Central bankers were under the spotlight yesterday, and a lack of top-tier data releases made it easier to reprice monetary policy biases across the major assets.

Which headlines influenced the major assets’ price action?

We have the deets!

Headlines:

- China announced a slew of stimulus measures that include cutting its reserve ratio requirement by 50bps and its 7-day reverse repo rate from 1.7% to 1.5%

- As expected, RBA kept its rates at 4.35% and repeated that inflation “remains too high”

- Major central bank members shared their two cents:

- ECB President Lagarde said high inflation is “not quite” beaten, said she talks but doesn’t coordinate with Powell

- BOJ Gov. Ueda believes inflation is “likely” to hit 2%, and confirmed his willingness to raise rates if their economic outlook materializes

- RBA Gov. Bullock shared that the team didn’t discuss a rate hike or the size of any potential rate cut. She added that “rates will remain on hold for the time being”

- BOE Gov. Bailey said “inflation has come a long way” and that easing would continue “gradually”

- ECB’s Madis Muller is not ruling out an October rate cut, but said it will be “easier” to decide with more data in December

- FOMC voting member Michelle Bowman – lone dissenter of the 50bps rate cut – thought the Fed should’ve moved at a more “measured pace”

- Bundesbank President Joachim Nagel believes some factors dragging the German economy are temporary, and that it will pick up momentum again even as it’s expected to remain weak this year

- BOC Gov. Macklem repeated that it’s “reasonable” to expect further rate cuts, and shared he’s closely watching consumer spending and business hiring and investment

- Germany IfO business climate worsened from 86.6 to 85.4 (86.1 expected) in September as the economy sees increased pressure

- U.S. S&P CoreLogic Case-Shiller house price index eased from 6.5% y/y to 5.9% y/y as expected in July

- U.S. FHFA house price index for July: 0.1% m/m (0.2% expected, June reading revised higher from -0.1% to 0.0%)

- U.S. CB consumer confidence fell from 105.6 to 98.7 (103.9 expected) in September

- API: U.S. crude oil inventories fell by 4.339M barrels (1.1M-barrrel draw expected, 1.96M-barrel increase previous) in the week ending September 20

- Japan services producer price index for August: 2.7% y/y (2.6% expected, July reading revised down from 2.8% to 2.7%)

Broad Market Price Action:

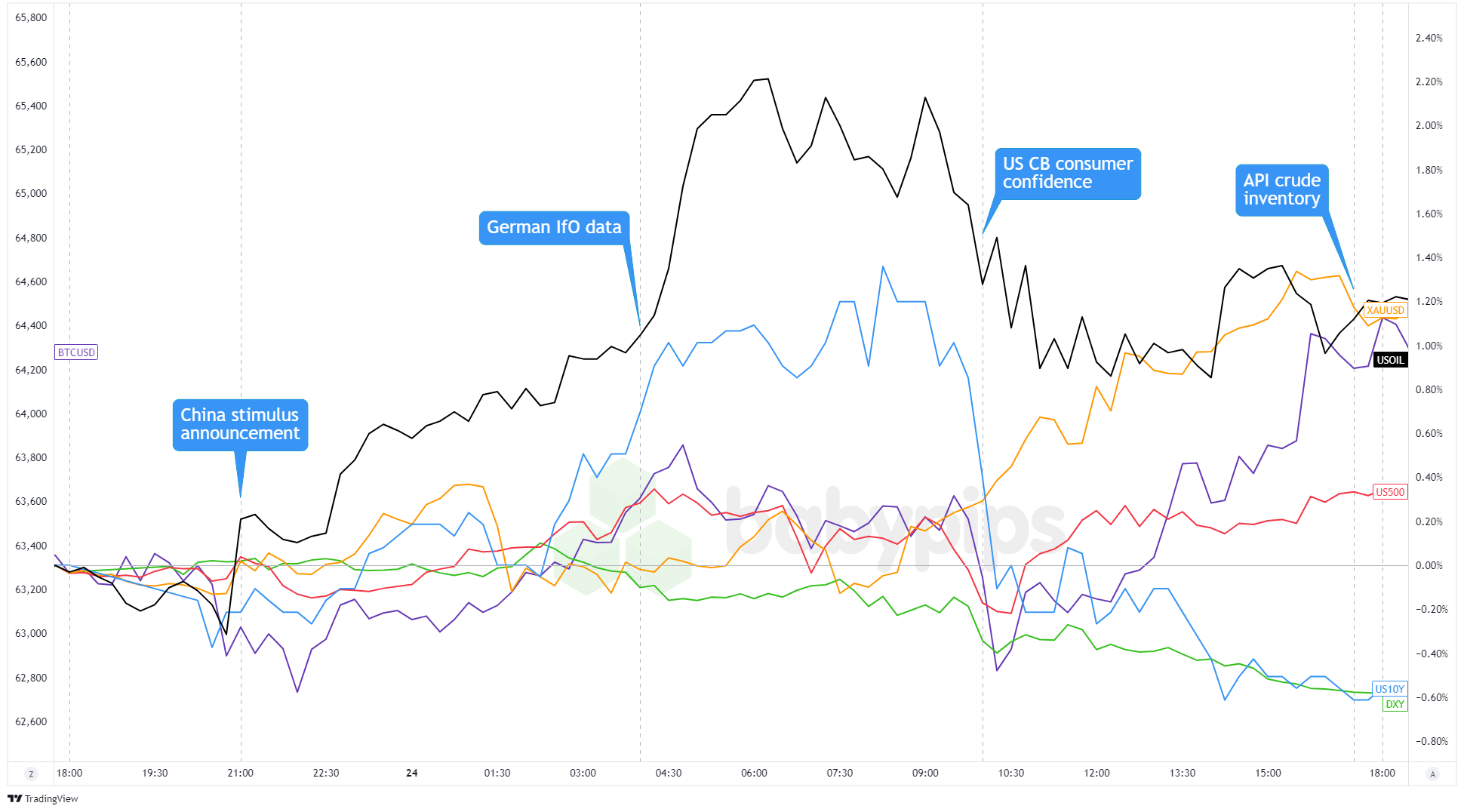

Dollar Index, Gold, S&P 500, Oil, U.S. 10-yr Yield, Bitcoin Overlay Chart by TradingView

Risk assets and major U.S. dollar counterparts got a boost during early Asian trading after Chinese officials rolled out plans to stimulate the economy. The measures include cutting the PBOC’s interest rates and reserve requirement ratio, lowering mortgage rates, and allowing companies to use PBOC funding to buy stocks.

China’s stimulus, paired with the Fed’s recent 50-basis-point rate cut, sparked risk-on sentiment across markets. Traders rode the optimism until the European and U.S. sessions, where weaker-than-expected German Ifo business climate data and a soft U.S. CB consumer confidence report took some wind out of the risk appetite.

Even with these weaker mid-tier reports, gold still hit new record highs, closing near $2,660. Bitcoin (BTC/USD) retested its September highs close to $64,700, while both the S&P 500 and Dow finished at fresh record highs.

Meanwhile, crude oil found additional support from rising tensions between Israel and Iran-backed Hezbollah in southern Lebanon, touching new weekly highs around $72.25 before settling near $71.50.

FX Market Behavior: U.S. Dollar vs. Majors:

Overlay of USD vs. Major Currencies Chart by TradingView

The U.S. dollar extended its losses as traders continued to price in the Fed’s easing cycle, while central bankers from other major economies drove individual currency moves.

Risk-on sentiment and USD-selling gained momentum after China announced easing measures, including cuts to PBOC interest rates and mortgage rates, and potential PBOC funding for companies to buy stocks.

The yen weakened after BOJ Governor Ueda hinted that rate hikes aren’t imminent. Meanwhile, the Australian dollar faced a ‘buy the rumor, sell the news’ dip, trading lower briefly despite the RBA’s ‘hawkish hold.’

Elsewhere, ECB’s Muller signaled a potential rate cut, favoring December over October. BOE Governor Bailey pointed to gradual rate reductions, while BOC’s Macklem hinted at further cuts.

The Greenback took another hit after a soft U.S. CB consumer confidence report, closing weaker across the board, with its largest losses against commodity currencies and smaller losses versus the yen.

Upcoming Potential Catalysts on the Economic Calendar:

- UBS economic expectations at 8:00 am GMT

- BOE member Megan Greene to give a speech at 8:00 am GMT

- U.S. new home sales at 2:00 pm GMT

- EIA crude oil inventories at 2:30 pm GMT

- FOMC voting member Adriana Kugler to give a speech at 8:00 pm GMT

- BOJ meeting minutes at 11:50 pm GMT

- RBA financial stability review at 1:30 am GMT (Sept 26)

Central banks will remain in focus as there aren’t a lot of top-tier data releases on tap.

BOE’s Greene could shake up Sterling’s price action in the London session while FOMC voting member Adriana Kugler could defend her vote to cut rates by 50bps during the U.S. session.

Mid-tier releases like the U.S. new home sales and EIA crude oil inventories can also influence overall risk sentiment, so make sure to keep your eyes glued to the tube if you have trades open this week!

Don’t forget to check out our brand new Forex Correlation Calculator!