This week our currency strategists focused on the U.K. jobs update and the U.S. CPI update for potential high-quality setups.

Out of the four scenario/price outlook discussions this week, two discussions arguably saw both fundie & technical arguments triggered to become potential candidates for a trade & risk management overlay. Check out our review on those discussions to see what happened!

Watchlists are price outlook & strategy discussions supported by both fundamental & technical analysis, a crucial step towards creating a high quality discretionary trade idea before working on a risk & trade management plan.

If you’d like to follow our “Watchlist” picks right when they are published throughout the week, you can subscribe to BabyPips Premium.

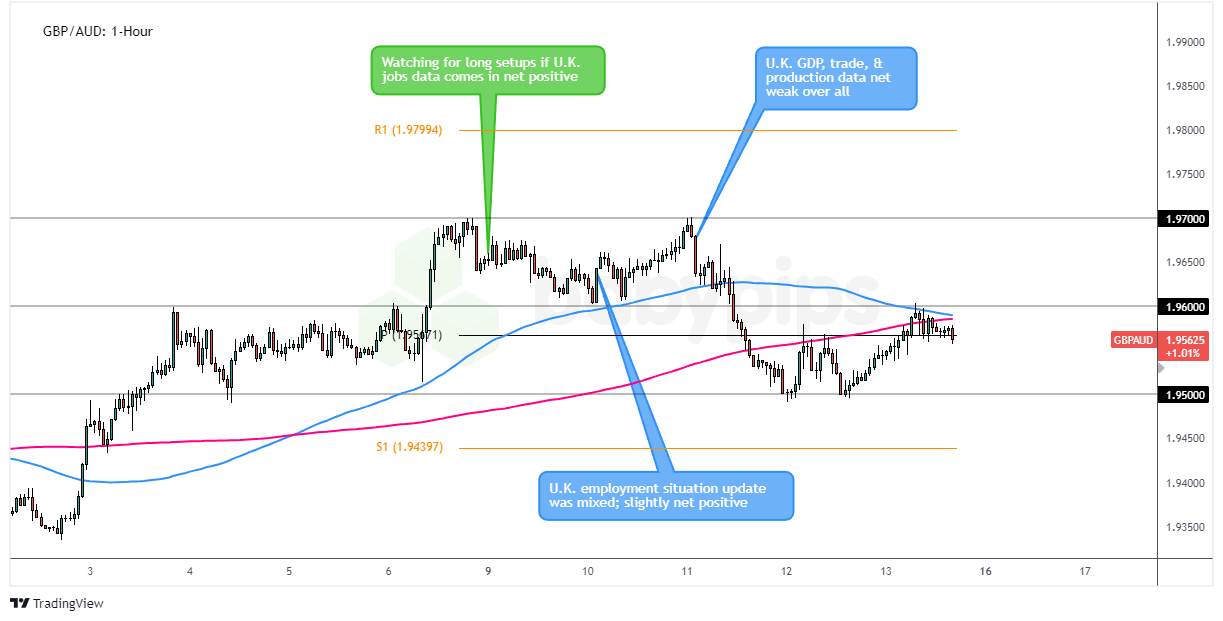

GBP/AUD: Monday – September 9, 2024

GBP/AUD 1-Hour Forex Chart by TradingView

On Monday, our strategists had their sights set on the U.K. Employment Situation Update for September 2024 and its potential impact on the British pound. Based on our Event Guide, expectations were mixed, with the claimant count change seen easing from 135K to 21K, the unemployment rate expected to steady at 4.2%, and average earnings index growth projected to slow from 5.4% to 4.9%.

With those expectations in mind, here’s what we were thinking:

The “Sterling Surge” Scenario:

If the employment data came in stronger than expected, particularly with lower jobless claims and steady or higher wage growth, we anticipated this could draw in fundie buyers boost the pound. We focused on GBP/AUD for potential long strategies, especially given the pair’s recent upward momentum in September and the recent growth worries from China influencing the Australian dollar.

The “Pound Plunge” Scenario:

If the U.K. jobs data disappointed, mainly showing a higher unemployment rate or a significantly slower wage growth rate, we thought this could weaken the pound. In this case, we considered GBP/JPY for potential short strategies, given the yen’s recent strength and the rate hike expectations from the Bank of Japan.

What Did the Data Say

The U.K. jobs data provided a mixed picture with the unemployment rate ticking down, but wage growth slowed to still elevated 4.0% rate. Overall, this update was generally perceived as slightly more positive than the markets expected, based on the reaction in Sterling.

Market Reaction

The initial market response to the U.K. jobs data was marginally positive for the pound against all major currencies, particularly the “safe havens.” This fundamentally aligned with our “Sterling Surge” scenario for GBP/AUD. As far as our technical arguments, we pointed out both a sustained upside break scenario and a pullback scenario to watch out for.

The initial reaction pushed GBP/AUD up to our upside break watch area of 1.9700 but that was the bearish turning point for the pair, thanks to a net negative economic activity update from the U.K. on Wednesday.

This pulled the market to our pullback-support area of watch, between 1.9550 – 1.9600. But thanks to the net weak U.K. economic activity update, bulls didn’t really step in until a test of the 1.9500 major psychological level. It was there that a double bottom formed, creating a technical signal the bulls were likely taking back control.

The Verdict

So, how did we do? In our original discussion, we mentioned potential long setups on GBP/AUD if the U.K. employment data came in net positive, which it did. The pullback scenario played out, but with the net weak U.K. economic activity update somewhat cancelling out our fundamental bullish bias after the slightly net positive U.K. jobs update, it’s tough to say that this was a high quality long setup.

But for those who considered a long play around the 1.9550 – 1.9600 potential support area without waiting for bullish reversal patterns, it’s likely the discussion was “not-likely” supportive of a net positive outcome.

For the more skill traders who waited for bullish behavior to form at the double bottom at 1.9500 before taking a long bias, it’s “likely” the discussion was supportive of a net positive outcome.

Overall, we’d rate this discussion as “not-likely” to “neutral” as real-time adaptations to the U.K. GDP update and following price action made the trade management plan and execution a big factor in the potential outcome.

USD/CAD: Tuesday – September 10, 2024

USD/CAD: 1-Hour Forex Chart by TradingView

On Tuesday, our strategists eyed the upcoming U.S. CPI report and its potential implications for the U.S. dollar. Based on our Event Guide for the CPI report, the markets were expecting headline inflation to come in at +0.2% m/m and +2.7% y/y, with core inflation at +0.3% m/m and +3.2% y/y. With those expectations and looking at the potential effects of recent economic events, here’s what we were thinking:

The “Greenback Gain” Scenario

If the CPI came in as expected or higher, we figured the Fed might lean towards a smaller 25bps rate cut in September. This could draw in fundamental USD buyers, and with the BOC recently cutting rates and signaling more easing to come, we eyed USD/CAD for potential long strategies to watch.

The “Dollar Dive” Scenario

If U.S. inflation came in significantly lower than expected, we thought the Fed might consider a larger 50bps rate cut. This could’ve been USD sellers’ time to shine, prompting a look at EUR/USD given the pair’s recent uptrend and if the ECB’s policy decision on Thursday is less dovish than expected.

What Did the Data Say

Well, folks, Wednesday rolled around, and the U.S. CPI decided to throw us a mixed bag of numbers. The headline CPI showed a 0.2% month-on-month increase as expected, but the annual reading slipped from 2.9% to 2.5%, lower than the market’s 2.7% estimates and marking the slowest pace since March 2021.

However, the core CPI (excluding food and energy) ticked higher from 0.2% to 0.3% m/m, matching expectations. The annual core inflation held steady at 3.2%, also in line with forecasts.

The hotter-than-expected monthly core CPI reading caught the market’s attention, as it showed persistent inflationary pressures in key areas like shelter costs, airline fares, and motor vehicle insurance.

Market Reaction

The initial market reaction was swift, with the U.S. dollar seeing a sharp but brief rally across the board. Looking at our USD/CAD chart, we can see that the pair indeed saw an immediate bounce following the CPI release, climbing from around the 1.3575 level towards the first target, the R1 pivot resistance point at 1.3613.

However, the pair’s upward momentum was somewhat tempered by broader market dynamics. The sentiment that prevailed after the initial volatility, which had initially supported the dollar, began to wane. Additionally, the reduced odds of a 50bps Fed rate cut likely capped the dollar’s gains.

Interestingly, the chart shows that after the initial spike, USD/CAD pulled back, possibly on some profit-taking and repositioning ahead of the U.S. PPI data due the next day. The pair found support around the pivot point (PP) at 1.3540, which aligned with the rising trendline that had been in place since early September.

By Thursday, we saw another push higher in USD/CAD as the U.S. PPI and weekly jobless claims data came in net positive for the dollar. This helped the pair find support with price action respecting the rising moving averages and the broken resistance area at 1.3575.

The Verdict

So, how’d we do? In our original discussion, we mentioned potential long setups on USD/CAD if the U.S. CPI came in line with expectations or higher, which it partially did (core CPI).

After the news the market did move to our first discussed target, but the market was limited there. There was also several opportunities to buy after pullbacks, although the successive rebounds were less intense thanks to rising 50 bps Fed cut expectations at the end of the week.

Overall, we’d rate this discussion as “likely” in supporting a potential positive outcome because while the strategy and outcome worked out well in favor of the fundamental long, the upside move was limited and individual trade execution and risk management decisions would have been crucial factors in the final result.