The major assets were all over the place on Wednesday as traders priced in their Fed rate cut biases, U.S. political updates, and top-tier reports from the U.K. and the U.S.

In FX, a hotter-than-expected U.S. core CPI helped the dollar recover some of its intraday losses but also limited its gains against risk-related currencies.

Which headlines dominated the markets yesterday? Let’s discuss the top ones:

Headlines:

- RBA Assistant Gov. Sarah Hunter said the labor market is “still tight relative to full employment” and historical standards

- The U.S. Presidential debates resulted in a reversal of “Trump trades” with the U.S. dollar, bond yields, and bitcoin trading lower

- BOJ member Junko Nakagawa said the Bank will continue to raise its rates “if our economic and price forecasts are met” and warned about wage growth overshooting expectations and inflation exceeding their target

- U.K. GDP showed no growth (0.0%) in July 2024, following flat growth in June 2024

- U.K. industrial production weakened by 0.8% m/m in July (0.3% expected, 0.8% previous); Manufacturing production fell by 1.0% after a 1.1% increase in June

- NIESR U.K. GDP tracker sees a 0.2% quarterly growth in Q3 2024 after a 0.5% uptick in Q2

- Hotter U.S. Core Inflation Reduced The Odds Of A 50bps Fed Rate Cut

- EIA: U.S. crude oil inventories increased by 0.8M barrels vs. 6.9M-barrel draw expected and expected 0.9M-barrel increase expected in the week ending September 6

Broad Market Price Action:

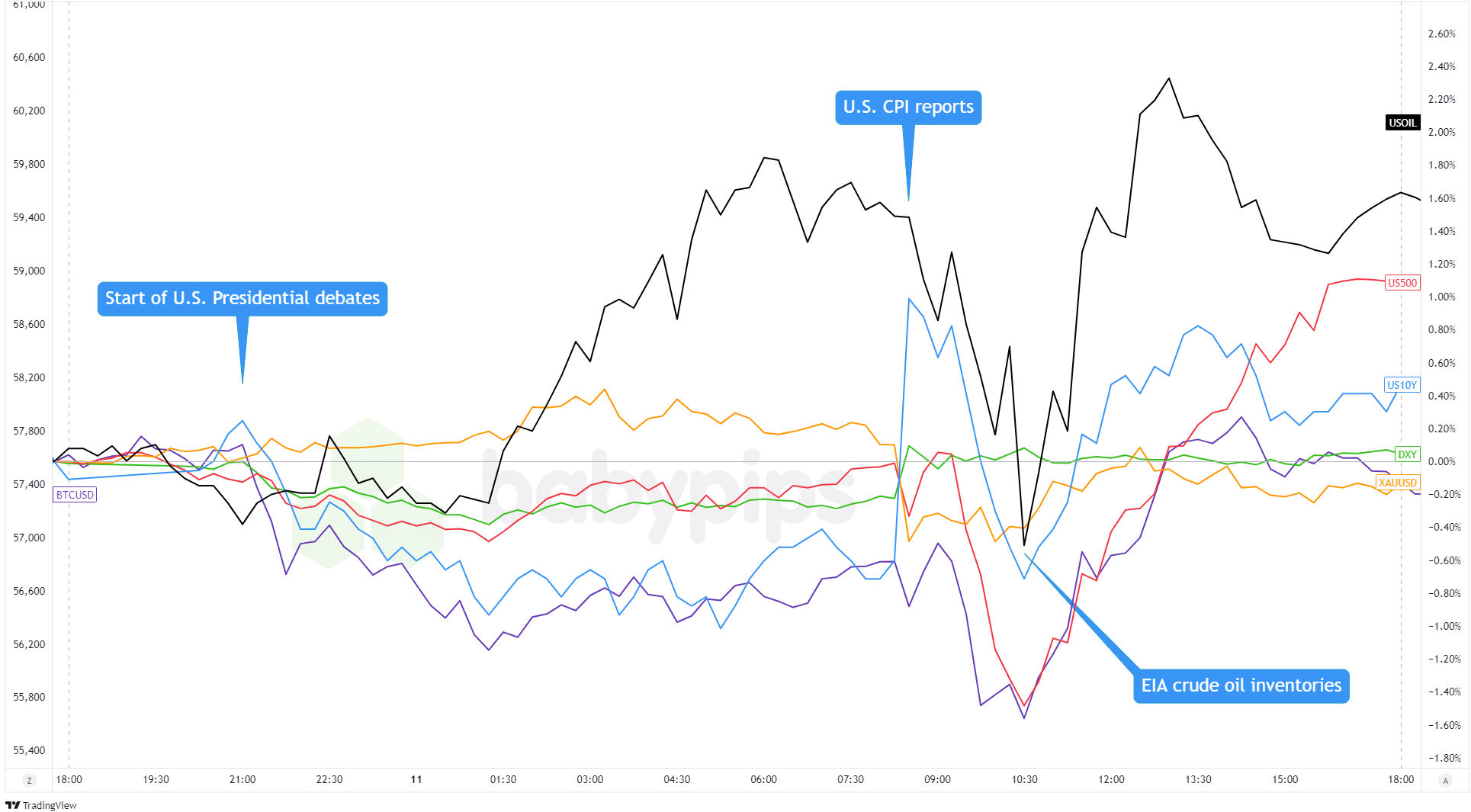

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Markets were pretty quiet early the day, with major assets trading in tight ranges, but that changed after the U.S. Presidential debate. The odds of a Harris win increased, and that weighed on U.S. 10-year yields, stock futures, and the dollar as traders saw less chance of higher tariffs or increased government spending under a Trump administration.

Things took a turn during the European session, with risk assets bouncing back—likely driven by some profit-taking after earlier declines in Asia. WTI crude climbed from $66.00 to $67.50, gold eased off record highs, and bitcoin pulled up from its intraday lows.

In the U.S., all eyes were on the CPI report. While annual inflation dropped to multi-month lows, the core reading dialed back expectations for a 50-basis-point rate cut from the Fed.

The dollar and 10-year yields initially spiked after the report, but risk appetite quickly returned. Gold recovered from $2,502 to close near $2,512, bitcoin revisited its weekly highs, and U.S. stock indices finished the day in the green.

FX Market Behavior: U.S. Dollar vs. Majors:

Overlay of USD vs. Major Currencies Chart by TradingView

The dollar started off weak as the U.S. Presidential debate lowered the odds of a Trump win, reducing expectations for more government spending and higher tariffs.

USD/JPY faced extra downward pressure after Bank of Japan (BOJ) official Junko Nakagawa backed further rate hikes. But the Greenback found some relief during the European session, likely from traders reversing earlier positions ahead of the U.S. CPI reports.

U.S. inflation showed weaker annual numbers, but the bump in core inflation cooled down some expectations of a 50-basis-point rate cut.

The dollar briefly rallied after the report, but a risk-on mood led to mixed results. It extended gains against safe havens like the Swiss franc and Japanese yen but lost ground to risk currencies like the pound, Aussie, kiwi, and Canadian dollar.

Upcoming Potential Catalysts on the Economic Calendar:

- Germany wholesale prices at 6:00 am GMT

- Italy quarterly unemployment rate at 8:00 am GMT

- ECB policy statement at 12:15 pm GMT, presser at 12:45 pm GMT

- Canada building permits at 12:30 pm GMT

- U.S. PPI reports at 12:30 pm GMT

- SNB Chairman Jordan to give a speech at 2:25 pm GMT

- U.S. Fed budget balance at 6:00 pm GMT

- BusinessNZ manufacturing index at 10:30 pm GMT

The markets are in for another big day as the European Central Bank (ECB) drops its September policies. Word around is that President Lagarde and her team may cut the Euro Area interest rates, so don’t even think of missing the announcement!

In the U.S., producer price updates may support or weaken the themes set by the consumer inflation readings. Hotter-than-expected prints would point to a 25bps Fed rate cut next week and probably push the dollar higher against the safe havens but lower against the risk-related currencies.

Don’t forget to check out our brand new Forex Correlation Calculator!