The Greenback was king among the major currencies once again, likely benefiting from sour economic data and sentiment updates.

Traders seemed to have been mainly focused on the weak economic data from China, plus another round of record high inflation updates, likely prompting an outlook that central banks will continue to be aggressive with monetary policy tightening going forward.

Notable News & Economic Updates:

China data dump on Monday:

- China’s July industrial production grew by 3.8% y/y vs. 4.6% expected, 3.9% previous

- China’s fixed-asset investment up by 5.7% ytd/y vs. 6.2% expected, 6.1% previous

- China’s retail sales improved by 2.7% y/y vs. 5.0% expected, 3.1% growth in June

- New home prices in China’s 70 major cities dropped by 0.9% y/y in July

- China’s retail sales improved by 2.7% y/y vs. 5.0% expected, 3.1% growth in June

U.S. lawmakers arrived in Taiwan despite current tensions with China; China stages new military drills near Taiwan

Meme stock mania briefly returned this week after Bed Bath & Beyond (BBBY) rallied from $13 to $30 and back on position updates from RC Ventures (GameStop Chairman Ryan Cohen’s venture capital firm)

U.K. CPI date for July came in super hot: +10.1% y/y vs. +9.8% y/y expected

EIA crude oil inventories fell by 7.1 million barrels

The United States and Taiwan have announced plans to begin formal trade negotiations in the Fall – Office of US Trade Representative

Ethereum developers back Sept. 15 Target for blockchain software ‘merge’

More central bank rate moves this week:

- People’s Bank of China unexpectedly cut interest rates by 10 bps to 2.75% on Monday

- The Reserve Bank of New Zealand raised the OCR by 50 bps to 3.00%

- Norway’s central bank hiked the deposit rate by 50bps to 1.75%

- The Philippine central bank hiked the key interest rate by 50bps to 3.75% on Thursday

- Turkey’s central bank shocked traders with a 100 bps rate cut to 13.00% despite soaring inflation

Mixed rhetoric from Fed officials this week after St. Louis’s James Bullard called for another 75bps hike while Kansas City’s Esther George says the pace of rate increases may slow

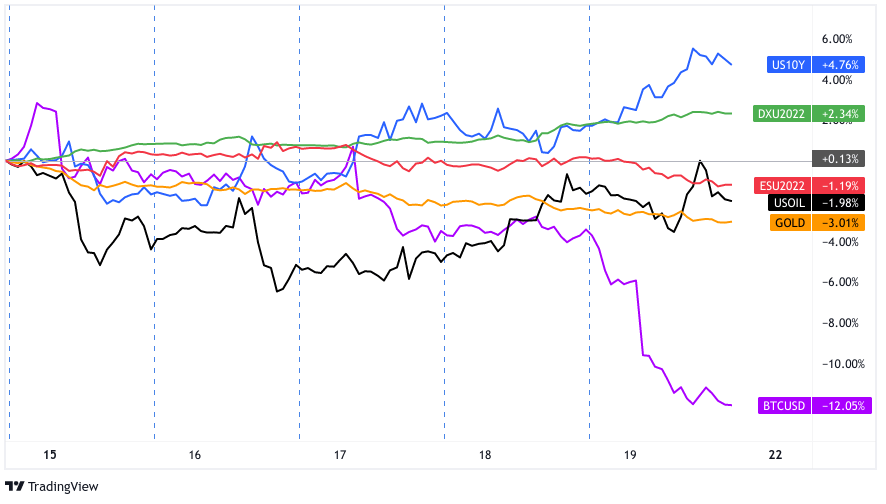

Intermarket Weekly Recap

Dollar, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay 1-Hour

It was a slow and steady grind for price action this week despite a pretty heavy calendar of major economic updates.

It’s likely that this week’s round of data wasn’t much of a surprise as we continued to see weak growth updates, signs that prices are still growing at a way too fast pace, and that central banks will continue to tighten aggressively for the foreseeable future.

Most notable and probably the biggest driver of sentiment this week was the economic data dump from China on Monday, most of which not only came in below previous reads, but also weaker-than-expectations.

Business sentiment also came in pretty sour this week, highlighted by a reading from the German ZEW economic confidence index hitting the lowest level since 2008 at -55.3.

Inflation updates seemed to have a big influence this week, and the most notable data point from the bunch came from the U.K. It was there that we saw another record number as the U.K. saw its CPI hit 10.1% y/y in July, the highest read in 40 years! Germany also came out with a scary inflation read as its producer prices index grew +5.3% in just one month!

All put together, and when combined with not only a round of interest rate hikes from around the world, and rhetoric from central bank officials that they will stay vigilant in fighting inflation, it’s no wonder why we saw the U.S. dollar take charge early in the week, followed by bond yields.

At the same time, risk assets turned lower, with equities bucking the trend, likely continuing the technical recovery, and some speculation we may have hit peak inflation.

But that trade seems to have turned on Friday, likely on some arguing that the bear market bounce is overextended short-term after a 4-week rally, and/or speculation interest rates will continue to rise, likely to put pressure on equities ahead.

In the FX space, price action seems to have been mainly influenced by broad risk sentiment as the Kiwi and the Aussie fell behind the pack, despite a rate hike from the RBNZ and a tick lower in Australia’s unemployment rate.

The pound was a big loser as well, only gaining against NZD, as consumer confidence hits a record low and expectations of a recession are high in the U.K.

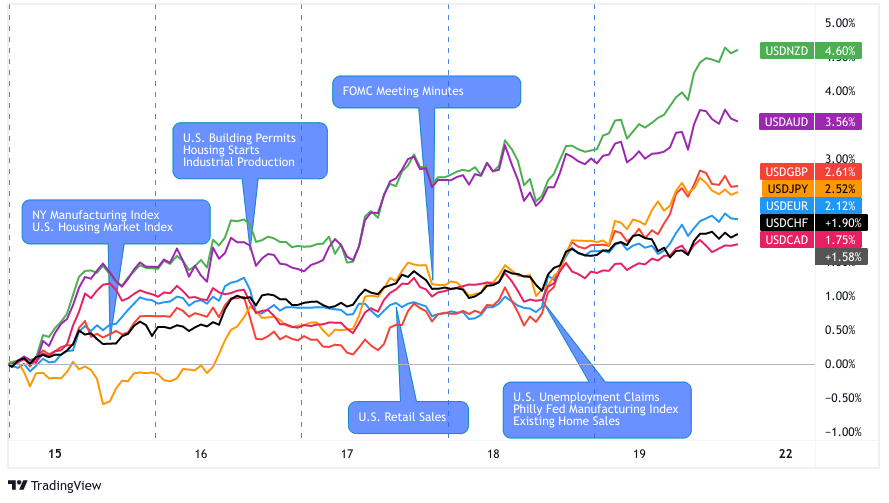

USD Pairs

Overlay of USD Pairs: 1-Hour Forex Chart

The National Association of Home Builders/Wells Fargo Housing Market Index dropped to 49 in August vs. 54 in July

Empire State manufacturing index tumbled from 11.1 to -31.3 vs. 5.1 forecast

U.S. Housing starts fell to 1.446M in July from 1.599M in June; building permits issued fell to 1.674M vs. 1.696M previous

U.S. Industrial production for July: +0.6% m/m vs. 0.0% previous

On Tuesday, President Joe Biden signed the $739B Inflation Reduction Act into law.

U.S. retail sales for July: 0.0% m/m vs. 0.8% m/m previous; core retail sales 0.4% m/m vs. 0.9% previous

MBA Weekly mortgage applications fell -2.3% w/w in the week ending Aug. 12

FOMC Meeting Minutes:

- Rates would have to hit “sufficiently restrictive” level then remain

- Spending and production have softened, but jobs gains robust

- Inflation conditions remains elevated

U.S. existing home sales fell 5.9% y/y to 4.81M in July vs. 5.11M in June

U.S. mortgage rates fell to 5.13% last week – Freddie Mac

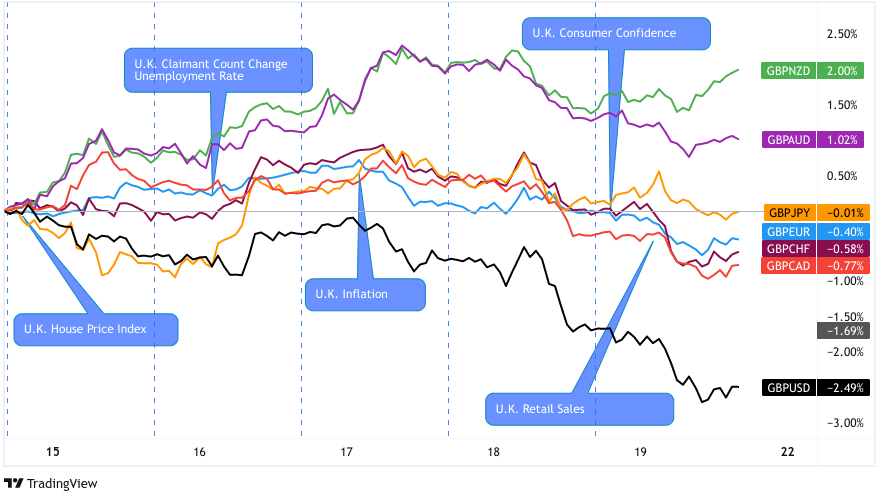

GBP Pairs

Overlay of GBP Pairs: 1-Hour Forex Chart

U.K. House prices fell by -1.3% in July to an average price of £365,173; the first price drop in 2022

U.K. average earnings index up by 5.1% vs. 4.5% forecast, 6.4% previous; U.K. jobless rate unchanged at 3.8% as expected

Soaring food and energy costs drive UK inflation to new 40-year high of 10.1% y/y in July

Bank of England announced out plans on Thursday to sell $23B corporate bond stockpile

U.K. consumer confidence hits a record low of -44 in August amid ‘acute’ cost-of-living concerns

U.K. public borrowing at 4.94B GBP in July, more than 2.8B GBP expected as PM contenders promise more help

U.K. retail sales were up by 0.3% m/m vs. -0.2% m/m previous; gets boost from online shopping in July

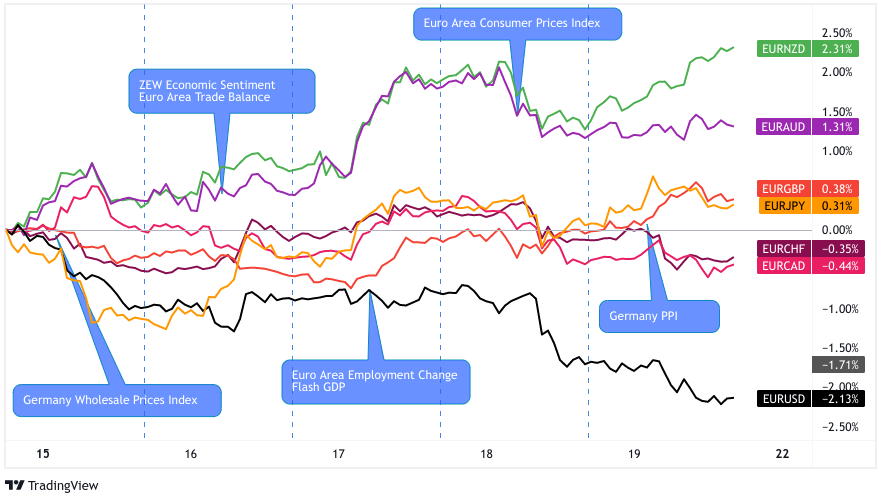

EUR Pairs

Overlay of EUR Pairs: 1-Hour Forex Chart

German ZEW Economic sentiment index: dips to -55.3 in August vs. -53.8 forecast

On Tuesday, Germany decided to keep three nuclear plants open, reducing reliance on Russian gas

Eurozone’s 30.8B EUR trade deficit reflects higher energy costs in June

According to Eurostat, GDP was up by 0.6% q/q & employment up by 0.3% q/q in the euro area; In the EU, GDP up by 0.6% q/q & employment up by 0.3% q/q

Final read for Eurozone CPI in July: +8.9% y/y

German annual producer prices climb 37.2%, the highest increase on record; +5.3% m/m

Euro area Current account recorded €4B surplus in June 2022, up from -€7B deficit in previous month

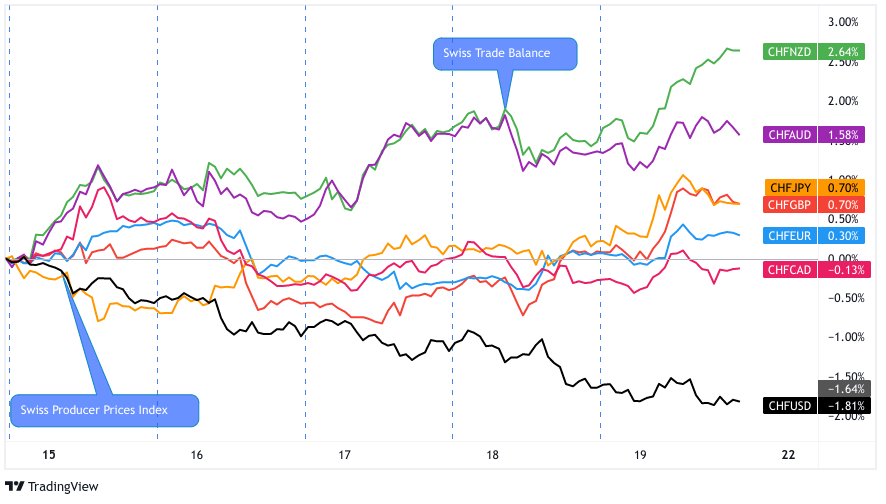

CHF Pairs

Overlay of CHF Pairs: 1-Hour Forex Chart

Swiss producer & import prices in July: -0.1% vs +0.3% m/m previous

Swiss sight deposits increase by 1.7B Swiss francs ($1.80B) last week showing possible central bank activity

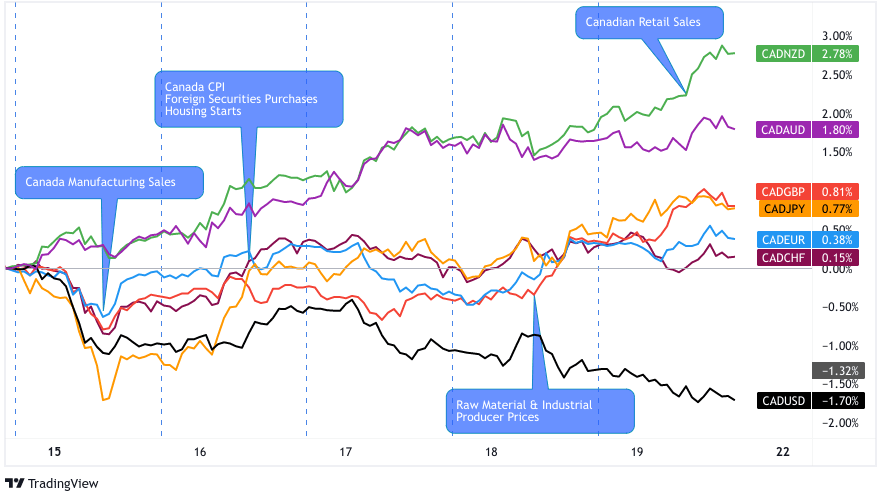

CAD Pairs

Overlay of CAD Pairs: 1-Hour Forex Chart

Canadian manufacturing sales slipped by 0.8% vs. a projected 0.7% decline

Canada CPI rose 7.6% y/y in July; +0.1% m/m

Foreign investors’ holdings of Canadian securities in June: -$17.5B vs. a revised higher $2.83B increase in May

Bank of Canada Governor Macklem says more work to do despite cooler inflation read

Canadian retail sales unexpectedly strong in June at 1.1% m/m vs. 0.4% forecast, Core retail sales down to 0.8% m/m vs. 1.9% previous & 0.9% expected

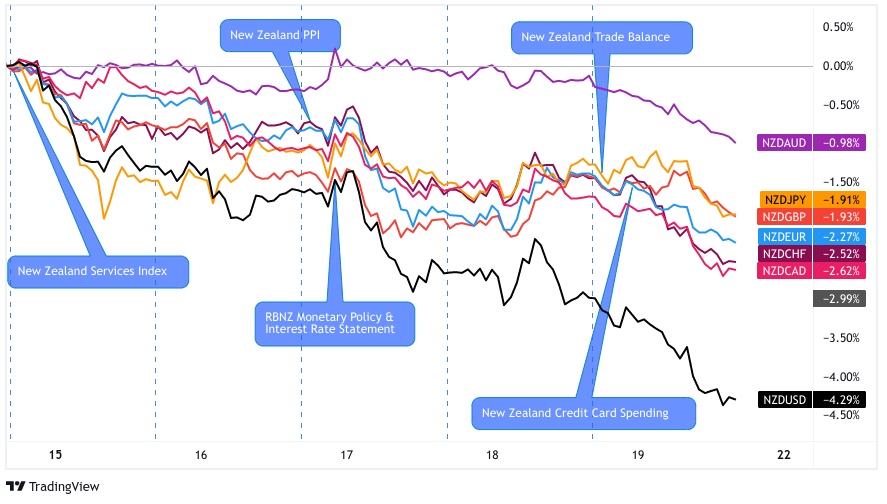

NZD Pairs

Overlay of NZD Pairs: 1-Hour Forex Chart

BusinessNZ services index lower from 54.7 to a five-month low of 51.2 in July

Global dairy prices fell at a slower pace at -2.9% vs. the previous auction at -5.0% on Aug. 2

RBNZ raises interest rates by 50 bps to 3.00% as expected; warns of future hikes being brought forward

NZ producer price outputs rise 2.4% in Q2

RBNZ Governor Orr testified to Parliament; apologized for how low-interest rates sent inflation to 32-year high

NZ posts 1.1B NZD trade deficit (vs. 0.5B surplus expected) as imports outpace exports in July

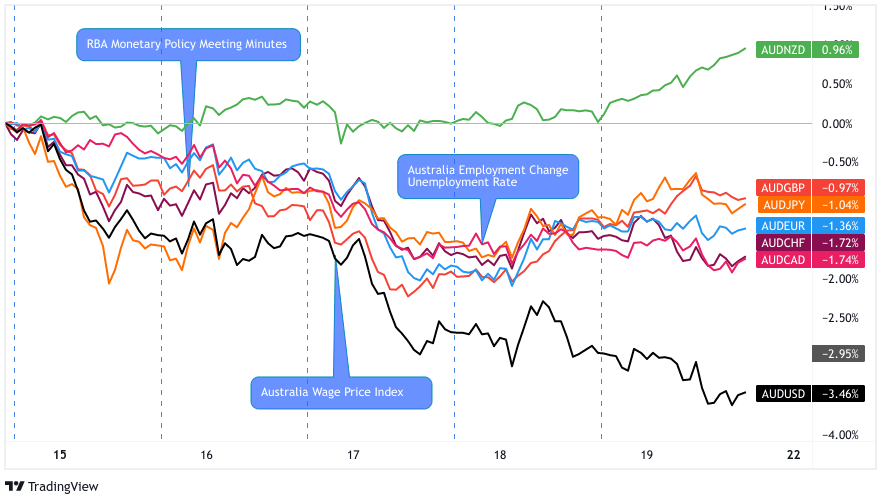

AUD Pairs

Overlay of AUD Pairs: 1-Hour Forex Chart

Reserve Bank of Australia meeting minutes kept options open for September rate hike, but emphasized that it’s not on a pre-set path.

AU wage growth up by 2.6% in the year to June – the fastest since Sept 2014 – but still lagged behind inflation

Australian economy lost 40.9K jobs in July vs. estimated 26.5K gain; jobless rate improved from 3.5% to 3.4%

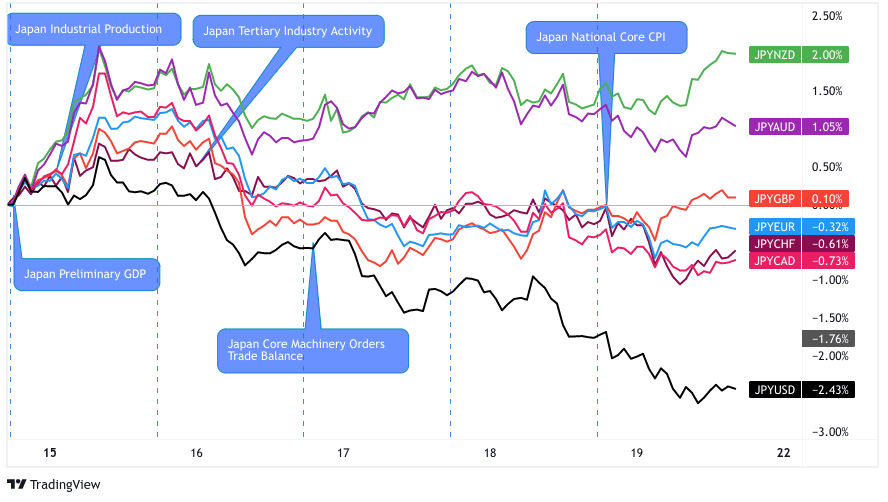

JPY Pairs

Overlay of Inverted JPY Pairs: 1-Hour Forex Chart

Japan’s GDP expands by 0.5% in Q2 after Covid curbs lifted; annualized rate of 2.2% exceeds pre-COVID level

Japan’s final industrial production up by 9.2% in June vs. 7.5% uptick in May

Japanese tertiary industry activity fell by 0.2% vs. expected 0.3% gain

Japan core machinery orders rise 0.9% vs. 1.3% uptick expected in June

Japanese Tankan manufacturing index rose to a 7-month high of 13 in Aug (vs. 9 previous)

Japan inflation rate at 2.4% y/y, the highest in near 8 years