Central bank events and inflation data appeared to be the main drivers for FX this week, and likely why currency price action was relatively limited to choppy, short-term moves as traders waited on the sidelines.

Overall, the Aussie dollar took the top spot thanks to high inflation updates and rate hike speculation, while traders looked bearish on the euro all week, possibly on low expectations of rate hike rhetoric and weak economic updates from the Euro area.

Notable News & Economic Updates:

Moderna says covid shot for younger kids showed strong results

Turkish lira bounces back from record low on Tuesday after Erdogan soothes diplomatic fears

Bank of Canada accelerates potential timing of rate hikes top possibly Q1 or Q2 of 2022

European Central Bank holds stimulus operations at €1.85T; will keep through March 22 or later if needed

U.S. shows weakest quarter of growth on supply woes; Advanced read of third quarter GDP at 2.0% vs. 6.7% in Q2

Bank of Japan holds monetary policy as-is as it lowered outlook for growth & inflation

China Evergrande is said to make another bond payment, avoiding default for a second time.

GDP up by 2.2% in the euro area and by 2.1% in the EU; Eurozone inflation rises to 4.1% in Oct. (13-year high)

FDA authorizes Pfizer’s Covid vaccine for kids ages 5 to 11

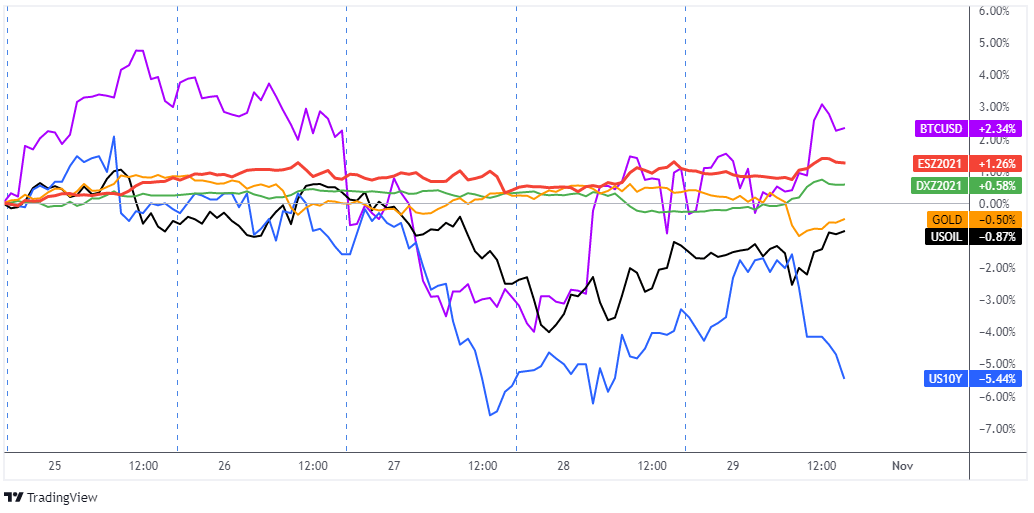

Intermarket Weekly Recap

Price action was a mixed bag this week across the financial markets as each asset class seemed to be moving to the beat of their own drums.

Equities stayed green this week with another net positive round of earnings releases, while bond prices rose/bond yields fell on Wednesday, possibly on lowered expectations of Fed tightening as we saw weak U.S. export data and retailer supply data hint at a lower growth outlook. Also risk sentiment was arguably negative to start the week, likely on the continued Chinese property developer issues and fears of debt defaults.

Oil fell earlier this week but eventually found a bid, likely on comments from OPEC who forecasted that a tighter global oil market may be ahead in the fourth quarter. U.S. inventory data was also a likely contributor to the bounce in oil prices (market nearly retested $80/barrel on WTI) as it showed supply shrink rapidly (supply fell by 1.81M barrels last week.

In the crypto space, bitcoin pulled back from all-time highs as ETF euphoria likely faded. This seemed to have pulled most of the crypto space with it, with exception to meme coins. Shiba Inu (SHIB) coin once again rocketed higher to new all-time highs after last week’s consolidation, gaining over 100% intraweek before pulling back. It’s likely the push for Robinhood to list the meme coin is the main catalyst, and seems to be dragging other meme coins higher with it like the previous meme coin king, Dogecoin.

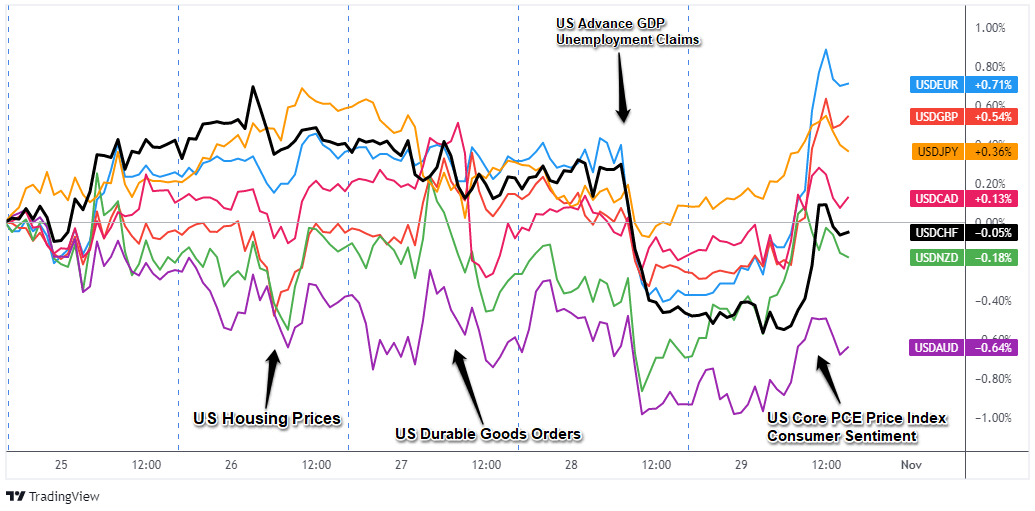

Looking at the FX charts below, we can see that the forex markets traded mostly sideways, with few pops of volatility here and there. It appears this week’s round of inflation updates and central bank events were the main focus for currency traders, and likely kept many on the sidelines to avoid possible event risk.

There were no major surprises as all central banks held off from interest rate changes for now and most re-iterated uncertainty with inflation expectations, but the Bank of Canada did shake things up a bit by ending their bond buying program on Wednesday. They also hinted that interest rate hikes may come sooner than expected, possibly in the first or second quarter of 2022.

USD Pairs

The Chicago Fed National Activity Index fell to minus 0.13 in September from 0.05 in August

Texas Factory Production eased in October to 18.3 from 24.2 in September — Dallas Fed

U.S. new home sales hit six-month high as the median price stays above $400K

Richmond Fed Manufacturing index for October rises to 12 vs. -3 in September

New orders for U.S. manufactured durable goods in September decreased $B or 0.4% to $261.3B

U.S. pending home sales fell unexpectedly by -2.3% in September

U.S. advance GDP for Q3 2020: 2% vs. 2.8% forecast; weekly jobless claims fell to 281K vs. 289K forecast

U.S. core PCE price index increased 3.6% for a fourth straight month

University of Michigan Consumer Sentiment for October: 71.7 vs. 72.8 previous

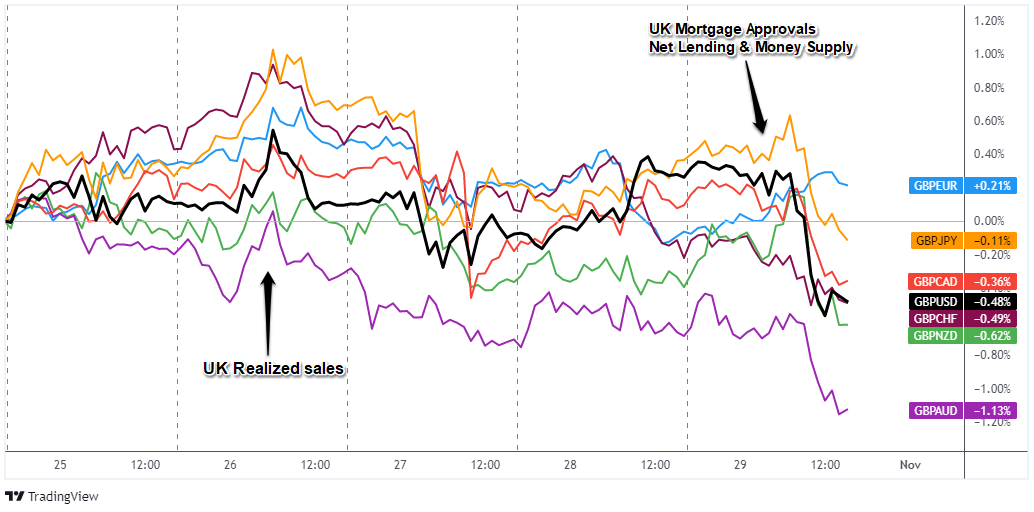

GBP Pairs

Bank of England’s Tenreyro says needs time to think about rate hike

U.K. serious covid cases hit levels last seen in March

U.K. Chancellor delivers $103B of stimulus to boost economy

U.K. slams France’s Brexit threats over fishing as tensions rise

UK mortgage approvals hit 14-month low as tax break ends; 72,645 in September from 74,214 previous

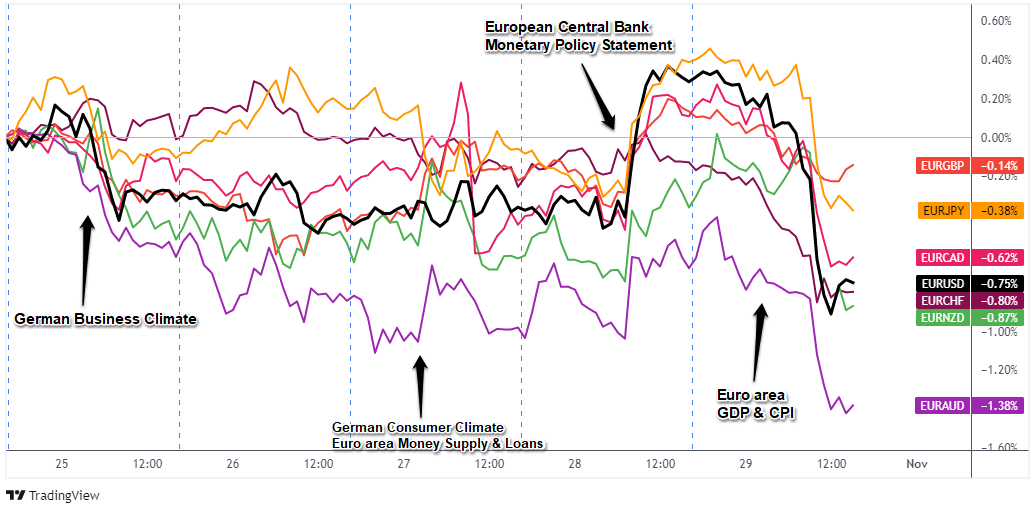

EUR Pairs

Spain’s central bank chief Pablo Hernandez de Cos said on Monday that high inflation may persist

German Ifo business climate index down from 98.8 to 97.7 vs. 98.2 forecast

German growth to slow sharply in final months of 2021 – Bundesbank says

German industrial exports hurt by raw material supply problems – Ifo

German unemployment fell by 39K in seasonally-adjusted terms to 2.46M in October

Germany preliminary GDP in the 3rd quarter of 2021 up 1.8% on the previous quarter

France preliminary GDP in Q3: +3.0%; CPI +2.6% in October

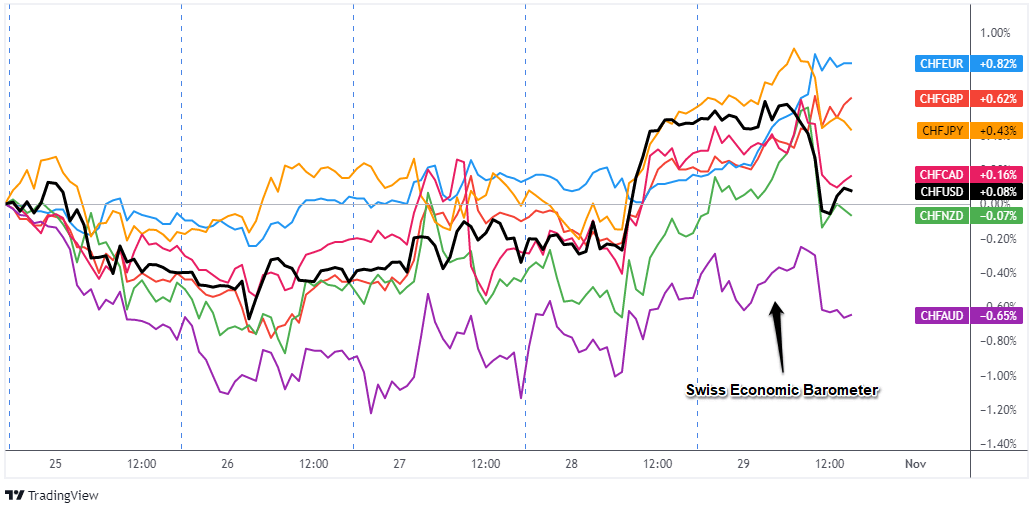

CHF Pairs

Green Economy push may affect effectiveness of Swiss National Bank’s monetary policy – Andrea Maechler

Swiss KOF Economic barometer: 110.68 vs. 111.0 previous

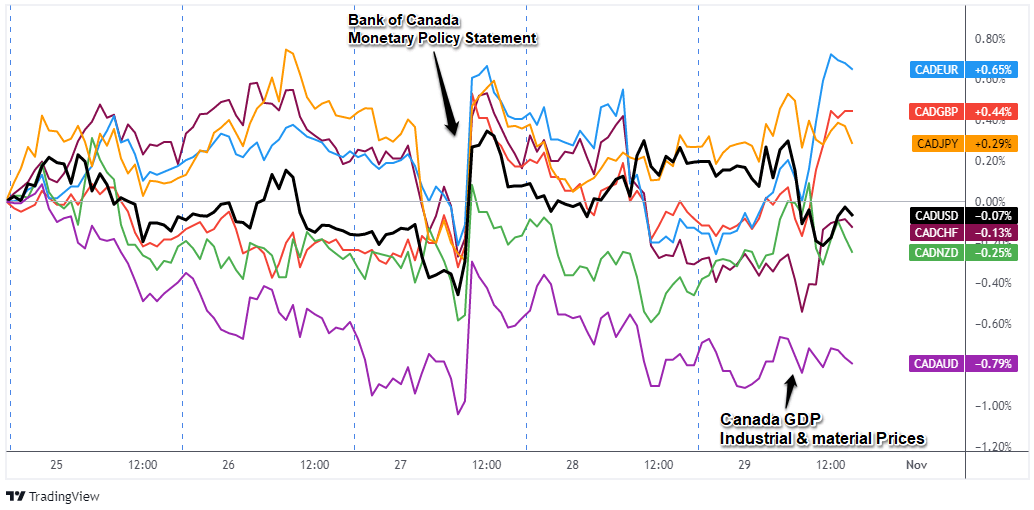

CAD Pairs

Canada Sept wholesale trade most likely rose 1.1% – Statscan flash estimate

Bank of Canada accelerates potential timing of rate hikes; ends bond buying program on Wednesday

Canada Industrial Product Price Index : +1.0% m/m in Sept; Raw materials: +2.5% m/m in Sept.

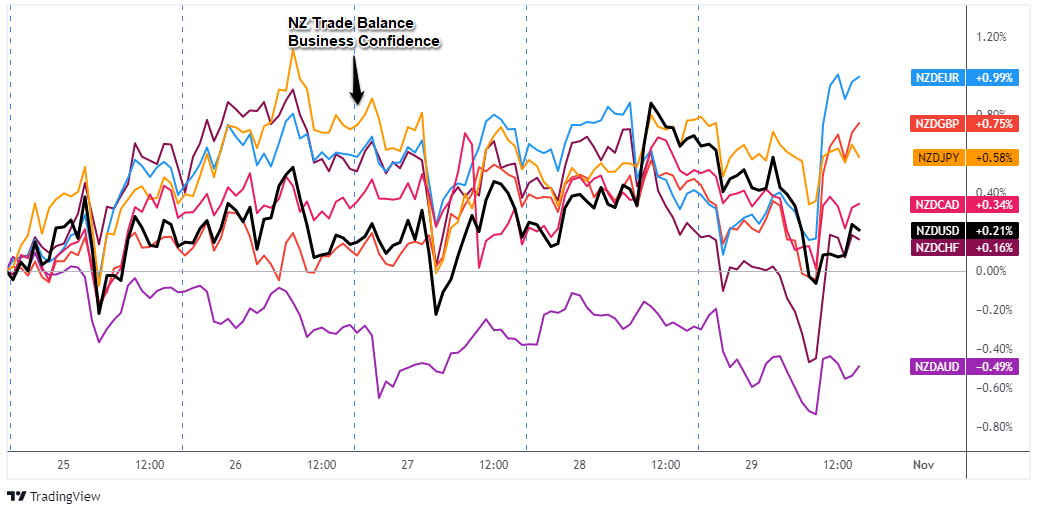

NZD Pairs

New Zealand Trade Balance: Imports rise to $6.6B in September vs. $4.4B in exports; third consecutive record month for imports

New Zealand business confidence falls in October as 13.4% of survey respondents expected economy to weaken.

ANZ: NZ consumer confidence falls 7 points to 98 as Covid-19 restrictions continue

RBNZ Governor Adrian Orr shows tightening bias with call on financial institutions to use their balance sheets to support economic recovery

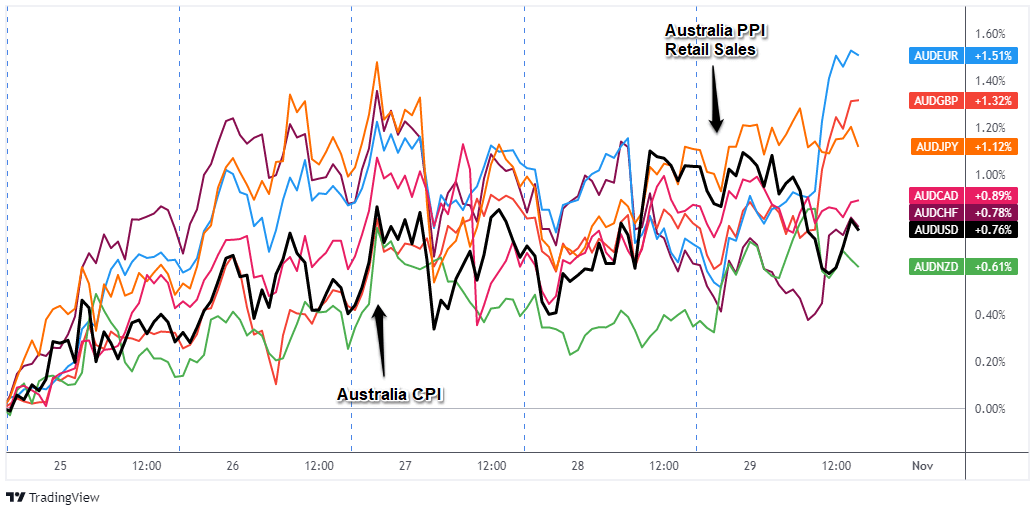

AUD Pairs

Australia Q3 CPI rises 0.8% q/q, 3.0% y/y; core inflation rises by 2.1% vs. 1.8% forecast

Australia export prices climb 6.2% on quarter in Q3, slowing from 13.2% in Q2; Import prices rose 5.4% vs. 1.9% previous

Australia PPI expands 1.1% on quarter in Q3

Australia retail sales climb 1.3% in September as economy reopens

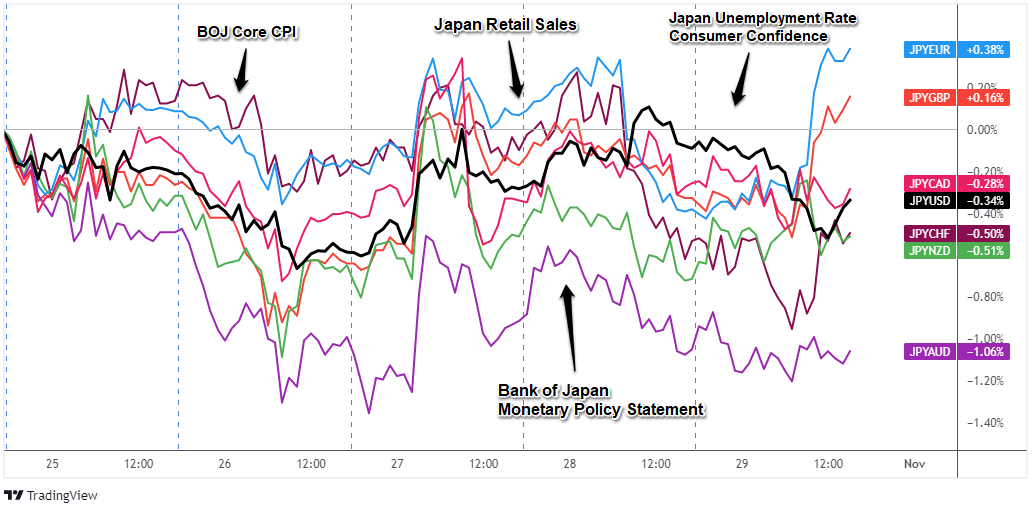

JPY Pairs

Bank of Japan holds monetary policy & sees inflation below 2% target for at least two years

Bank of Japan says it will not be influenced by the actions of moves by other central banks

Japan’s jobless rate unchanged at 2.8% in Sept

Japan consumer confidence falls to 39.2 vs. 37.8 previous

Japan Housing Starts at 4.3% vs. 7.5%