U.K. drama, global inflation updates and central bank commentary were all in play this week, and likely why intermarket price action was mixed for the most part.

In terms of forex, the Kiwi easily took the top spot this week, likely fueled by an incredibly hot inflation read from New Zealand, while the Greenback fell to last place among the majors. This was solidified on Friday on rumors of some Fed members fearing the risks of over tightening.

Notable News & Economic Updates:

In its second round of airstrikes in a week, Russia used drones to attack Ukrainian cities, killing at least four people in an apartment building in the heart of Kyiv during the morning rush hour.

Ukraine said that Russia had destroyed almost a third of its power plants in the last week as part of a campaign to attack infrastructure before winter.

Oil fell on Tuesday on speculation that the Biden administration was moving towards releasing at least another 10 million to 15 million barrels of oil from the nation’s emergency stockpile.

American Petroleum Institute said on Tuesday that U.S. crude oil stockpiles fell by about 1.3M barrels for the week ending Oct. 14.

Russian President Vladimir Putin introduced martial law in Donetsk, Luhansk, Kherson and Zaporizhzhia, the four regions of Ukraine annexed by Russia in September

Bloomberg reported on Thursday that Chinese officials are contemplating whether to lower the mandated quarantine time for visitors

Indonesia central bank hiked interest rates by 50 bps to 4.75%, as expected

Liz Truss announced on Thursday that she will step down from her position as British PM after only six weeks due to her economic plan that angered many members of her own party and rattled financial markets.

Federal Reserve Bank of Philadelphia President Patrick Harker predicted that policymakers will increase interest rates to “far beyond” 4% this year and keep them there to fight inflation, while they would leave the door open to taking more action if necessary.

The Bank of Japan took more action on Friday to reduce rising yields by offering to purchase bonds with maturities of 10 to 25 years for ¥100B ($664.98M).

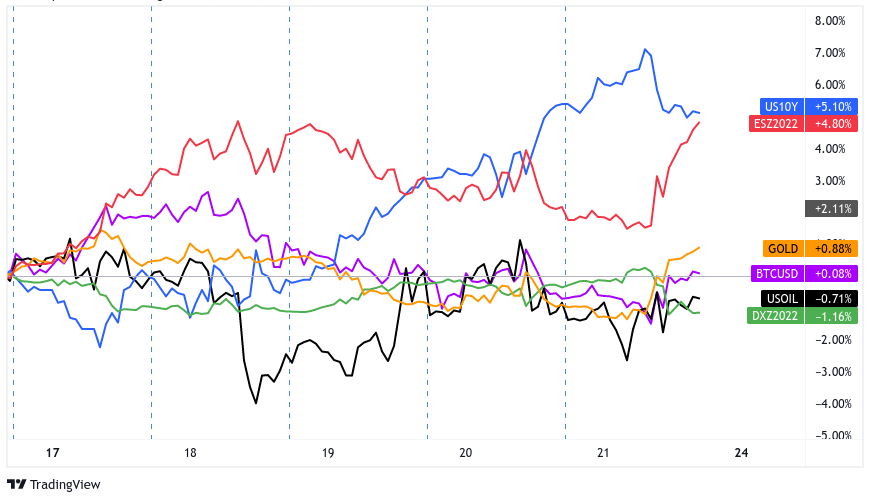

Intermarket Weekly Recap

Dollar, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay 1-Hour

On the intermarket chart above, we can see a clear break from the usual recent themes of rising bond yields, strong U.S. dollar against weakness in pretty much everything else. It’s was likely due to a heavy news and data cycle this week splitting trader focus.

First, we saw fresh developments from the U.K. on Monday as New Chancelor of the Exchequer Jeremy Hunt ripped into the prior stimulative measures that rocked the U.K. bond market over the past month. Arguably, this brought down some level of fear in the markets, evidenced by a dip in bond yields/USD and rise in equities and crypto.

On Tuesday, traders turned their focus to Japanese officials as they tried to jawbone yen weakness, and oil prices saw some action, dipping on speculation of more oil to be released from the US emergency oil reserve.

But on Wednesday, bond yields and the Dollar came back on to the main staged, arguably ripping higher on more hotter-than-expected inflation reads, this week from New Zealand, the U.K. and Canada. Oil also shot up higher during the U.S. session, possibly a reaction to a surprise draw in U.S. crude stockpiles, according to private survey data.

On Thursday, the big news of the session was the resignation of recently appointed British Prime Minister Lizz Truss, but the big market driver seems to have been the reaction to comments from Fed member Harker. He gave hawkish comments during the U.S. session on how interest rates may go far beyond 4.00% this year.

On Friday, it looks like traders went risk-on ahead of the weekend, possibly a reaction to intervention by the Bank of Japan in Japan’s bond markets, but more likely a combination of an end-of-week profit taking and a report from the Wall Street Journal that some Fed officials may be concerned about the risks of over tightening monetary policy.

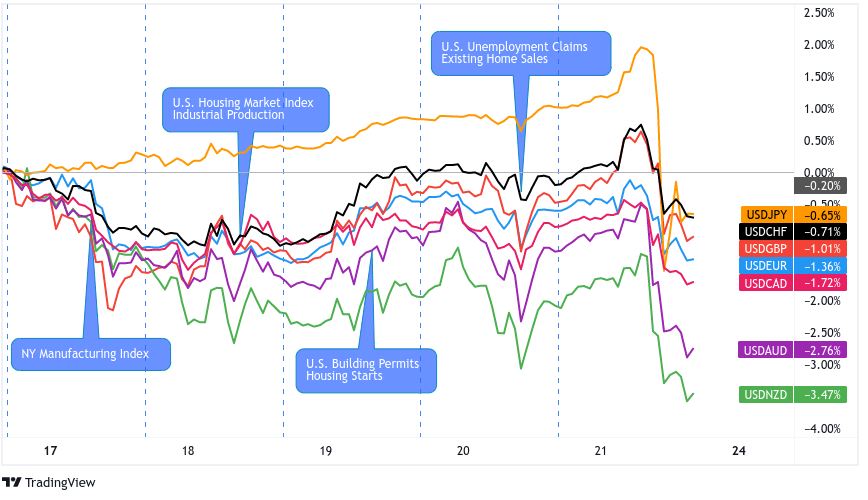

USD Pairs

Overlay of USD Pairs: 1-Hour Forex Chart

New York Manufacturing Index fell to -9.1 in October vs. -1.5 in September; inventory and employment indicators slightly grew, as well as input prices; companies have little expectations of improvement in business conditions over the next six months.

The National Association of Home Builders (NAHB)/Wells Fargo Housing Market Index (HMI) for October: -8 points to 38; fast rising interest rates blamed for the fall in confidence.

U.S. Housing Starts: -8.1% y/y in September to a seasonally adjusted annual rate of 1.439M units.

Neel Kashkari, president of the Minneapolis Federal Reserve, said that the Federal Reserve cannot end its campaign of monetary policy tightening until its benchmark interest rate reaches 4.5% to 4.75% if “underlying” inflation is still accelerating.

U.S. mortgage rates hit a new high as the 30-year fixed mortgage jumped another 13 basis points to 6.94% in the week ended Oct. 14, the highest levels since 2002

Fed’s Beige Book says U.S. economy expanded modestly, notes some easing of price growth pressure

FOMC’s Bullard expects Fed to end its “front-loading” of aggressive rate hikes by early next year

Philly Fed Manufacturing Index: -8.7 vs. -5.0 forecast and -9.9 previous

U.S. weekly initial jobless claims for week ending Oct. 15: 214K vs. a lower revised 230K previous

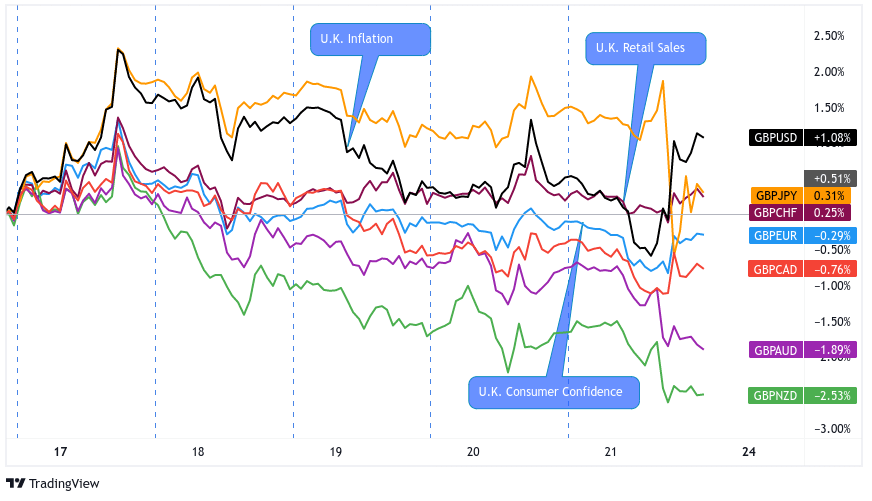

GBP Pairs

Overlay of GBP Pairs: 1-Hour Forex Chart

The Truss administration’s tax and spending policies during its brief six weeks in office would likely result in higher interest rates for UK borrowers, the governor of the Bank of England has warned this past weekend

On Monday, Britain’s new finance minister, Jeremy Hunt, got rid of Prime Minister Liz Truss’s economic plan and scaled back her huge energy support plan.

On Tuesday, the Bank of England said the report in the Financial Times about a new delay to the start of its government bonds sales was inaccurate

U.K. headline CPI popped higher in September from 9.9% y/y to 10.1% y/y in August and the 10.0% y/y forecast; core CPI read at 6.5% y/y vs. 6.3% y/y previous

On Wednesday, British Prime Minister Liz Truss tried to regain control over her divided party. Conservative enforcers told lawmakers that they had to support her fracking policy in a vote that was seen as a test of confidence in the government.

The annual growth in the average price of a home in the United Kingdom was 13.6% up to August 2022, down from 16.0% in July 2022.

U.K. GfK consumer confidence index improved from -49 to -47 vs. -52 forecast

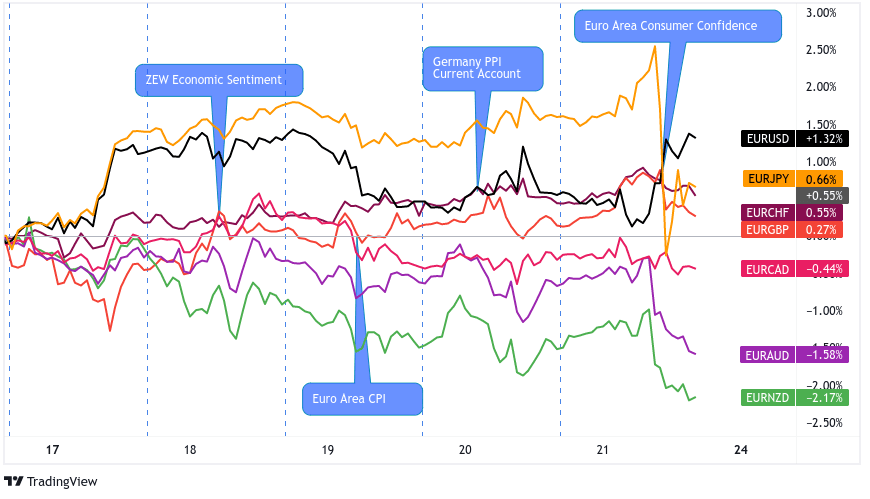

EUR Pairs

Overlay of EUR Pairs: 1-Hour Forex Chart

German investor sentiment for October: -59.2 vs. -61.9 previous; current conditions index dropped by 11.7 points to -72.2

Eurozone final September CPI came in at +9.9% y/y vs. +10.0% y/y preliminary read; core CPI at 4.8% y/y vs. 4.3% previous

Germany producer prices for industrial products for September: 45.8% y/y and 2.3% m/m

Euro area current account recorded a €26B deficit in August 2022 vs. a €20B deficit in September

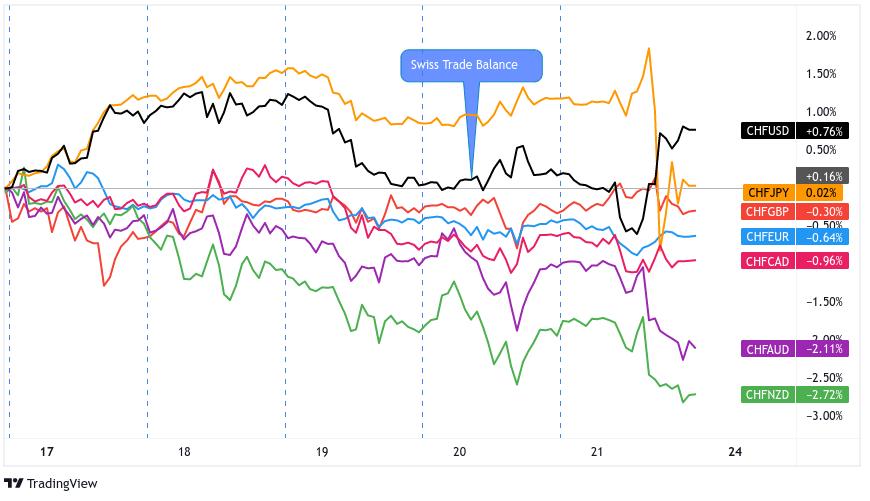

CHF Pairs

Overlay of CHF Pairs: 1-Hour Forex Chart

From a slightly revised CHF 2.3B in August, the Swiss trade surplus climbed to CHF 2.8B in September 2022. The increase in exports to CHF 22.8B from a month earlier and the increase in imports to CHF 19.9B made it the highest trade surplus since April.

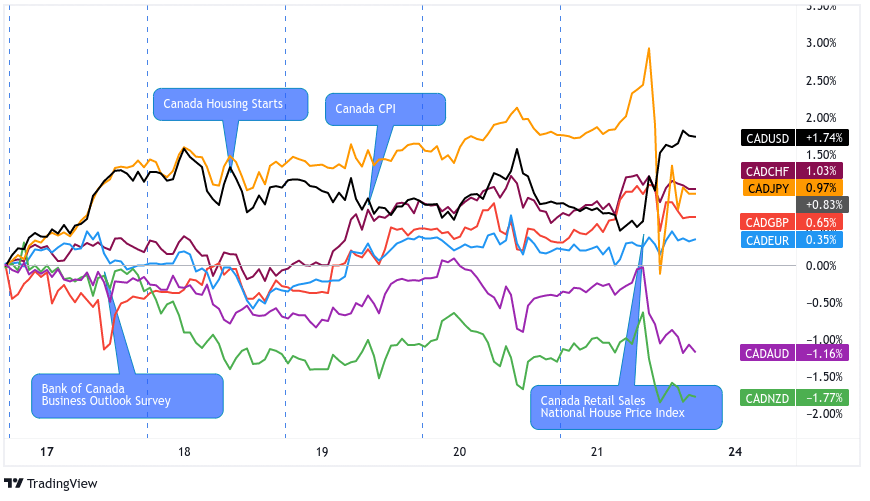

CAD Pairs

Overlay of CAD Pairs: 1-Hour Forex Chart

Bank of Canada Business Outlook Survey Indicator fell to 1.69 in Q3 2022 vs. 4.87 in Q2 2022 as firms sees little signs of inflation softening

Canadian inflation data for September was stronger-than-expected at 6.9% y/y vs. 6.7% forecast; on a monthly basis, prices rose by +0.1% m/m vs. a -0.1% forecast

Canada Retail Sales dropped -0.5% m/m in September vs. a +0.7% rise in August.

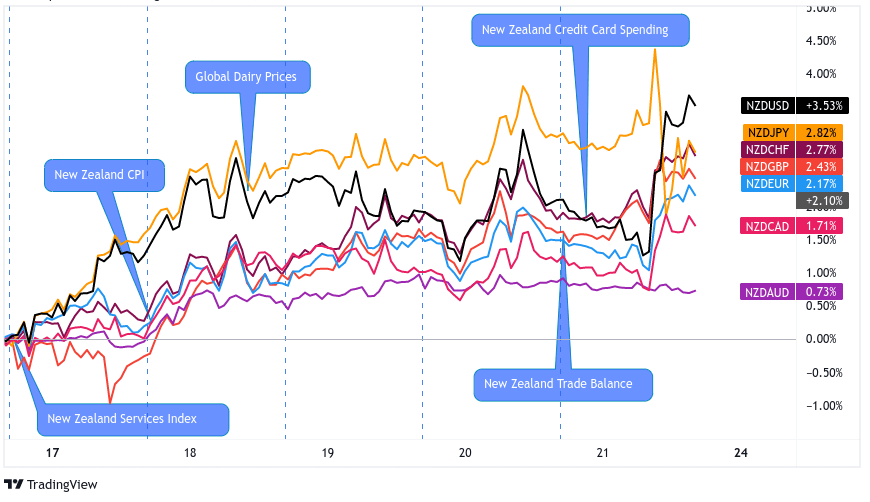

NZD Pairs

Overlay of NZD Pairs: 1-Hour Forex Chart

New Zealand business services index down from 58.6 to 55.8

New Zealand inflation stays near 32-year high at 7.2%, fueling RBNZ bets

Global dairy price index falls by -4.6% from the last autcion to an average price of $3.723

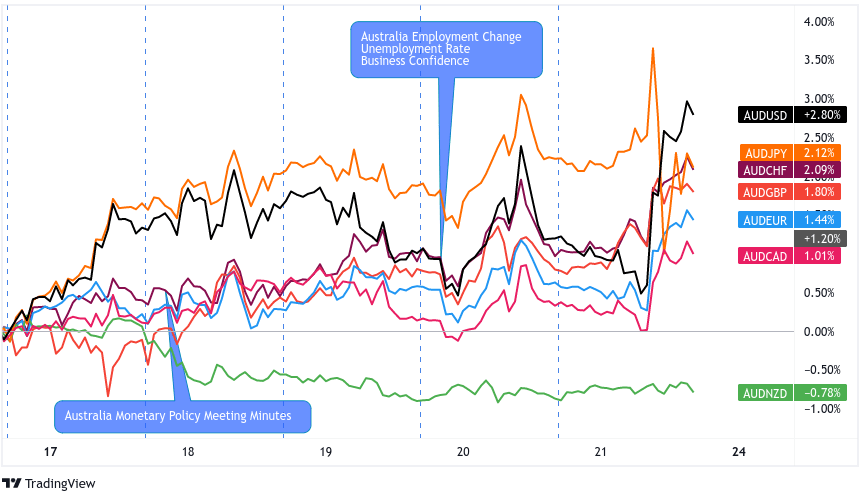

AUD Pairs

Overlay of AUD Pairs: 1-Hour Forex Chart

RBA’s meeting minutes: a smaller increase was warranted given the pace and lagging effect of the “substantial” rate hikes; further interest rate hikes are “likely” over the period ahead

Westpac’s Australia leading index read for September: -0.1% m/m vs -0.1% m/m prior

Australia jobless rate unchanged at 3.5% in September

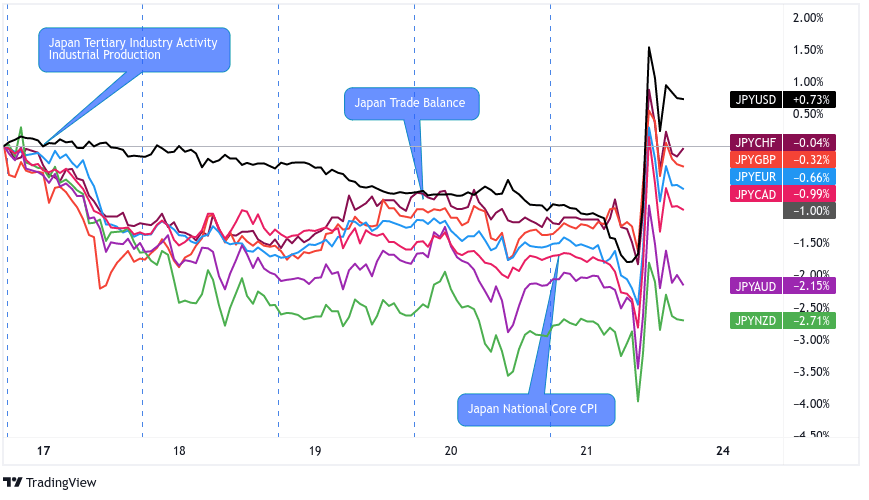

JPY Pairs

Overlay of Inverted JPY Pairs: 1-Hour Forex Chart

Haruhiko Kuroda, governor of the Bank of Japan, stated that monetary easing will continue, signifying no interest in a change in policy even as the yen continued its recent steep decline and hit a new 32-year low.

Japanese authorities continued to give verbal warnings to the market on Monday of willingness to firmly respond to rapid yen losses.

Japanese tertiary industry index rebounded by 0.7% after earlier 0.5% dip

Japanese industrial production upgraded from 2.7% to 3.4% growth

BOJ Kuroda aid that consumer inflation will likely accelerate towards year-end before pulling back below 2% in the next fiscal year

Japan trade deficit was 2.09 trillion yen ($14B) in September, the second month in a row over 2T yen; exports gained 28.9% y/y while imports rose in value 45.9% y/y

The benchmark rate in Japan surged beyond the policy ceiling of 0.25%, prompting the BOJ to announce an unexpected round of buying ¥250B ($1.7B) of bonds ranging from 5-year to longer-dated debt.

Japanese national core CPI up from 2.8% y/y to 3.0% y/y as expected