Happy New Year!

2024 promises to be a wild ride for the forex market!

From central bank showdowns to political drama, it’s going to be an exciting year trading currencies!

Let’s unpack what’s in store for major currencies like the US dollar, euro, yen, and more.

But first, let’s review how the major currencies fared in 2023.

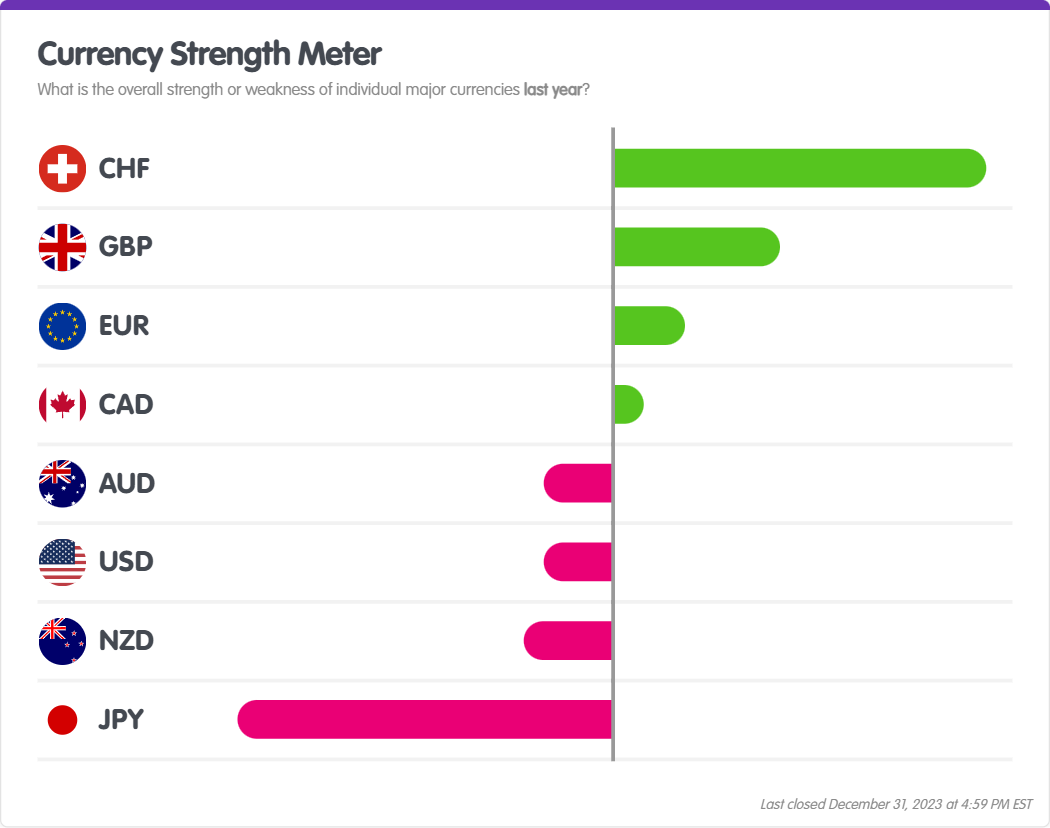

What was the strongest and weakest currency in 2023?

Based on MarketMilk’s Currency Strength Meter, the Swiss Franc (CHF) was the strongest currency.

And the Japanese yen (JPY) was the weakest currency overall.

Who were the winners and losers in 2023?

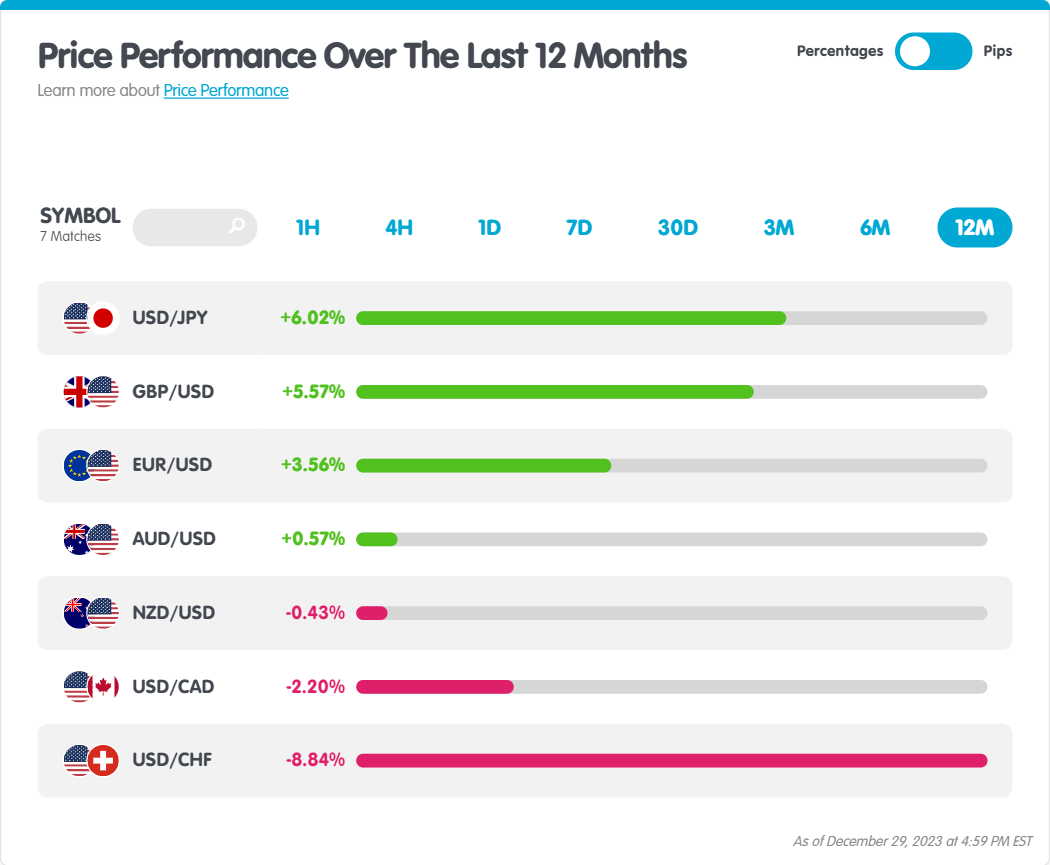

In 2023, the performance of major currency pairs varied.

Let’s see who soared and who sank last year:

Using the Performance tool for “The Majors” watchlist on MarketMilk, we can quickly see how each currency pair performed (based on percentage) over the last 12 months.

USD/JPY ended the year as the winner gaining over 6%, and GBP/USD not far behind gaining over 5.5%.

USD/CHF was the biggest loser, falling over 8%.

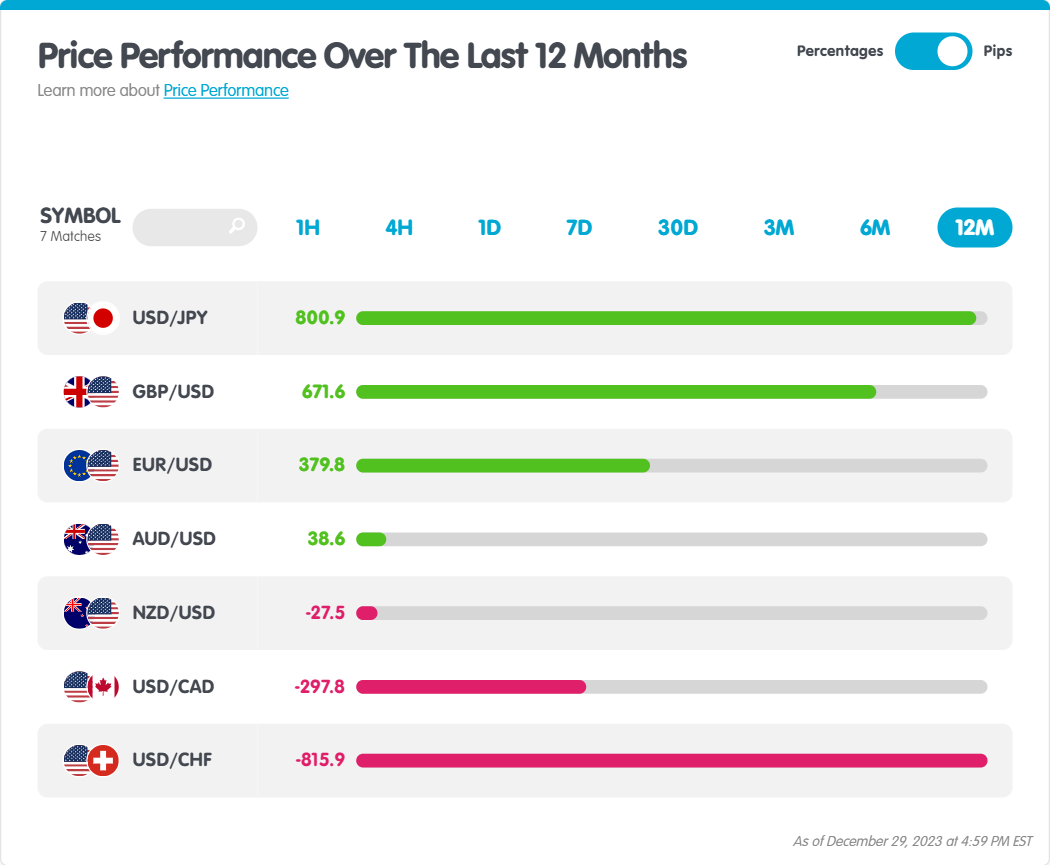

Here are their price performances measured in pips:

Isn’t it interesting how AUD/USD and NZD/USD ended the year almost unchanged from the start of the year?!

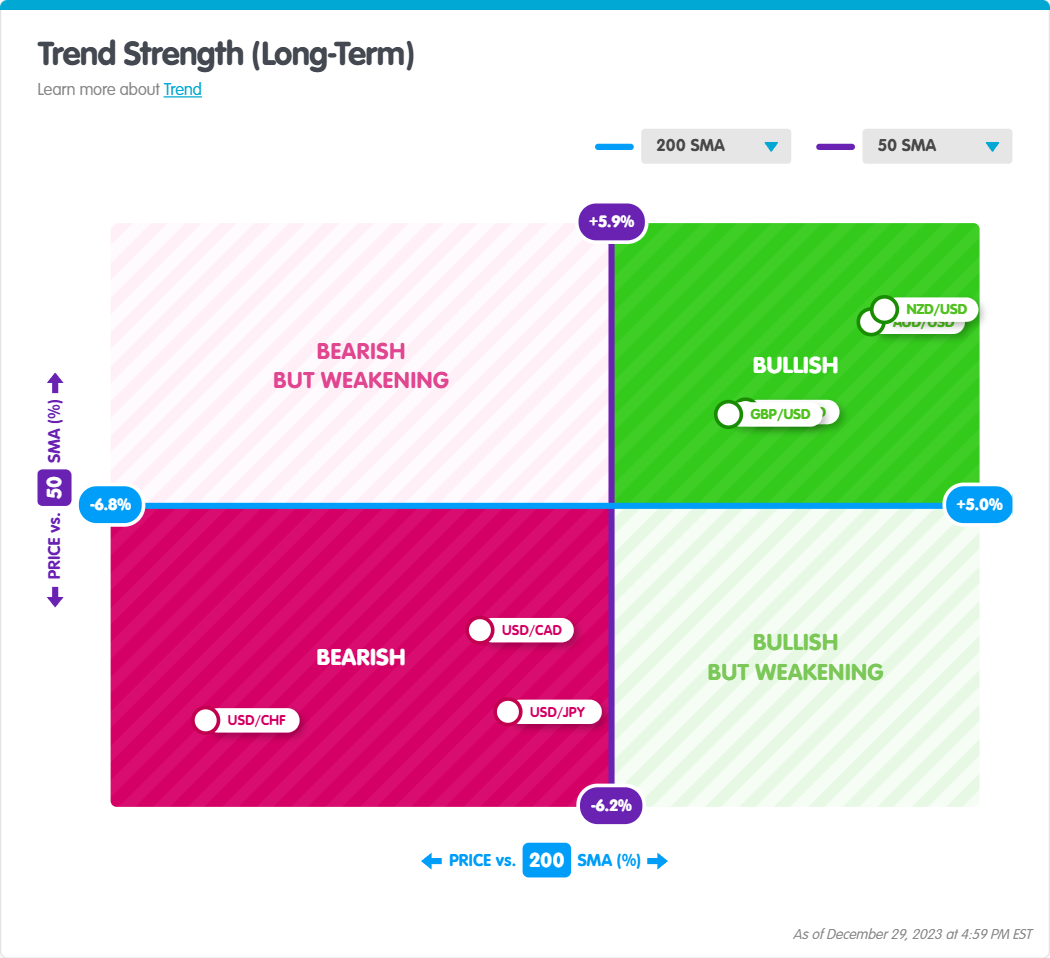

Bullish or bearish?

Which currency pairs are starting the year in a long-term bullish trend? Are there any in a long-term bearish trend?

Using the Trend Matrix tool for “The Majors” watchlist on MarketMilk, let’s find out:

The matrix above shows where each currency pair is trading relative to their daily 50 and 200 SMA.

Bullish trend:

As you can see, AUD/USD, NZD/USD, GBP/USD, and EUR/USD are all trading above their 50 SMA (purple y-axis) and 200 SMA (blue x-axis).

In this group, NZD/USD is trading the furthest way from both its 50 and 200 SMA. We can confirm this by looking at an actual daily chart:

NZD/USD Chart by TradingView

The arrow shows how far ABOVE the last closed price is from the 200 SMA (blue) and 50 SMA (purple).

Bearish trend:

For the bears, USD/CAD, USD/CHF, and USD/JPY are all trading below their 50 SMA (purple y-axis) and 200 SMA (blue x-axis).

In this group, USD/CHF is trading the furthest way from both its 50 and 200 SMA. Again, we can confirm this by looking at its price chart:

AUD/USD Chart by TradingView

The arrow shows how far BELOW the last closed price is from the 200 SMA (blue) and 50 SMA (purple).

Now, the question is will these trends continue or reverse in 2024?

Last Chance! Year-End Promo Ends Tonight!

Time is ticking on our year-end promo! Upgrade to Babypips Premium and access exclusive content, features, and more. Get 10% off your premium subscription before it’s gone! Use code HOLIDAY at checkout. Subscribe now!

Here’s my outlook for each currency pair for the new year:

EUR/USD

Look for the EUR/USD to modestly rise this year due to a slowdown in the US economy, a reduction in inflation, and the Federal Reserve (Fed) adopting a less restrictive monetary policy.

Due to tighter financial conditions which should discourage businesses and individuals from borrowing and spending (“reduce aggregate demand”), which should slow down the economy, which should cause inflation to slow even further (“disinflation”), the Fed is expected to start cutting interest rates around spring.

This would be bearish for the dollar and bullish for the euro.

Based on historical seasonal patterns, the dollar tends to perform well at the start of the year, and with the eurozone likely in recession, Q1 might be too soon to see a significant rally in EUR/USD, so Q2 seems a higher probability.

That said, a huge increase in USD liquidity in Q1 due to the combination of the draining of the Overnight Reverse Repo (ON RRP) facility, the drawdown of the Treasury General Account (TGA), and the Bank Term Funding Program (BTFP) arbitrage could override the seasonal pattern and cause the EUR/USD to strengthen earlier than expected.

Other potential obstacles to a EUR/USD rally include a further deterioration in economic growth in the eurozone and the possibility that the European Central Bank (ECB) also cut rates, following the Fed’s lead.

Cutting rates would keep the yield differentials from narrowing as much as expected. So if the ECB lowers rates sooner, and the Fed later, this could cause EUR/USD to weaken.

Lastly, let’s not forget about the upcoming US presidential election! The election can have a significant impact on the dollar but predicting the exact nature of this impact involves a fair amount of speculation (“guessing”). Since the candidates aren’t even finalized yet, we’ll have to wait and see.

For example, while Trump’s election in 2016 initially strengthened the dollar, it later stabilized, suggesting other factors played a bigger role in the long run. His 2020 defeat also didn’t translate into any significant currency movements.

For now, I think the Fed’s interest rate path and the ECB stance will likely have a greater impact on EUR/USD than the election results. If the Fed continues raising rates faster than the ECB, the dollar could strengthen, regardless of who wins the presidency.

GBP/USD

The British pound took off in 2023 after the Bank of England (BoE) hiked rates aggressively to fight soaring inflation.

Even at a 15-year high of 5.25%, the BoE is expected to maintain these high rates. This stance has provided support for the British pound, especially since the BoE’s approach is more aggressive than that of the Federal Reserve (Fed).

But the story doesn’t end there. While high rates support the pound now, they also slow down the economy.

With inflation expected to cool down over time, the BoE is likely to start cutting rates by mid-2024. Around 100 basis points worth of cuts are expected for the second half. This scenario would take the wind out of the pound’s sails.

If the UK’s economic data turns out to be significantly worse than expected, the focus might shift from the central bank’s monetary policies to the worsening economic situation, which could further weaken the pound.

On the flip side, if the economic data consistently outperforms expectations, it could lead to the BoE choosing to not cut rates (or cut less than expected), which would boost the pound.

USD/JPY

The Japanese yen (JPY) has been the biggest loser of 2023, falling against all other major currencies.

Why? Because Japan’s central bank, the Bank of Japan (BoJ), has been “zigging” while the other central banks have been “zagging.”

While other major central banks were raising interest rates to fight inflation, the BoJ has kept its interest rate below zero. This “ultra-loose” policy makes holding the yen less attractive compared to currencies offering higher returns.

However, things might be changing. Rumors about the BoJ ditching its sub-zero rate have surfaced, along with expectations of the future Fed rate cuts. These shifts have already boosted the yen, with USD/JPY plunging from 151.90 in mid-November to below 141.00 in December!

If the Fed starts to cut rates, the gap between US and Japanese interest rates will shrink.

And even if the BoJ doesn’t abandon its sub-zero rate entirely, even a small increase would boost the yen compared to the current situation.

As the interest rate differential between the USD and JPY narrows. look for the yen to continue to gain strength in 2024.

USD/CHF

Due to its status as a “safe-haven” currency, the Swiss franc (CHF) has become a go-to choice for folks looking for stability amidst the geopolitical unrest in Ukraine and the Middle East.

As these conflicts continue, the CHF is likely to continue being a popular choice due to its “safety.”

Another factor contributing to the franc’s strength is the successful efforts of the Swiss National Bank (SNB) in maintaining a relatively stable inflation environment by keeping inflation below its target of 2%.

However, the most significant factor behind the franc’s strength last year might be the SNB’s active currency intervention to strengthen the currency.

The central bank has been purchasing CHF (by selling foreign currencies) in the FX market as a part of tightening its monetary policy, viewing a strong franc as necessary to prevent inflation from imported goods.

Looking ahead, current market expectations of about 70 basis points of interest rate cuts from the SNB next year. This suggests that the SNB’s monetary policy will not be as aggressive as that of the Fed or the ECB in terms of rate cuts.

This should provide support for CHF in 2024 even if the SNB stops intervening.

Have you subscribed yet? Year-End Promo Ends in Hours! ⌛

Don’t miss out on our year-end promo! Get 10% off your premium subscription before it’s gone! Use code HOLIDAY at checkout. Upgrade to Babypips Premium to unlock exclusive content, features, and more. Subscribe now!

AUD/USD

The story of the Australian dollar (AUD) in 2023 wasn’t a happy one.

The Fed started raising interest rates earlier than the Reserve Bank of Australia (RBA), making the US dollar more attractive due to the interest rate differential. This has weighed heavily on the AUD/USD.

But 2024 could be a different story. The Fed is singing a new tune. having recently hinted at cutting rates, potentially even lower than Australia’s. This would narrow the interest rate differential and give the AUD a boost.

However, even with a narrowing interest rate differential, the Aussie faces some challenges. China, a key trading partner for Australia, is showing signs of a slowdown. This could hurt Australia’s exports and limit its economic growth, which is a negative for AUD.

Also, if the RBA’s rate hikes cause a sharp economic slowdown or even a recession, the AUD could suffer a big fall.

That said, if the RBA can achieve a “soft landing” for the economy and avoid a recession, or if the global economy rebounds unexpectedly, Australian growth and inflation could stay strong, which would be bullish for the AUD.

Will the Aussie take off or faceplant in 2024? Stay tuned for the RBA’s February meeting. The RBA will release its quarterly monetary policy statement, along with its updated economic forecasts, and hold a press conference. Their tone and any hints about future rate decisions will heavily influence AUD/USD’s direction.

NZD/USD

Inflation, hiring, and wage growth are all ticking down, suggesting the Reserve Bank of New Zealand (RBNZ) will likely start cutting rates by summer. However, several factors add uncertainty to this outlook.

The ongoing surge in migration and high government spending from the previous administration could push inflation higher than expected. This would make it harder for the RBNZ to cut rates.

The recent change in New Zealand’s government could also significantly impact RBNZ policy.

New Zealand’s recently-elected conservative coalition government plans to implement tax cuts, which could be inflationary.

They also want to change the RBNZ’s focus from a “dual mandate” of controlling inflation and unemployment to just inflation (“price stability”). A bill was recently passed by the Parliament to repeal the mandate.

This could mean higher interest rates for longer, which would be bullish for the Kiwi dollar.

U.S. Dollar Index (DXY)

Since the Federal Reserve’s dovish shift, the Dollar Index has been experiencing downward pressure, a trend that continued as the year closed. The Dollar Index fell by 2.1% in 2023.

This decline in the dollar was primarily fueled by market expectations that the Fed was finished with hiking interest rates and would start reducing them early and aggressively in 2024.

Fed fund futures indicate there’s about a 70% chance that the fed fund rates will end 2024 in the range of 3.50% to 4.00%.

Entering 2024, the markets perceive the Fed as the most likely among the major central banks to initiate rate cuts, anticipated to begin in March.

As long as this view holds, it will be difficult for the dollar to make a significant recovery. It seems likely that the dollar will soon test the 100 level.

This perception of the Fed as the most dovish of the major central banks could shift due to several factors:

- The Fed could adopt a more hawkish stance and challenge the expectations of a March rate cut.

- There could be a rebound in US inflation.

- Officials from the European Union and/or other major central banks could unexpectedly lean towards dovish policies and forecast rate cuts earlier than expected.

Unless any of these scenarios unfold though, the dollar is likely to continue its downward trajectory. ⬇️