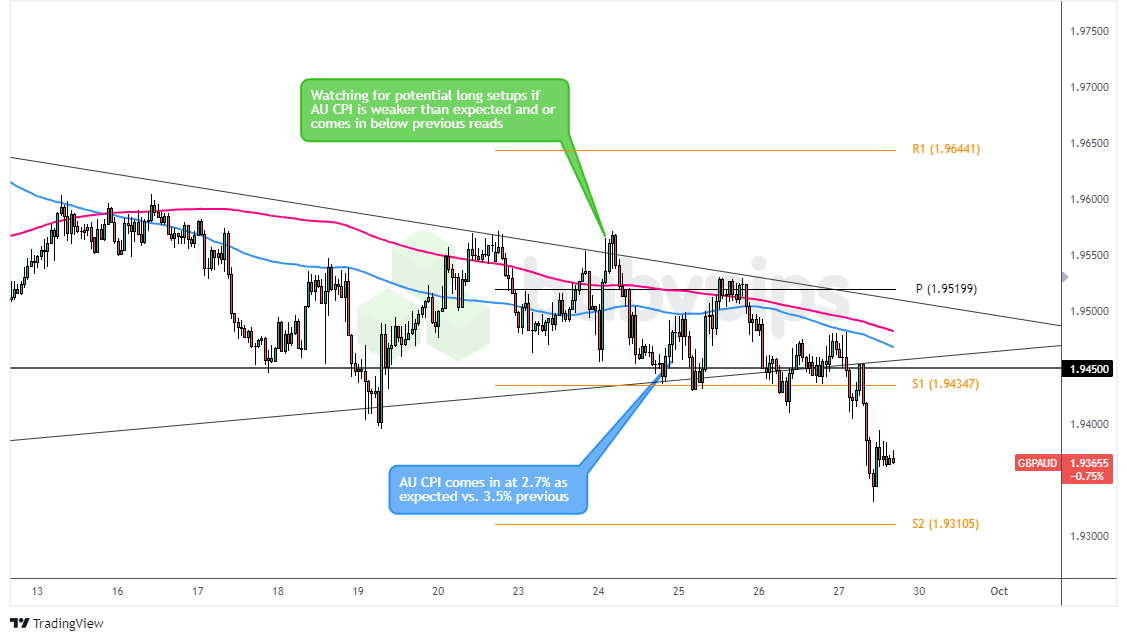

GBP/AUD: Tuesday – September 24, 2024

GBP/AUD 1-Hour Forex Chart by TradingView

On Tuesday, our forex strategists had their sights set on the upcoming Australia CPI release and its potential impact on the Australian dollar. Based on our Event Guide for the CPI report, the markets were expecting headline inflation to slow from 3.5% year-on-year to 2.7% in August, which would still leave annual inflation above the RBA’s target range.

With those expectations in mind, here’s what we were thinking:

The “Aussie Dip” Scenario:

If the CPI came inline or weaker-than-expected or below the previous reading, we anticipated this could draw in fundamental AUD sellers in the short-term. We focused on GBP/AUD for a potential bearish Aussie play as the Bank of England is one of the few central banks resisting rate cuts as much as possible, potentially keeping Sterling buyers interested, and the pair seems to be drawing in technical support at a major area of interest between 1.9400 – 1.9500.

The “Aussie Advance” Scenario:

If Australia’s inflation data surprised to the upside or showed resilience in core measures, we thought this could support the RBA’s relatively hawkish stance and boost the Aussie. In this case, we considered AUD/NZD for potential long opportunities, given the pair’s recent bullish behavior since finding major support around 1.0800 in early September.

What Actually Happened

Well, folks, Wednesday rolled around, and the Australian Bureau of Statistics (ABS) released the August CPI data. The headline inflation came in at 2.7% year-on-year, exactly in line with market estimates and lower than July’s 3.5% increase.

Key points from the CPI report:

- Excluding volatile items and holiday travel, consumer prices rose by 3.0% in August, slower than the 3.7% uptick in July.

- The RBA’s trimmed mean inflation (a measure of underlying inflation) came in at 3.4%, lower than July’s 3.8% annual increase.

- Housing (+2.6%), Food and non-alcoholic beverages (+3.4%), and Alcohol and tobacco (+6.6%) saw the most gains.

- Transport (-1.1%) and Furnishings (-0.9%) helped offset the price increases.

Market Reaction

The initial market reaction to the CPI release saw a brief downswing in the Australian dollar, as traders digested the broadly cooler inflation reading. However, the Aussie quickly recovered its post-release losses, likely due to the consideration that the CPI release was unlikely to change the RBA’s view that inflation “remains too high.”

Looking at our GBP/AUD chart, we can see that the pair initially saw a small bounce following the CPI release, climbing to retest the strong area of technical confluence between the Pivot point and the falling highs pattern.

As the week progressed, GBP/AUD reversed back lower, finding support around the S1 Pivot support area, but eventually breaking below the S1 pivot point and the 1.9400 psychological level.

Interestingly, the GBP/AUD’s downward trajectory was influenced by several factors throughout the week:

- China’s monetary and fiscal stimulus announcements early in the week provided support for the Aussie and broad risk-on sentiment..

- The RBA’s decision earlier in the week to hold rates steady at 4.35% initially boosted AUD, although some of these gains were pared back following the Governor’s comments on productivity concerns and subdued GDP growth.

- Positive U.S. mid-tier data releases on Thursday lifted risk assets, including AUD, across the board.

- Friday’s tightened volatility ahead of the U.S. Core PCE Price Index data, followed by a risk-on sentiment after its release, further supported AUD against GBP.

The Verdict

So, how’d we do? In our original discussion, we mentioned potential long setups on GBP/AUD if the Australia CPI came in weaker than expected. While the CPI did come in lower than the previous month, it matched market expectations exactly. This resulted in a brief bullish move for GBP/AUD, but it wasn’t sustained.

We mentioned two technical setups, including a sustained upside trade above the 1.9600 psychological handle that may draw in technical bulls, or a pullback to the trend line support near the S1 (1.9435) Pivot Point, where buying support may form.

The upside break scenario never had a chance to play out, but the formation of buying behavior around 1.9450 did, several times in fact. Unfortunately, only the first bounce from that area could have played out positive, while the following retests would have likely turned out negative, making the trading plan selected and real-time execution decisions as big factors on this trading outcome.

Because of the execution factor, we’d rate this discussion as “unlikely-to-neutral” to have supported a net positive outcome, mainly given that the market closed below both discussion price and event price, but there was a chance to have grabbed some pips for skilled, active traders.

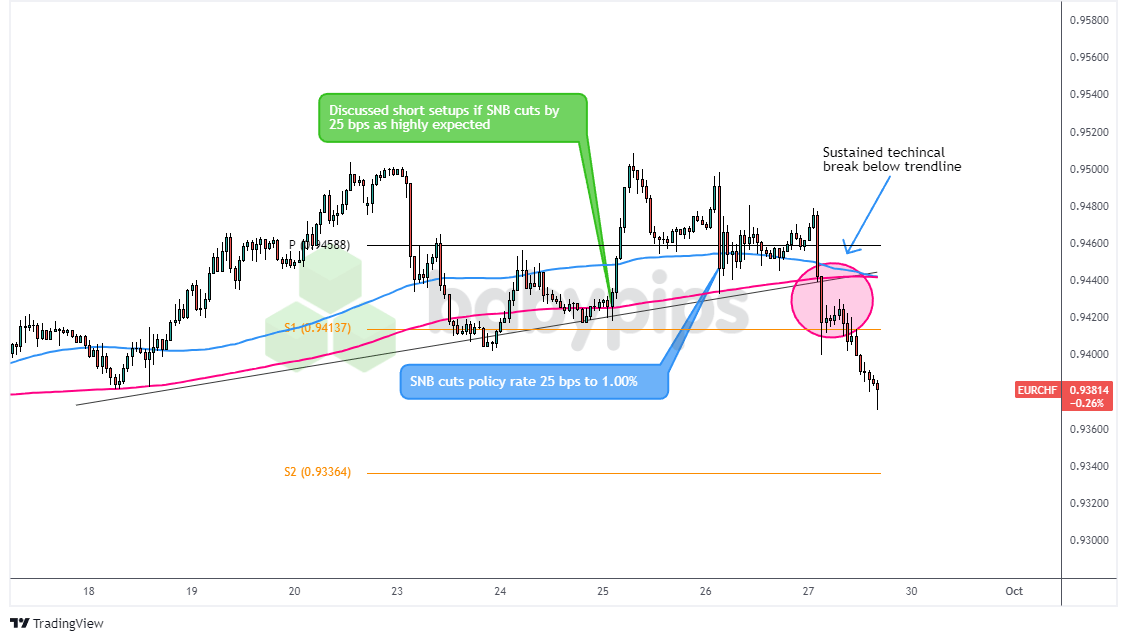

EUR/CHF: Wednesday – September 25, 2024

EUR/CHF 1-Hour Forex Chart by TradingView

On Wednesday, our strategists had their sights set on the Swiss National Bank (SNB) Monetary Policy Statement and its potential impact on the Swiss franc. Based on our Event Guide, expectations were for a 25 basis point rate cut from 1.25% to 1.00%, with possible downward revisions to inflation forecasts and potential currency intervention threats.

With those expectations in mind, here’s what we were thinking:

The “Safe-Haven Surge” Scenario:

If the SNB delivered the expected 25 bps cut, we thought this outcome would actually draw in SNB bulls. This outcome was likely already priced in the market, so if it played out in the way, we saw strong odds of traders taking profits on CHF shorts.

We paired this outlook with the euro, given the recent string of net negative Euro area data, likely supporting more rate cuts ahead speculation and pressure on the euro in the short-term.

The “Franc sell” Scenario:

If the SNB delivered the expected 25 bps cut and signaled a more aggressive easing cycle or possibly currency intervention, we anticipated this could weigh on the CHF. We eyed GBP/CHF given the relatively hawkish stance on inflation and rates from the Bank of England, as well as the strong bullish price action in the pair recently.

What Did the Data Say

On Thursday, September 26, the Swiss National Bank announced its monetary policy decision:

-

The SNB cut its policy rate by 25 basis points to 1.00%, as widely expected.

Inflation forecasts were significantly reduced:- 2024: From 1.3% to 1.2%

- 2025: From 1.1% to 0.6%

- GDP growth forecast at around 1% for 2024, rising to 1.5% for 2025.

- The bank remained willing to intervene in foreign exchange markets as necessary.

- Outgoing Chairman Thomas Jordan hinted at the possibility of more rate cuts in the future.

Market Reaction

The initial market reaction to the SNB statement release saw a brief strengthening of the Swiss franc across the board, which was inline with our “buy-the-rumor, sell-the-news” base case, triggering our fundamental argument to watch EUR/CHF.

However, the pair’s downward momentum was short-lived. As the press conference progressed and outgoing Chairman Jordan hinted at the possibility of more aggressive easing, EUR/CHF found support and began to climb.

The climb higher was limited as well, likely due to bearish sentiments on both currencies battling it out until the Friday session. It was on Friday where the bears took control, likely a reaction to sub 2% inflation readings from France and Spain that sent the euro spinning lower, prompting EUR/CHF to break technical support levels and trigger our technical bearish bias on the pair.

The Verdict

In our original discussion, we mentioned potential short setups on EUR/CHF based on the idea that a negative outcome was likely priced in and that if the only cut by 25 bps, there could be a “buy-the-rumor, sell-the-news” reaction.

Now we did note that if the SNB signaled a more aggressive easing cycle, which it did through Chairman Jordan’s comments about possible future rate cuts, fundamental bears could have taken control.

Given that the CHF reaction was bullish, we would have likely lean that way, and when the pair broke to the downside on Friday, the odds of a successful trade were pretty strong, especially with a bearish euro catalyst.

Overall, we think it’s “likely” that the discussion was net supportive of a positive outcome, but given that the move was limited to Friday’s price action, the run lower was capped before the weekend close.