A bit of calm returned to the financial markets in the past trading sessions, but we still saw pretty big moves among a few major currencies and asset classes.

Bitcoin staged quite the rebound as it closed roughly 5% higher for the day while Treasury yields chalked up pretty decent gains as well.

Here’s a quick rundown of the headlines and economic updates that affected the markets:

Headlines:

- Australia’s ANZ job advertisements fell 3.0% month-on-month in July vs. previous 2.7% slump (downgraded from initially reported 2.4% decline)

- RBA kept interest rates unchanged at 4.35% in a “hawkish hold” decision, as policymakers mentioned that “inflation is still too high and is coming down slower than expected”

- Swiss unemployment rate ticked higher from 2.4% to 2.5% in July as expected

- German factory orders rebounded by 3.9% month-on-month in June vs. estimated 0.4% uptick and previous 1.7% drop

- Swiss retail sales tumbled by 2.2% year-on-year in June (+0.5% expected, previous reading downgraded from +0.4% to -0.2%)

- U.K. construction PMI in July: 55.3 (52.5 expected, 52.2 previous)

- New Zealand GDT auction yielded 0.5% gain in dairy prices (0.4% previous)

- New Zealand employment change in Q2 2024: +0.4% q/q (-0.2% expected, previous reading downgraded from -0.2% to -0.3%)

- New Zealand jobless rate in Q2 2024: 4.6% (4.7% expected, previous reading revised from 4.3% to 4.4%)

- New Zealand labor cost index in Q2 2024: 0.9% q/q (0.8% expected, 0.8% previous)

Broad Market Price Action:

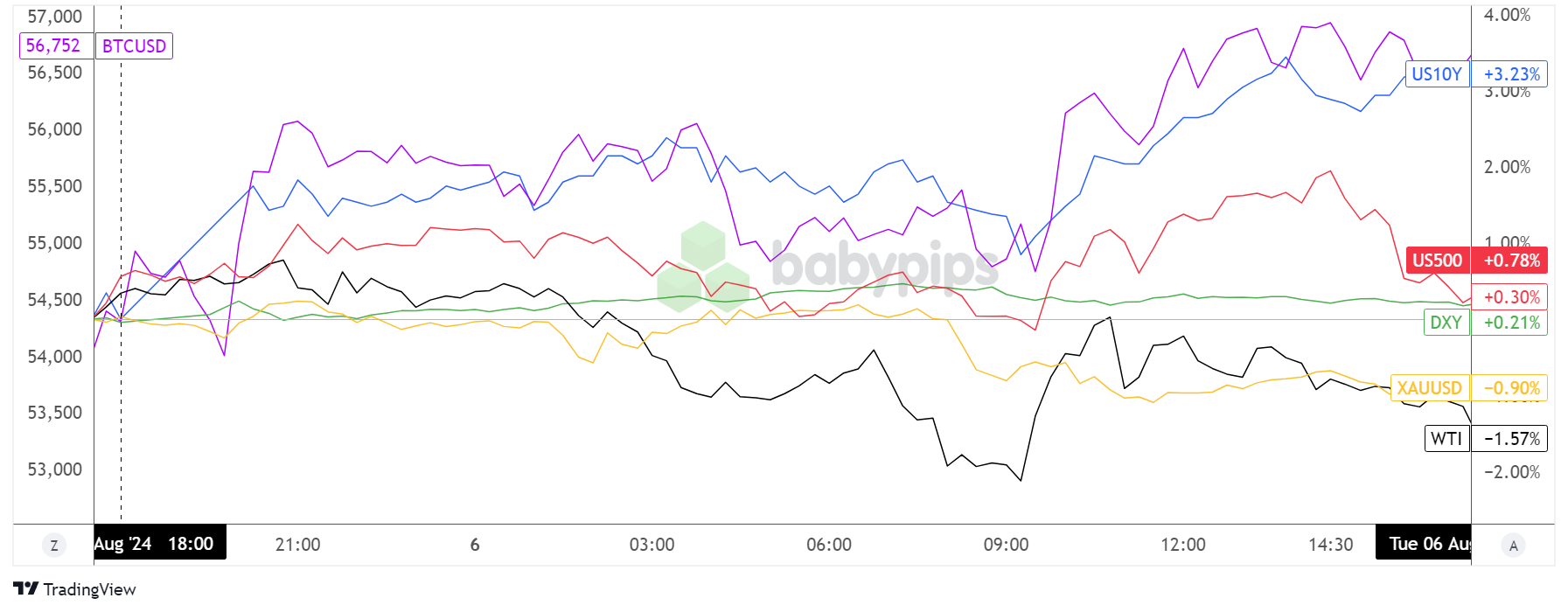

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

The market panic from Monday seemed to subside during Tuesday’s Asian trading session, as commodities like gold and crude oil traded sideways while Treasury yields edged higher.

Bitcoin was off to a running start, as it bounced off the $54,000 zone early on and traded right around $56,000 before tumbling back to $55,000 at the start of London market hours. Another rally ensued as U.S. session traders got to their desks, taking BTC/USD past its intraday highs to close nearly 3% higher for the day.

Meanwhile, crude oil also managed to bounce right around the New York session, thanks to a report by the U.S. Energy Information Administration indicating global inventory drop of about 400,000 barrels per day in the first half of the year, adding to ongoing supply concerns from geopolitical risks. Still, this was not enough to put the commodity back in positive territory since risk-off flows lingered.

In the U.S. equity market, indices capped off their three-day slump, as the S&P and Nasdaq both closed in the green, even after paring majority of its strong gains earlier in the session.

FX Market Behavior: U.S. Dollar vs. Majors:

Overlay of USD vs. Major Currencies Chart by TradingView

Dollar price action was all over the place on Tuesday, as USD/JPY had its own usual thing going – this time related to the unwinding of the carry trade – while some major currencies had individual catalysts to respond to.

The Aussie chalked up some gains following a somewhat “hawkish hold” announcement from the RBA, with the central bank keeping rates unchanged as expected but also warning that inflation remains hotter than expected. AUD/USD wound up returning its post-RBA gains ahead of the U.S. session, before it joined the rest of the commodity currencies in taking advantage of risk appetite.

On the flip side, sterling wound up as the weakest of the bunch, despite a stronger than expected U.K. construction PMI release, while its European peers also closed in negative territory.

Upcoming Potential Catalysts on the Economic Calendar:

- Chinese trade balance coming up

- German industrial production and trade balance at 6:00 am GMT

- SNB foreign currency reserves report at 7:00 am GMT

- Canadian Ivey PMI at 2:00 pm GMT

- EIA crude oil inventories at 2:30 pm GMT

- BOC Summary of Deliberations at 5:30 pm GMT

- BOJ Summary of Opinions at 11:50 pm GMT

There’s not much on the docket in terms of the usual set of top-tier catalysts today, although the Chinese trade balance would be worth a look when it comes to gauging overall market sentiment.

Other mid-tier reports to keep an eye out for include Canada’s Ivey PMI, which serves as a leading indicator for employment and inflation, as well as the BOC Summary of Deliberations a.k.a. central bank meeting minutes that could have clues on future policy moves.