This week our currency strategists focused on the Euro area CPI update and the U.S. Manufacturing PMI update for potential high-quality setups.

Out of the four scenario/price outlook discussions this week, one discussion arguably saw both fundie & technical arguments triggered to become a potential candidate for a trade & risk management overlay. Check out our review on those discussions to see what happened!

Watchlists are price outlook & strategy discussions supported by both fundamental & technical analysis, a crucial step towards creating a high quality discretionary trade idea before working on a risk & trade management plan.

If you’d like to follow our “Watchlist” picks right when they are published throughout the week, you can subscribe to BabyPips Premium.

EUR/GBP: Monday – September 30, 2024

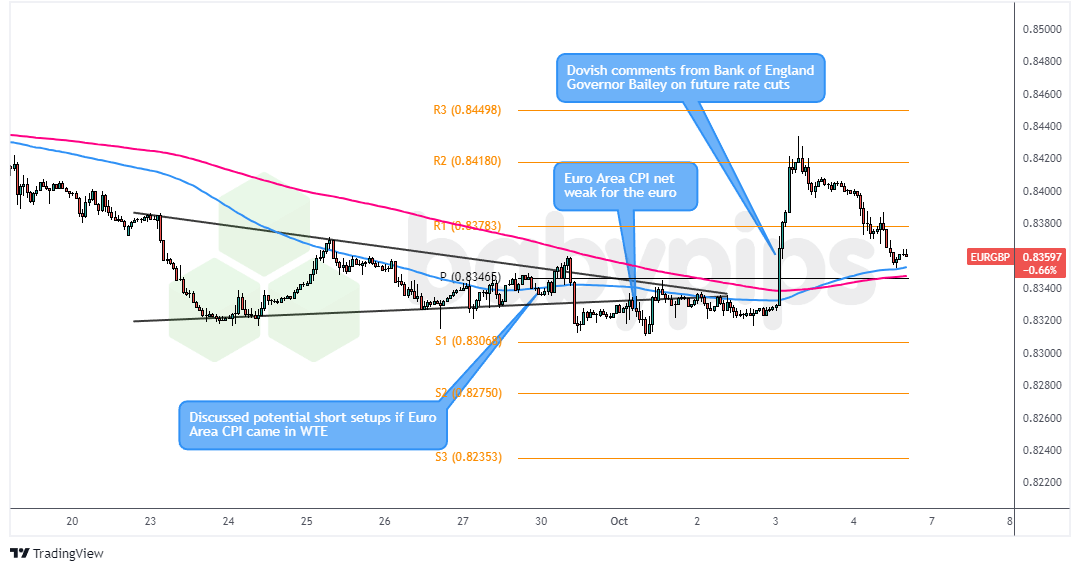

EUR/GBP 1-Hour Forex Chart by TradingView

On Monday, our forex strategists had their sights set on the upcoming Euro Area CPI release and its potential impact on the euro. Based on our Event Guide for the Euro Area Flash CPI Reports, the markets were expecting headline inflation to come in at 1.9% y/y (vs. 2.2% previous) and core inflation at 2.7% y/y (unchanged from previous).

With those expectations in mind, here’s what we were thinking:

The “Euro Surge” Scenario:

If the CPI came in higher than expected, we figured this could ease pressure on the ECB to cut rates in October. We thought this could draw in fundamental EUR buyers, and we had our eyes on EUR/CAD for potential long strategies, especially given the pair’s recent upward momentum and the Bank of Canada’s recent dovish signals.

The “Euro Slide” Scenario:

If Euro Area inflation came in weaker than expected, we anticipated this could increase expectations for an ECB rate cut in October. We eyed EUR/GBP for potential short strategies, as the pair was testing resistance at the top of a recent range, and the Bank of England had maintained a more hawkish stance due to relatively sticky inflation conditions in the U.K.

What Actually Happened

Well, folks, Tuesday rolled around, and the Euro Area CPI decided to throw us a mixed bag of results. The flash estimates from Eurostat showed that the annual inflation rate in the Euro area dropped to 1.8% in September, down from 2.2% in August and slightly below the expected 1.9%. The core inflation rate held steady at 2.7% y/y, in line with expectations.

Key points from the CPI report:

- Energy prices continued to be the main driver of disinflation, falling 3.3% y/y

- Food, alcohol & tobacco inflation eased to 5.4% from 6.4% in August

- Services inflation slowed to 4.1% from 4.4%

- Non-energy industrial goods inflation remained stable at 4.1%

Market Reaction

The initial market reaction to the CPI release saw weakening of the euro across the board. While the underlying metrics in the flash CPI update showed relatively high inflation rates, the sub-2% headline number plus weak Euro area PMIs were likely the main bearish drivers of the day.

Looking at our EUR/GBP chart, we can see that the pair initially saw a small dip but found buyers just above the S1 Pivot support area. It’s likely this week’s broad risk aversion sentiment may have played a role in putting pressure on risk assets, like the British pound, sparking choppy behavior in EUR/GBP until the Thursday session.

On Thursday, BOE Governor Bailey surprised the markets with a dovish turn in sentiment on the future interest rates, saying that the central bank could ease aggressively if inflation remains subdued. This pushed sterling off a cliff to one of its worst days of the year, and EUR/GBP up over a massive 3 daily ATR higher.

The Verdict

So, how’d we do? In our original discussion, we mentioned potential short setups on EUR/GBP if the Euro Area CPI came in weaker than expected, which it did. But the broad risk-off environment favored low-yielding assets like the euro vs. risk-on assets, putting a lid on any downside moves this week.

Plus the surprise comments from Bank of England Governor Bailey knocked Sterling down for the count this week, making any short plays on EUR/GBP very unlikely of recovering, with exception to those who took shorts at the R2 Pivot resistance area.

So overall, we’d rate this discussion as “not likely” supportive of a potential positive outcome because while the weak headline Euro area CPI update did bring pressure to EUR/GBP initially, external factors like risk environment and central bank commentary pushed the price well above discussion levels and trigger levels to likely hit most invalidation arguments if good trade management practices were used.