Thanks to a heavy economic calendar, it was a very busy week for forex traders who had to balance global business surveys, economic data updates and lots of central bank speak. It’s no surprise that we saw choppiness and a less tight correlation from the usual intermarket price patterns.

The New Zealand dollar ended up being this week’s clear winner in FX, thanks to much-better-than-expected data from China helping Kiwi take the mid-week lead and overshadowing net negative updates from New Zealand.

Notable News & Economic Updates:

U.K. and the European Union leaders made a new deal that would tackle trade and political disruption in Northern Ireland after Brexit

U.S. CB consumer confidence unexpectedly fell from 106.0 to 102.9 in January on sticky inflation and high interest rate expectations

Several ECB officials commented this week on how they’re winning the inflation fight but the ECB will stay aggressive with rate hikes until it is certain price growth will return to 2%.

China’s official manufacturing PMI jumped from 50.1 to 52.6 in February, the fastest expansionary pace since April 2012, while the services PMI improved from 56.3 to 54.4 after Beijing withdrew its zero-COVID policies

China’s private sector Caixin manufacturing PMI rose from 49.2 to 51.6 in February and marked its first increase since July 2022 as output and new orders saw notable increases after China lifted its zero-COVID policies

Eurozone Manufacturing PMI for February: 48.5 vs. 48.8 in January; Services PMI rose to 52.7 in February (an 8-month high)

U.K. Manufacturing PMI rose to 49.3 in February (47.0 in January); signs of resilience and stability seen across many sub-sectors; optimism for 2023 is seen at the highest its been in 12 months

U.S. Manufacturing PMI for February: 47.3 vs. 46.9 in January; new orders continue to fall; “Input prices faced by manufacturing firms increased at a sharp pace”

Bitcoin and other major cryptos dropped sharply on Friday, likely a reaction to negative headlines for Silvergate Bank, a crypto-friendly financial institution.

Intermarket Weekly Recap

Dollar, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay 1-Hour by TradingView

Markets started the week by bargain-hunting after the previous week’s selloff led European and U.S. equities to their worst week so far this year. End-of-month profit-taking may have also added to the pro-risk, anti-USD sentiment that played out during the Monday U.S. session.

Risk-taking carried over to Tuesday trading with the safe-haven yen taking an extra knock from incoming BOJ Deputy Gov. Shinichi Uchida and future BOJ Gov. Kazuo Ueda supporting the current “Abenomics” before the Japanese Parliament.

Safe-haven assets got their mojo back during Tuesday’s U.S. trading session after a U.S. PMI report showed the manufacturing sector contracted for a fourth consecutive month in February. Chicago’s PMI, Richmond’s Fed Manufacturing survey, and the CB consumer confidence data also reflected weaker business sentiment due to higher interest rate expectations.

The disappointing reports got mixed in with end-of-month profit-taking, likely fueling the turn lower in equities and risk assets while U.S. Treasury yields, gold, and the U.S. dollar jumped higher.

Just as Asian session traders were ready to extend the pessimism, China’s official manufacturing and services PMIs as well as Caixin’s manufacturing PMI came out Wednesday morning. The reports not only noted the fastest factory activity expansion in more than a decade, but it also showed sharp increases in China’s factory activity, new orders, and employment after the government lifted its zero-COVID policies.

Not surprisingly, commodity-related currencies like AUD and NZD jumped at the news, but bullish sentiment Aussie seems to have been limited by Australian updates that gave room for the RBA to consider less aggressive monetary policy tightening ahead (e.g., Australia’s inflation came in below expectations and previous at +7.4% y/y in January, Australia’s GDP disappointed at 0.5% q/q in Q4 vs. +0.8% q/q estimate).

European and U.S. equities didn’t get much chance to celebrate China’s recovery, however, thanks to Germany’s inflation data mirroring upside surprises in Spain and France’s CPIs, supporting higher-for-longer interest rate speculations.

Expectations of higher interest rates from major central banks carried over to Thursday trading when the benchmark 10-year U.S. Treasury yields hit new intraweek high above 4%–the highest since November! It also didn’t help that U.S. initial jobless claims and labor productivity data reflected a tight enough labor market to support further rate hikes.

Relief came when FOMC voting member Raphael Bostic spilled that the Fed could pause its rate hikes as soon as mid or late summer this year, correlating with a turn in U.S. Treasury yields while other risk assets turned higher.

Friday’s price action looked like a continuation of Thursday’s, actually even accelerating in its risk-on lean as bond yields continued to fall. This arguably was catalyzed by a big dip in the Eurozone producer prices index and another round of net contractionary global business sentiment data, toning down the recent strengthening of the “higher-for-longer interest rates” narrative that is currently dominating broad market sentiment.

Despite that action, it appears that cryptocurrencies were the place to be for short-term traders to find volatility as BTC/USD dropped from the $23,400 area to below $22,000 in less than an hour while other major crypto pairs showed similar downswings.

This is broadly attributed to fresh headlines on Silvergate Bank – a crypto-friendly financial institution – which failed to submit a SEC report and had “operational issues.” Crypto heavyweights like Coinbase and Galaxy Digital have already dropped Silvergate as a banking partner.

Most Notable FX Moves

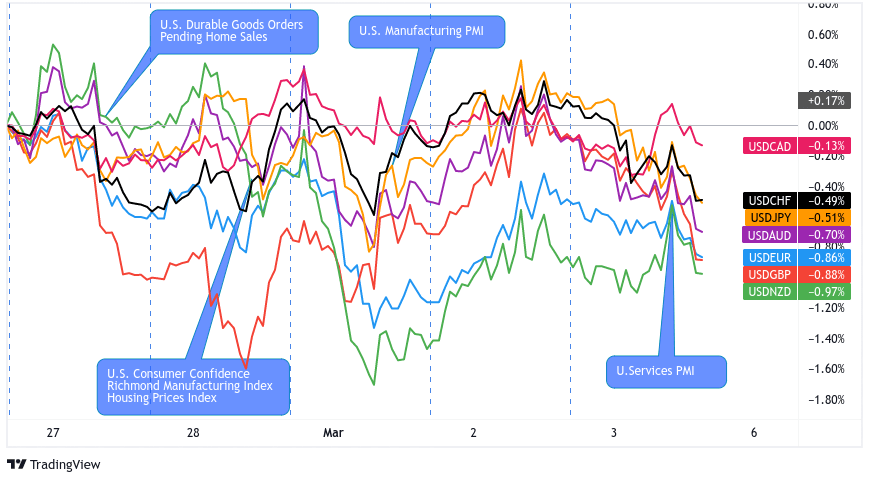

USD Pairs

Overlay of USD Pairs: 1-Hour Forex Chart

More Fed speak:

- Philip Jefferson says services inflation remains “stubbornly high,” but slowing wage growth may helps soften high inflation conditions

- Kashkari and Bostic suggested on Wednesday that aggressive interest rate hikes and maintaining rates high for a while may be needed to reduce inflation

U.S. Pending Home Sales Index jumped by +8.1% m/m in January to 82.5 vs. a +1.1% m/m increase in December

U.S. Durable Goods Orders dropped in by -4.5% in January vs. a 5.1% m/m rise in December; core durable goods orders rose by +0.7% m/m vs. -0.2% m/m previous

Chicago PMI fell by 0.7 points in February to 43.6; employment sub-index fell 4.7 into contractive territory

Richmond Manufacturing Index fell to -16 in February from -11 in January

US CB consumer confidence unexpectedly fell from 106.0 to 102.9 in January on sticky inflation and high interest rate expectations

U.S. Manufacturing PMI for February: 47.3 vs. 46.9 in January; new orders continue to fall; “Input prices faced by manufacturing firms increased at a sharp pace”

ISM U.S. Manufacturing PMI for February: 47.7 vs. 47.4 in January; “Employment Index returned to contraction after two months of expansion”; Prices Index jumped to 51.3 vs. 44.5 previous

U.S. initial jobless claims, a proxy for layoffs, dipped from 192K to 190K last week and supported a strong labor market.

GBP Pairs

Overlay of GBP Pairs: 1-Hour Forex Chart

The British pound was participating in the risk rally when BOE Governor Bailey signaled that it would be wrong to assume further rate hikes from the central bank. GBP dropped from intraweek highs to intraweek lows before steadying just above its weekly open prices.

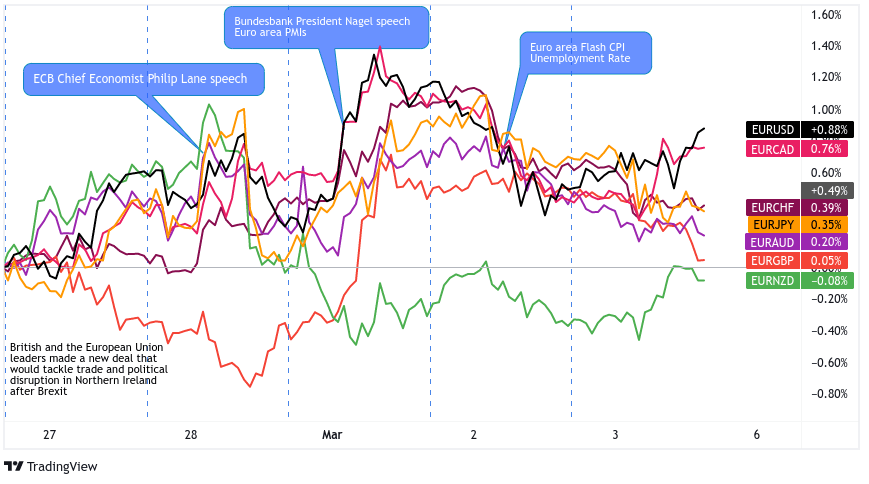

British and the European Union leaders made a new deal that would tackle trade and political disruption in Northern Ireland after Brexit

Jon Cunliffe, Bank of England Deputy Governor, said a new digital pound may protect consumers in the event of a banking system failure, supporting a proposal to make cash accessible online.

BOE Gov. Bailey cautions against suggesting that the central bank is done with rate hikes or needs to do more

BRC: UK’s shop prices 8.4% higher from a year ago in February, faster than January’s 8% increase and three-month average of +7.8%

U.K. Manufacturing PMI rose to 49.3 in February (47.0 in January); signs of resilience and stability seen across many sub-sectors; optimism for 2023 is seen at the highest its been in 12 months

EUR Pairs

Overlay of EUR Pairs: 1-Hour Forex Chart

ECB Chief Economist Philip Lane said on Tuesday that they’re winning the inflation fight but the ECB will continue rate hikes until it is certain price growth will return to 2%.

Eurozone Manufacturing PMI for February: 48.5 vs. 48.8 in January; new orders fell for a 10th consecutive month; input price pressures easing; “”Factory employment rose moderately and at the quickest rate in four months.”

Bundesbank President Joachim Nagel said on Wednesday that he supports faster quantitative tightening (QT) and larger interest rate hikes to tame inflation.

Euro area annual inflation down to 8.5% y/y in February (8.3% y/y forecast) vs. 8.6% y/y in January; core CPI rose by 5.6% y/y vs. 5.3% forecast/previous

Christine Lagarde, president of the European Central Bank, said on Thursday that interest rates may need to continue higher after the anticipated 50 bps adjustment in two weeks.

ECB’s February minutes showed agreement over further tightening, but also talks of policy rates “coming closer to a level where caution was needed to ensure that monetary policy was not tightened excessively.”

Eurozone Services PMI rose to 52.7 in February (an 8-month high) vs. 50.8 in January; cost pressures ebbed in manufacturing sector but rose substantially in services sector

On Friday, Eurostat reported that factory gate prices in the 20 eurozone countries fell -2.8% m/m in January for a 15.0% y/y increase, down from the 24.5% y/y read in December.

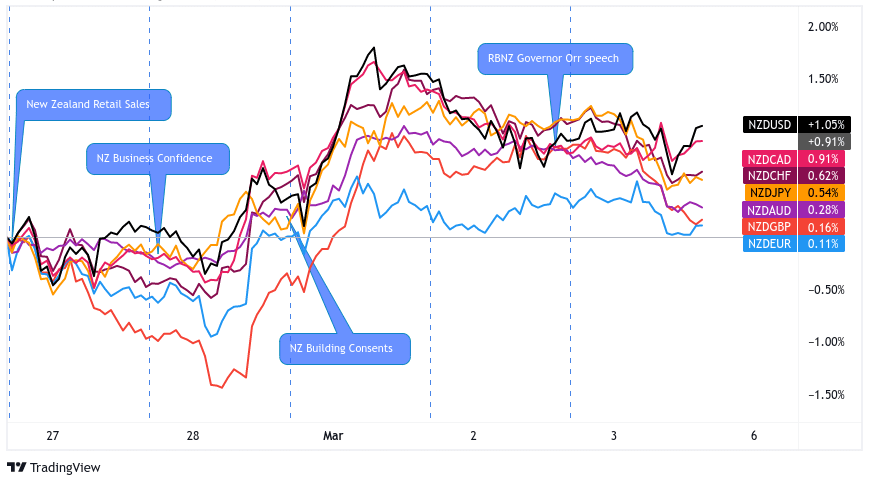

NZD Pairs

Overlay of NZD Pairs: 1-Hour Forex Chart

A jump in risk-taking started NZD’s intraweek uptrend and made it a good candidate for bulls who were looking to price in China’s better-than-expected business activity reports.

Retail sales sank by 0.6% in Q4 after a surprise 0.6% increase in Q3 2022

ANZ business confidence index improved from -52.0 to -43.3 to reflect reduced pessimism

Building permits decline by another 1.5% m/m after a 7.2% drop in December

New Zealand overseas trade index rebounded by 1.8% q/q in Q4 after previous 3.9% slide instead of decreasing by the estimated 1.7%, exports up 20% from previous period

RBNZ Gov. Orr: We need to bring inflation back to target range “over a reasonable horizon” to not “unnecessarily crash the economy and turn temporary, slower growth into permanent unemployment.”

Consumer confidence eased 3 points to 79.8 in February amidst higher living costs and interest rates

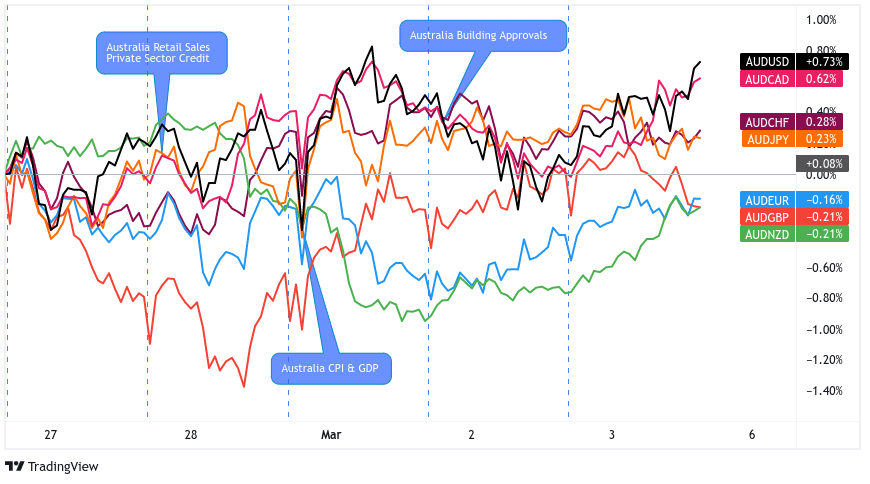

AUD Pairs

Overlay of AUD Pairs: 1-Hour Forex Chart

Stronger than expected Australian data (private sector credit, retail sales) keep pressure on RBA to keep hiking rates

Australia’s inflation up by 7.4% y/y in January, slower than December’s 8.4% growth and the expected 8.1% increase but still way above RBA’s 2%-3% target range

Australia’s GDP disappoints at 0.5% q/q in Q4, less than the estimated 0.8% uptick and Q3’s upwardly revised 0.7% growth, as cost pressures and high interest rates drag household consumption to its slowest growth in five quarters

S&P Global Australia Manufacturing Purchasing Manager’s Index came in at 50.5 in February vs. 50.0 in January; “Both input and output price indexes have stopped falling in any meaningful way.”; “Employment levels overall rose at the fastest rate since last September”

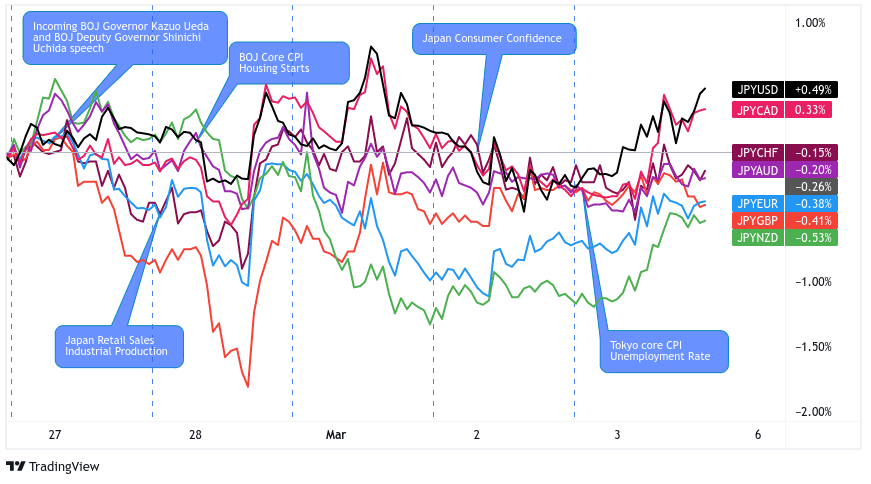

JPY Pairs

Overlay of Inverted JPY Pairs: 1-Hour Forex Chart

BOJ’s Wakatabe warns secular stagnation risk has yet to pass

Japanese preliminary industrial production sank 4.6% m/m vs. estimated 2.9% decline in Jan, largest fall in eight months

Japan’s retail sales popped 6.3% higher y/y vs. projected 4.2% gain and previous 3.8% reading

Incoming BOJ Governor Kazuo Ueda and BOJ Deputy Governor Shinichi Uchida show support for “Abenomics,” says central banks must remain “on guard” against low inflation as cost-push factors do not last long.

Japan’s au Jibun Bank manufacturing PMI adjusted higher from 47.4 to 47.7 in February but still lower than January’s 48.9 reading

Japanese consumer confidence index ticked higher from 31.0 to 31.1 in February, short of estimated improvement to 32.1

Tokyo’s core inflation slows from 42-year high of 4.3% y/y to 3.3% in February, closer to BOJ’s 2% target

Japan’s unemployment rate unexpectedly dipped from 2.5% to 2.4%, the lowest reading since February 2020